1.1 Corporate information

Commercial Bank of Ceylon PLC (the “Bank”) is a public limited liability company listed on the Colombo Stock Exchange (CSE), incorporated on June 25, 1969 under the Companies Ordinance No. 51 of 1938, and domiciled in Sri Lanka. It is a licensed commercial bank regulated under the Banking Act No. 30 of 1988 and amendments thereto. The Bank was re-registered under the Companies Act No. 07 of 2007 on January 23, 2008, under the Company Registration No. PQ 116. The registered office of the Bank is situated at “Commercial House”, No. 21, Sir Razik Fareed Mawatha, Colombo 01, Sri Lanka.

The ordinary shares of the Bank (both Ordinary Voting and Non-Voting shares) have a primary listing on the CSE. The unsecured subordinated debentures of the Bank are also listed on the CSE.

The staff strength of the Group and the Bank was as follows:

| As at December 31, | 2019 | 2018 |

| Group | 5,656 | 5,457 |

| Bank | 5,062 | 5,027 |

Corporate information is presented in the inner back cover of this Annual Report.

1.2 Consolidated Financial Statements

The Consolidated Financial Statements as at and for the year ended December 31, 2019, comprise the Bank (Parent Company) and its Subsidiaries (together referred to as the “Group” and individually as “Group entities”) and the Group’s interest in its Associate.

The Bank does not have an identifiable parent of its own. The Bank is the Ultimate Parent of the Group.

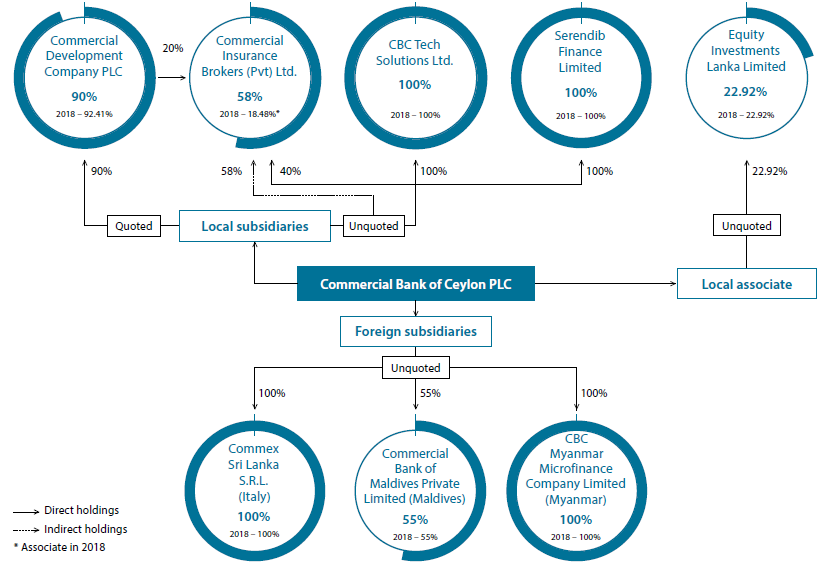

1.3 Principal business activities, nature of operations of the Group and ownership by the Bank in its subsidiaries and associate

Figure – 23

During the year, the Bank acquired 40% stake in Commercial Insurance Brokers (Private) Limited, from Chemanex PLC, for a purchase consideration of Rupees Two Hundred and Fifty Million (Rs. 250,000,000/-). As the Bank’s subsidiary, Commercial Development Company PLC too has a stake of 20% in Commercial Insurance Brokers (Private) Limited, it makes the Group’s stake in Commercial Insurance Brokers (Private) Limited to be 58% as at December 31, 2019.

Principal business activities and nature of business operations of the Group

Table – 26

| Entity | Principal business activities |

| Commercial Bank of Ceylon PLC | Banking and related activities such as accepting deposits, personal banking, trade financing, offshore banking, RFC & NRFC operations, travel-related services, corporate and retail credit, syndicated financing, project financing, development banking, lease & hire purchase, rural credit, issuing of local and international debit and credit cards, internet banking, mobile banking, money remittance facilities, dealing in Government Securities and treasury-related products, salary remittance package, bullion trading, export and domestic factoring, pawning, margin trading, digital banking services, bancassurance and Islamic banking products and services etc. |

| Subsidiaries | |

| Commercial Development Company PLC (CDC) | Property development, related ancillary services and outsourcing of staff for non-critical functions of the Bank (parent). |

| CBC Tech Solutions Limited | Providing Information & Communication Technology (ICT) related products, services and solutions to corporate sector. |

