Largest and systemically important

Commercial Bank of Ceylon PLC is the largest private sector commercial bank – and the third largest bank overall – in Sri Lanka in terms of total assets, which stood at Rs. 1.387 Tn. (USD 7.633 Bn.) as at the end of 2019. It has been designated by the Central Bank of Sri Lanka as a higher-tier Domestic Systemically Important Bank (D-SIB) and accounts for approximately 11.1% of sector assets.

A hundred year legacy

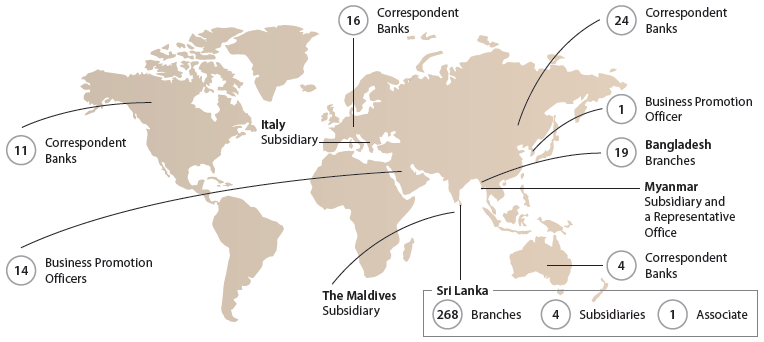

The Bank’s origins date back to 1920, and it marked a half-century of operations under its present name, Commercial Bank of Ceylon PLC. Its 5,062 employees serve over 3.5 million plus customers through a wide local and international network of branches, subsidiaries, agency arrangements, Business Promotion Officers, and correspondent banking relationships.

Growing international footprint

With the acquisition of the Bangladesh operations of Crédit Agricole Indosuez in 2003, the Bank began its expansion beyond Sri Lanka’s shores. Since then, it has established subsidiaries in Italy, the Maldives and Myanmar.

Risk profile

Commercial Bank is rated AA(lka) by Fitch Ratings Lanka Ltd, the highest rating for a local private sector bank. The rating outlook was changed from stable to negative in January 2020 consequent to revision of the outlook of the Sri Lankan sovereign and the deterioration in the operating environment. Bank’s risk profile reflects a restrained risk appetite, a robust funding base, a secure level of liquidity, a sound domestic franchise and stable, consistent performance.

Diversification

The Bank’s business is well diversified across four main business segments: Personal Banking, Corporate Banking, Treasury, and International Operations. The latter covers operations in Bangladesh, Maldives, Italy, and Myanmar, which now account for 16% of consolidated assets and 22% of consolidated profit before taxes. Besides geographical diversification, the Bank has successfully accomplished a higher level of diversification in its operations across many other parameters such as customer profile, currency wise, products and services portfolio, funding profile, maturity profile, economic sectors and the sources of revenue.

Vibrant financial intermediation

In 2019, the Bank became the first private sector bank in Sri Lanka to cross the Rupees One Trillion threshold in deposits. Customer deposits fund 76% of total assets, demonstrating the Bank’s strong role as a financial intermediary. For the past five years, the Bank’s loans to deposits ratio was 87% on average, reflecting a corresponding growth between loans and deposits. The Bank’s asset quality is one of the best in the industry, while its Current Accounts and Savings Accounts (CASA) make up 37.10% of total deposits, the highest among the local private sector banks.

Strong capitalisation

The Bank held a Total Tier 1 ratio of 12.298% as of December 31, 2019, well above the regulatory minimum of 10%. The Bank’s growth was prudent with gearing in terms of on-balance sheet assets as well as risk-weighted assets remaining at 10.42 times and 7.3 times, respectively, as of the end of 2019. Demonstrating the strength of the franchise, the Bank’s shares reported the highest price to Book Value of 0.73 times and the highest market capitalisation of Rs. 97 Bn. (USD 533 Mn.) among the Bank, Finance and Insurance institutions on the Colombo Stock Exchange at end of 2019 (the Bank is the fourth largest institution listed on the CSE overall).

Ownership of the Bank

Of approximately 12,268 ordinary voting shareholders of the Bank, DFCC Bank PLC (13.54%), Employees’ Provident Fund (9.63%), Insurance Corporation Ltd. (8.83%), Mr Y S H I Silva (8.07%), NTAsian Discovery Master Fund (5.52%), Melstacorp PLC (4.62%) and the International Finance Corporation (4.44%) are the major shareholders, holding a combined ownership stake of over 56%. Notably, the Bank has a substantial foreign shareholding, with foreign entities owning a combined 18% stake in the Bank.

Our regional presence and global connectivity

Figure – 01