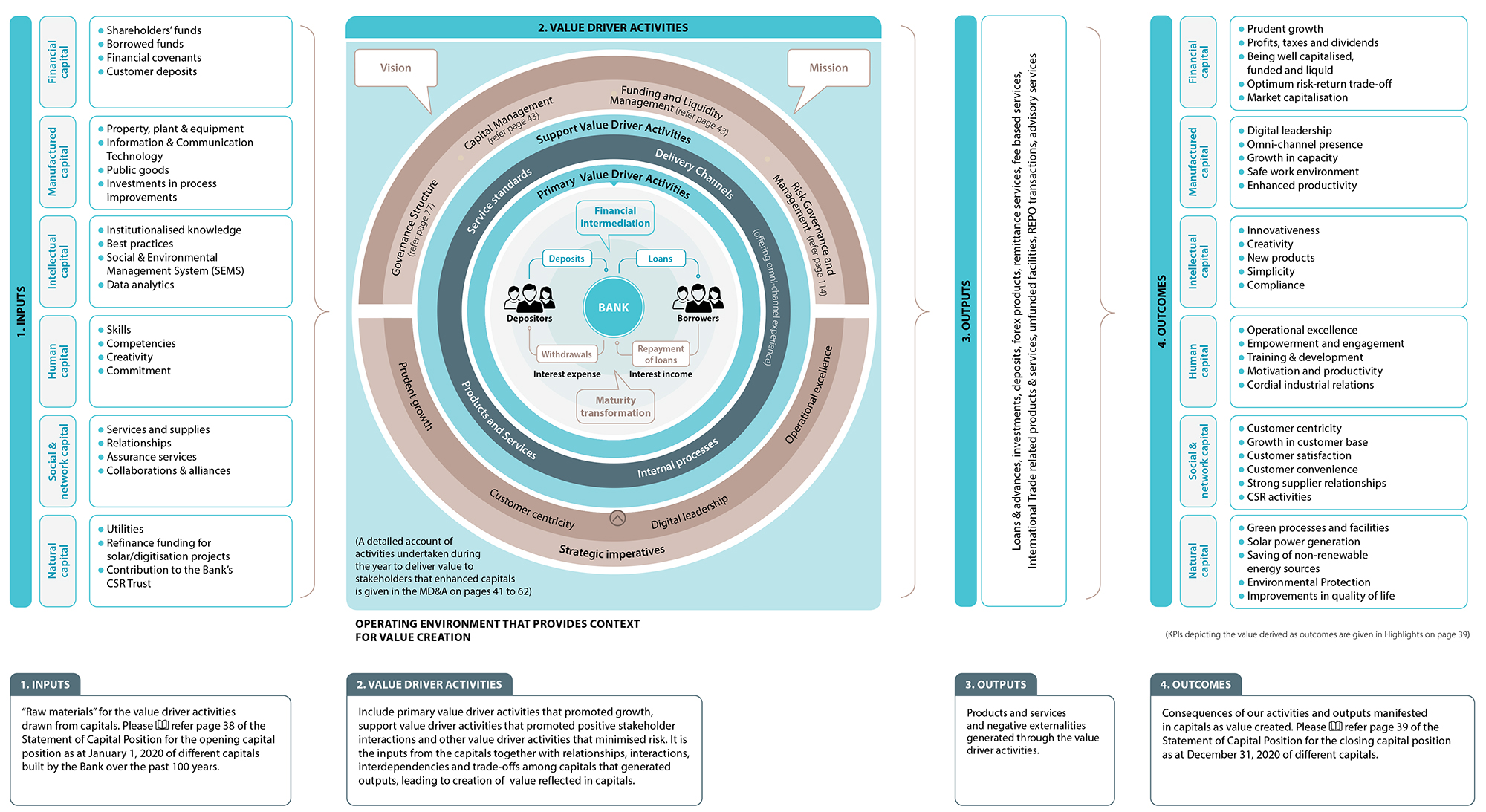

Business Model for Sustainable Value Creation

The specification of an organisation’s business model is a crucial aspect of the integrated reporting process. An organisation’s business model is its system for creating value, i.e. its system for transforming inputs, through its essential business activities, into outputs and outcomes that realise the organisation’s strategic objectives. For the reader of this report, it is helpful to briefly clarify each of those four terms to provide a guide for following the visual depiction of the Bank’s business model below.