| Serendib Finance Limited (SFL) | Providing financial services including leasing, hire purchase, loans etc. |

| Commercial Insurance Brokers (Pvt) Limited (CIB) | Providing professional service and handling all insurance portfolios of individuals as well as many leading and reputed organizations in Sri Lanka engaged in diverse business activities. |

| Commex Sri Lanka S.R.L. (Commex) | Operating as an agent to the Bank (parent) for opening accounts, providing money transfer services, issuance and encashment of foreign currencies and travelers cheques, collecting applications for credit facilities and handling of ATM cards etc. |

| Commercial Bank of Maldives Private Limited (CBM) |

Offering of extensive range of banking and related financial services. |

| CBC Myanmar Microfinance Company Limited | Providing microfinance services to the people of Myanmar. The company also provides savings, business/livelihood development services for the clients adopting a credit plus approach. |

| Associate | |

| Equity Investments Lanka Limited | Providing investment services, risk capital and venture capital management |

2.1 Statement of compliance

The Consolidated Financial Statements of the Group and the separate Financial Statements of the Bank, have been prepared and presented in accordance with the Sri Lanka Accounting Standards (SLFRSs and LKASs), laid down by The Institute of Chartered Accountants of Sri Lanka (CA Sri Lanka) and in compliance with the requirements of the Companies Act and the Banking Act and provide appropriate disclosures as required by the Listing Rules of the CSE. These Financial Statements, except for information on cash flows have been prepared following the accrual basis of accounting.

These SLFRSs and LKASs are available at the website of CA Sri Lanka – www.casrilanka.com

The Group did not adopt any inappropriate accounting treatments, which are not in compliance with the requirements of the SLFRSs and LKASs, regulations governing the preparation and presentation of the Financial Statements.

Details of the Group’s Significant Accounting Policies followed during the year are given in Notes 6 to 10.

The formats used in the preparation and presentation of the Financial Statements and the disclosures made therein also comply with the specified formats prescribed by the Central Bank of Sri Lanka (CBSL) in the Circular No. 02 of 2019 dated January 18, 2019, on “Publication of Annual and Quarterly Financial Statements and Other Disclosures by Licensed Banks”.

2.2 Responsibility for Financial Statements

The Board of Directors of the Bank is responsible for the preparation and presentation of the Financial Statements of the Group and the Bank as per the provisions of the Companies Act No. 07 of 2007 and amendments thereto (Companies Act) and Sri Lanka Accounting Standards.

The Board of Directors acknowledges their responsibility for Financial Statements as set out in the “Annual Report of the Board of Directors”, “Statement of Directors’ Responsibility” and the certification on the Statement of Financial Position on pages 03, 103 and 139, respectively.

These Financial Statements include the following components:

- an Income Statement and a Statement of Profit or Loss and Other Comprehensive Income providing the information on the financial performance of the Group and the Bank for the year under review.

- a Statement of Financial Position (SOFP) providing the information on the financial position of the Group and the Bank as at the year end.

- a Statement of Changes in Equity depicting all changes in shareholders’ funds during the year under review of the Group and the Bank.

- a Statement of Cash Flows providing the information to the users, on the ability of the Group and the Bank to generate cash and cash equivalents and utilisation of those cash flows.

- Notes to the Financial Statements comprising Significant Accounting Policies and other explanatory information.

2.3 Approval of Financial Statements by the Board of Directors

The Financial Statements of the Group and the Bank for the year ended December 31, 2019 (including comparatives for 2018), were approved and authorised for issue by the Board of Directors in accordance with Resolution of the Directors on February 20, 2020 (The Financial Statements of the Group and the Bank for the year ended December 31, 2018, were approved and authorised for issue by the Board of Directors on February 22, 2019).

2.4 Basis of measurement

The Financial Statements of the Group have been prepared on the historical cost basis except for the following material items stated in the SOFP.

Basis of measurement

Table – 27

| Items | Basis of measurement | Note No./s |

| Financial instruments measured at fair value through profit or loss including derivative financial instruments | Fair value | 31, 32 & 46 |

| Financial assets measured at fair value through other comprehensive income | Fair value | 36 |

| Land and buildings | Measured at cost at the time of acquisition and subsequently at revalued amounts which are the fair values at the date of revaluation |

39 |

| Investment property | Measured at cost at the time of acquisition and subsequently at Fair value. |

40 |

| Defined benefit obligation | Net liability for defined benefit obligations are recognised as the present value of the defined benefit obligation, less net total of the plan assets, plus unrecognised actuarial gains, less unrecognised past service cost, and unrecognised actuarial losses | 50 |

| Equity settled share-based payment arrangements | Fair value on grant date | 54 |

2.5 Going concern basis of accounting

The Management has made an assessment of its ability to continue as a going concern and is satisfied that it has the resources to continue in business for the foreseeable future.