Inputs refer to the "capitals" – stocks of value – the organisation uses as resources, or, in other words, the capitals from which an organisation derives value. These input capitals include not only financial capital reflected in the Statement of Financial Position, but also what might be termed “off-balance sheet” or "hidden" capitals, like the tacit knowledge of an organisation, the brand and reputation an organisation has built over years, or the strength of its stakeholder relationships. These inputs are then put to work in the organisation’s business activities – literally capitalised – to generate outputs (the organisation’s key products and services) and outcomes (the value created by the organisation for itself and for its stakeholders as a consequence of the outputs). As the Bank’s business model demonstrates, this is a dynamic process where capitals are constantly circulating and value is continuously being created and transformed. An integrated report is nothing but the story of this dynamic process across a single year and a snapshot of an organisation’s capital position at the year’s end (see Statement of Capital Position).

Financial intermediation and maturity transformation

The business model of the Bank revolves around the two primary value driver activities of financial intermediation and maturity transformation. Financial intermediation refers to the role the Bank plays as a conduit between depositors and borrowers, allowing savings (liabilities) to be channeled into investments and assets. Maturity transformation refers to the process of converting short-term funds into long-term lending and investments. By ensuring the efficient allocation of financial resources, these two activities are essential for the economic development of the society

at large.

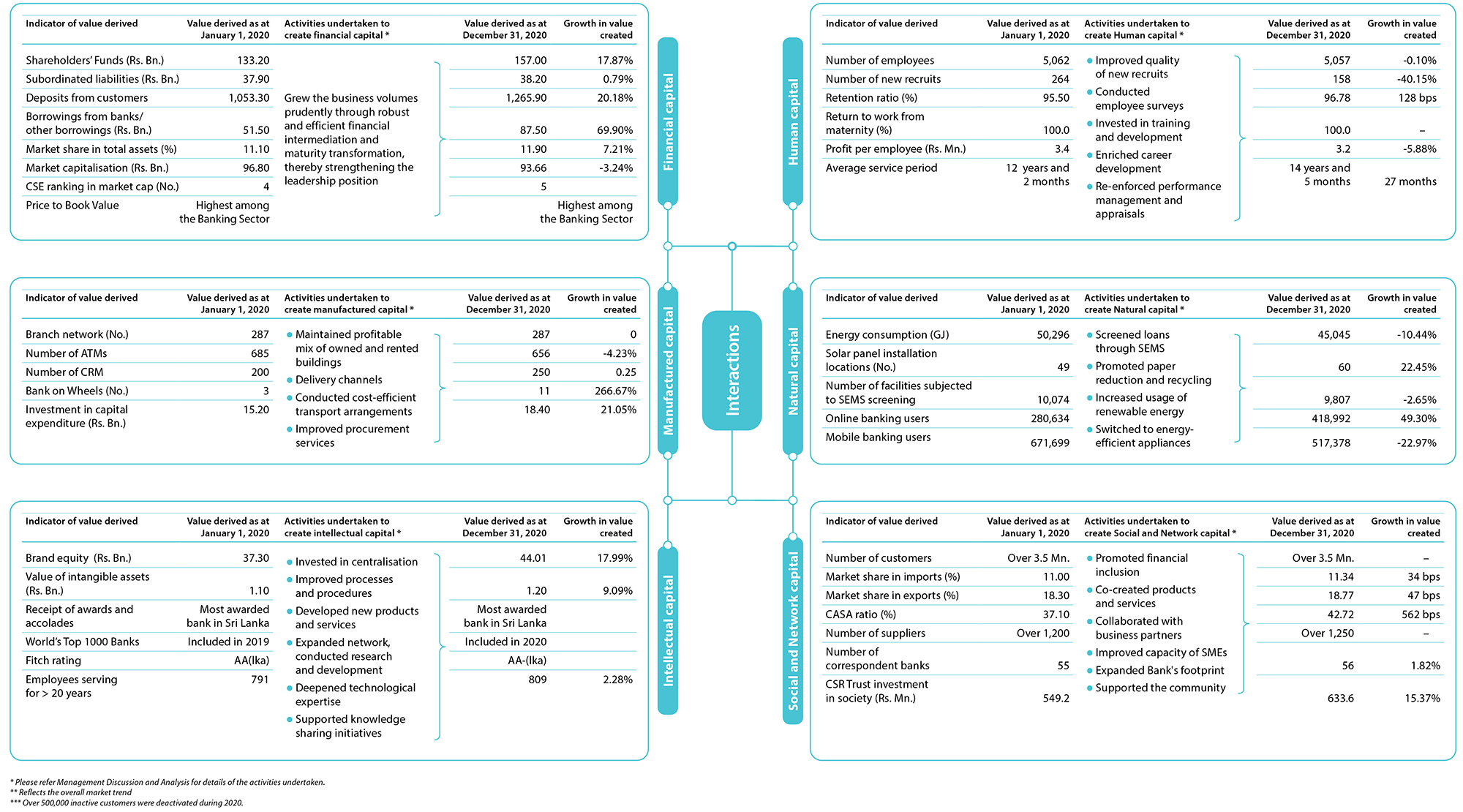

Statement of capital position

The activities the Bank undertakes in furtherance of financial intermediation and maturity transformation, and the consequent interactions and trade-off among the capitals in this dynamic process, serve to augment the capitals and reflect the value created over the year. The Statement of the Capital Position of the Bank as at January 1, 2020 and December 31, 2020 is provided on Statement of Capital Position.

Besides the value derived as reflected in the enhanced positions of the other capitals, the two broader categories of income – net interest income from fund-based operations and fee and commission income from fee-based operations – enable the Bank to enhance its financial capital. Fund-based operations involve the process of mobilising funds from depositors and borrowings from other sources in order to lend and invest; this process generates interest income and incurs interest expenses. The interest margin, which is the difference between the lending rate and the borrowing rate, compensates the Bank for the credit risk, funding risk and interest rate risk. All other services provided by the Bank not involving funds are fee-based operations. Reflecting efficient financial intermediation, the Bank generated 66.15% of its total operating income by way of net interest income (2019 : 71.51%).