Furthermore, the Management is not aware of any material uncertainties that may cast significant doubt upon the Group’s ability to continue as a going concern. Therefore, the Financial Statements of the Group continue to be prepared on a going concern basis.

2.6 Functional and presentation currency

Items included in these Financial Statements are measured using the currency of the primary economic environment in which the Bank operates (the functional currency).

Each entity in the Group determines its own functional currency and items included in the Financial Statements of these entities are measured using that functional currency. There was no change in the Group’s presentation and functional currency during the year under review.

These Financial Statements are presented in Sri Lankan Rupees, the Group’s functional and presentation currency.

The information presented in US Dollars in the Section on “Supplementary Information” does not form part of the Financial Statements and is made available solely for the information of stakeholders.

2.7 Presentation of Financial Statements

The assets and liabilities of the Group presented in the SOFP are grouped by nature and listed in an order that reflects their relative liquidity and maturity pattern.

No adjustments have been made for inflationary factors affecting the Financial Statements.

An analysis on recovery or settlement within 12 months and more than 12 months from the Reporting date is presented in Note 62.

2.8 Rounding

The amounts in the Financial Statements have been rounded-off to the nearest rupees thousands, except where otherwise indicated as permitted by the Sri Lanka Accounting Standard – LKAS 1 on “Presentation of Financial Statements” (LKAS 1).

2.9 Offsetting

Financial assets and financial liabilities are offset and the net amount reported in the SOFP, only when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or to realise the assets and settle the liabilities simultaneously. Income and expenses are not offset in the Income Statement, unless required or permitted by an Accounting Standard or Interpretation (issued by the IFRS Interpretations Committee and Standard Interpretations Committee) and as specifically disclosed in the Significant Accounting Policies of the Bank.

2.10 Materiality and aggregation

Each material class of similar items is presented separately in the Financial Statements. Items of dissimilar nature or function are presented separately, unless they are immaterial as permitted by the LKAS 1 and amendments to the LKAS 1 on “Disclosure Initiative” which was effective from January 1, 2016.

Notes to the Financial Statements are presented in a systematic manner which ensures the understandability and comparability of Financial Statements of the Group and the Bank. Understandability of the Financial Statements is not compromised by obscuring material information with immaterial information or by aggregating material items that have different natures or functions.

2.11 Comparative information

- Comparative information including quantitative, narrative and descriptive information is disclosed in respect of the previous period in the Financial Statements in order to enhance the understanding of the current period’s Financial Statements and to enhance the inter period comparability. The presentation and classification of the Financial Statements of the previous year are amended, where relevant for better presentation and to be comparable with those of the current year. The Group/Bank has not restated the comparative information for contracts within the scope of Sri Lanka Accounting Standard – SLFRS 16 on “Leases” (SLFRS 16). Therefore, the comparative information is reported under Sri Lanka Accounting Standard – LKAS 17 on “Leases” (LKAS 17) and is not comparable with the information presented for 2019. Due to adoption of SLFRS 16, deferred tax asset created under LKAS 17 on the liability of straight lining of lease rentals has been transferred directly to equity as of January 1, 2019 and are disclosed in Statement of Changes in Equity.

2.12 Use of significant accounting judgements and assumptions and estimates

In preparing the Financial Statements of the Group in conformity with SLFRSs and LKASs, the Management has made judgements, estimates and assumptions which affect the application of Accounting Policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised prospectively.

Significant areas of critical judgements, assumptions and estimation uncertainty,

in applying the Accounting Policies that have most significant effects on the amounts recognised in the Financial Statements

of the Group are as follows:

A. Significant accounting judgements

Information about judgements made in applying the Accounting Policies that have most significant effects on the amounts recognised in these Financial Statements is included in Notes 2.12.1 and 2.12.3 below.

2.12.1 Determination of control over investees

Management applies its judgement to determine whether the control indicators set out in Note 37 indicates that the Group controls the investees.

2.12.2 Classification of financial assets and liabilities

The Significant Accounting Policies of the Group provides scope for financial assets to be classified and subsequently measured into different categories, namely, at Amortised Cost (AC), Fair Value through Other Comprehensive Income (FVOCI) and Fair Value Through Profit or Loss (FVTPL) based on the following criteria;

- The entity’s business model for managing the financial assets as set out in Note 7.1.3.1.

- The contractual cash flow characteristics of the financial assets as set out in Note 7.1.3.2.

2.12.3 Classification of investment property

Management uses its judgment to determine whether a property qualifies as an investment property. A property that is held either to earn rental income or for capital appreciation or both and thus generates cash flows largely independently of the other assets held by the Group are classified as investment property. On the other hand, a property used in production or supply of goods and services or administrative purposes and thus generates cash flows that are attributable not only to property but also to other assets used in the production or supply process are classified as property, plant & equipment. The Group assesses on an annual basis, the accounting classification of its investment properties, taking into consideration the current use of such properties.

B. Assumptions and estimation uncertainties

Information about assumptions and estimation uncertainties that have a significant risk of resulting in material adjustments are included in Notes 2.12.4 to 2.12.13 below:

2.12.4 Fair Value of financial instruments

The fair values of financial assets and financial liabilities recognised on the SOFP, for which there is no observable market price are determined using a variety of valuation techniques that include the use of mathematical models. The Group measures fair value using the fair value hierarchy that reflects the significance of input used in making measurements. Methodologies used for valuation of financial instruments and fair value hierarchy are stated in Note 27.

2.12.5 Impairment losses on financial assets

The measurement of impairment losses across the categories of financial assets under Sri Lanka Accounting Standard – SLFRS 9 on “Financial Instruments” (SLFRS 9) requires judgement, in particular, the estimation of the amount and timing of future cash flows and collateral values when determining impairment losses.

Accordingly, the Group reviews its individually significant loans and advances at each reporting date to assess whether an impairment loss should be provided in the Income Statement. In particular, the Management’s judgement is required in the estimation of the amount and timing of future cash flows when determining the impairment loss. In estimating these cash flows, Management makes judgements about a borrower’s financial situation and the net realisable value of any underlying collateral. Each impaired asset is assessed on its merits, and the workout strategy and estimate of cash flows considered recoverable. These estimates are based on assumptions about a number of factors and hence actual results may differ, resulting in future changes to the impairment allowance made.

A collective impairment provision is established for:

- groups of homogeneous loans and advances that are not considered individually significant; and

- groups of assets that are individually significant but that were not found to be individually impaired.

As per SLFRS 9, the Group’s Expected Credit Loss (ECL) calculations are outputs of complex models with a number of underlying assumptions regarding the choice of variable inputs and their interdependencies. Elements of the ECL models that are considered accounting judgements and estimates include:

- The Group’s criteria for qualitatively assessing whether there has been a significant increase in credit risk and if so allowances for financial assets measured on a Life Time Expected Credit Loss (LTECL) basis.

- The segmentation of financial assets when their ECL is assessed on a collective basis.

- Development of ECL models, including the various statistical formulas and the choice of inputs.

- Determination of associations between macro-economic inputs, such as GDP growth, inflation, interest rates, exchange rates and unemployment and the effect on Probability of Default (PDs), Exposure At Default (EAD) and Loss Given Default (LGD).

- Selection of forward-looking macro- economic scenarios and their probability weightings, to derive the economic inputs into the ECL models.

The accuracy of the provision depends on the model assumptions and parameters used in determining the ECL calculations.

Refer Note 18 for details.

2.12.6 Impairment of non-financial assets

The Group assesses whether there are any indicators of impairment for an asset or a Cash Generating Unit (CGU) at each reporting date or more frequently, if events or changes in circumstances necessitate to do so. This requires the estimation of the “Value in use” of such individual assets or the CGUs. Estimating “Value in use” requires the Management to make an estimate of the expected future cash flows from the asset or the CGU and also to select a suitable discount rate in order to calculate the present value of the relevant cash flows. This valuation requires the Group to make estimates about expected future cash flows and discount rates and hence, they are subject to uncertainty.

Refer Note 7.6 for details.

2.12.7 Revaluation of property, plant and equipment

The Group measures land and buildings at revalued amounts with changes in fair value being recognised in Equity through Other Comprehensive Income (OCI). The Group engages independent professional valuers to assess fair value of land and buildings in terms of Sri Lanka Accounting Standard – SLFRS 13 on “Fair Value Measurement” (SLFRS 13). The key assumptions used to determine the fair value of the land and building and sensitivity analyses are provided in Notes 39.5 (b) and 39.5 (c).