Gearing

Financial intermediation and maturity transformation cause the business model of banks to substantially differ from other corporates. The principal difference is the substantially lower Return on Assets (ROA), which is less than 2% in general, in stark contrast to between 10% - 20% earned by corporates in other sectors. This prompts banks to resort to the process of gearing in order to make the returns to the investors attractive in terms of Return on Equity (ROE). Gearing involves expanding the business volumes by mobilising more and more funding from depositors and other providers of funds to the banks and lending or investing such funds to grow the loan book and investment portfolios on the strength of a given amount of capital.

Gearing primarily remains the foundation of the Bank’s business model, which enables us to operate at around 10 times higher business volumes compared to the shareholders’ equity. It is our license to mobilise deposits from the public that has made it possible. However, we are well aware that gearing exposes the Bank to a multitude of internal and external risks. In addition, certain emerging global developments are now threatening to disrupt this conventional business model. As explained later in the report, the Bank has established a sound risk management framework with necessary oversight of the Board of Directors and thereby has been able to successfully manage such risks.

Stakeholder returns

As shown in Table 07, Commercial Bank has been able to improve its profitability over the years while prudently maintaining gearing at acceptable levels. This improvement in profitability reflects the net impact of the value we have been able to create by delivering value to and by deriving value from our stakeholders. From investors’ perspective, this value creation is reflected in the returns the Bank has been able to generate for them in terms of earnings, dividends and appreciation in market price of shares. The market capitalisation of the Bank’s shares remained the highest among the Banking, Finance and Insurance institutions as at end 2020 while its shares ranked fifth among all listed companies in the Colombo Stock Exchange as at end 2020. Further details on the performance of the Bank’s shares are found in the section on “Investor Relations”.

While growing organically in the domestic market, the Bank has taken steps to leverage inorganic and regional growth opportunities, primarily to geographically diversify its risk exposures and sources of revenue and thereby enhance its sustainability of operations and long-term value creation. These efforts have now made the Bank a well-established regional bank.

The Bank’s business model that delivers value to and derives value from the stakeholders, leading to sustainable value creation

Figure - 07

Statement of Capital Position

Table – 07