2.12.8 Useful life-time of the property, plant and equipment

The Group reviews the residual values, useful lives and methods of depreciation of property, plant and equipment at each reporting date. Judgement of the Management is exercised in the estimation of these values, rates, methods and hence they are subject to uncertainty.

Refer Note 20.

2.12.9 Fair valuation of investment property

Fair valuation of the investment property is ascertained by independent valuations carried out by Chartered valuation surveyors, who have recent experience in valuing properties of similar location and category. They have made reference to market evidence of transaction prices for similar properties, with appropriate adjustments for size and location. The key assumptions used to determine the fair value of investment property are provided in detail in Note 40.

2.12.10 SLFRS 16 – Leases (Applicable from January 1, 2019)

2.12.10.1 Determination of the lease term for lease contracts with renewal and termination options (Group as a lessee)

The Group determines the lease term as the non-cancellable term of the lease, together with any periods covered by an option to extend the lease if it is reasonably certain to be exercised, or any periods covered by an option to terminate the lease, if it is reasonably certain not to be exercised.

The Group has several lease contracts that include extension and termination options. The Group applies judgement in evaluating whether it is reasonably certain whether or not to exercise the option to renew or terminate the lease. That is, it considers all relevant factors that create an economic incentive for it to exercise either the renewal or termination option. After the commencement date, the Group reassesses the lease term if there is a significant event or change in circumstances that is within its control that affects its ability to exercise or not to exercise the option to renew or to terminate (e.g., construction of significant leasehold improvements or significant customisation of the leased asset).

2.12.10.2 Estimating the incremental borrowing rate

As the Group cannot readily determine the interest rate implicit in the lease, it uses its incremental borrowing rate (“IBR”) to measure the lease liabilities. The IBR is the rate of interest that the Group would have to pay to borrow over a similar term, and with a similar security, the funds necessary to obtain an asset of a similar value to the right-of-use asset in a similar economic environment. The IBR therefore reflects what the Group “would have to pay’’, which requires estimation when no observable rates are available (or when they need to be adjusted to reflect the terms and conditions of the lease).The Group estimates the IBR using observable input when available and is required to make certain entity-specific adjustments.

2.12.11 Deferred tax assets

Deferred tax assets are recognised in respect of tax losses to the extent that it is probable that future taxable profit will be available and can be utilised against such tax losses. Judgement is required to determine the amount of deferred tax assets that can be recognised, based upon the likely timing and level of future taxable profits, together with future tax-planning strategies.

Refer Note 43 for details.

2.12.12 Defined benefit obligation

The costs of the defined benefit plans are determined using an actuarial valuation. The actuarial valuation involves making assumptions about discount rates, expected rates of return on assets, future salary increases, mortality rates, future pension increase, etc. Due to the long-term nature of these plans, such estimates are subject to significant uncertainty.

Refer Note 50 for the assumptions used.

2.12.13 Provisions for liabilities, commitments and contingencies

The Group receives legal claims in the normal course of business. Management has made judgements as to the likelihood of any claim succeeding in making provisions. The time of concluding legal claims is uncertain, as is the amount of possible outflow of economic benefits. Timing and cost ultimately depends on the due processes in respective legal jurisdictions.

Information about significant areas of estimation uncertainty and critical judgements in applying Accounting Policies other than those stated above that have significant effects on the amounts recognised in the Consolidated Financial Statements are described in Notes 7.10 to 7.15.

2.13 Events after the reporting period

Events after the reporting period are those events, favourable and unfavourable, that occur between the Reporting date and the date when the Financial Statements are authorised for issue.

In this regard, all material and important events that occurred after the reporting period have been considered and appropriate disclosures are made in Note 70, where necessary.

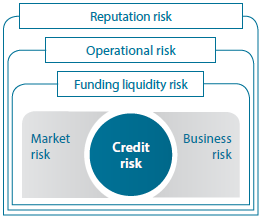

3.1 Introduction and overview

Risk is inherent in the Bank’s activities, but is managed through a process of ongoing identification, measurement and monitoring, subject to risk limits and other controls. This process of risk management is critical to the Bank’s continuing profitability and each individual within the Bank is accountable for the risk exposures relating to his or her responsibilities.

The Group has exposure mainly to the following risks from financial instruments:

- Credit risk;

- Market risk;

- Liquidity risk; and

- Operational risk.

Types of risk

Figure – 24

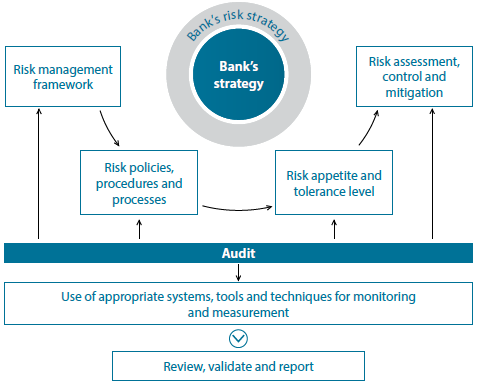

3.2 Bank’s risk management framework

The Board of Directors of the Bank has the overall responsibility for the establishment and oversight of the Bank’s Risk Management Framework.

The Risk Management Policy of the Bank translates overall risk appetite on business activities in a holistic approach to provide the guidance required for convergence of strategic and risk perspectives of the Bank.

The Group’s risk management policies are established to identify and analyse the risks faced by the Group, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. The Risk Management Policy Framework constitutes the Credit Policy, Lending Guidelines, ALM Policy including Liquidity Risk Policy, Foreign Exchange Policy, Operational Risk Policy, IT Risk Policy, Market Risk Policy, Stress Testing Policy, etc., which have been firmly established to provide control and guidance for decision-making throughout the Bank in a uniform manner.

The Committee structure embedded to the system acts as a fact finding and decision making authority through meaningful discussions of multiple points of view. The Risk Management Committees effectively deliberate on matters at hand to provide guidance to the business lines with a view to managing risk in accordance with the strategic goals and risk appetite of the Bank.

The Board of Directors of the Bank has formed a mandatory Board Committee namely, the Board Integrated Risk Management Committee (BIRMC) as per Banking Act Direction No. 11 of 2007 on Corporate Governance. The performance of the Committee and the duties and roles of members are reviewed by the Board annually.

The meetings of the Executive Integrated Risk Management Committee (EIRMC) are conducted on a monthly basis to discuss Credit, Operational and IT risk matters of the Bank while priority is given for liquidity and market risks at the Assets and Liabilities Committee (ALCO) meetings that convene at least once a fortnight.

Risk and Control Self-Assessment (RCSA) framework is adopted to identify risks involved in business activities of the Bank and to implement appropriate risk mitigatory measures after assessing criticality of such risks. The Integrated Risk Management Department carries out semi-annual Bank-wide RCSA function focusing on adherence to laws, regulations, and regulatory guidelines as well as internal controls and approved policies.

Further, the Internal Audit function of the Bank independently monitors and evaluates the risk management function of the Bank and provides their views on adequacy of the Risk Management Framework to the Board Audit Committee (BAC).

Bank‘s Financial Risk Management Framework

Figure – 25

Credit risk

The risk that the Bank will incur a loss due to its customers or counterparties fail to discharge their contractual obligations.

The Bank manages and controls credit risk by setting limits on the amount of risk it is willing to accept for individual counterparties and for geographical and industry concentrations and by monitoring exposures in relation to such limits.

Management of credit risk

Lending Guidelines of the Bank formulated in consultation with lending units provide expected granularity of credit assessment, risk grading, their acceptability of collateral, etc., as well as limits on exposures and concentration levels to various sectors, counterparties, geographies, and segments.

A robust risk grading system incorporating Basel requirements of facility rating and counterparty rating are adopted by the Bank for evaluation of credit proposals. This risk grading framework consists 10 grades of varying degrees of risk as indicators for the Lending Officers to evaluate and arrive at suitable risk-reward trade-offs in their propositions. These risk grades are reviewed by the Integrated Risk Management Department regularly.

Portfolio level credit risk analyses are taken up at monthly EIRMC as well as quarterly BIRMC meetings. Individual credit proposals evaluated by the Lending Officers are approved by the Authorising Officers within the hierarchy in Delegated Authority Levels whilst ensuring a minimum of four eyes principle when approving any lending proposals. Escalation of approving levels occurs based on exposure levels as well as final risk ratings of borrowers.

The Executive Credit Committee (ECC) and the Board Credit Committee (BCC) are entrusted with approval of high value facilities while the Board will be the ultimate authority for approving facilities beyond predetermined threshold levels. Deliberations take place at BCC level on facilities taken up for approval within the specified threshold and recommendation for approval of the Board based on quantum of exposures proposed is exercised.

The Integrated Risk Management Department provides risk approval for individual proposals above predetermined threshold levels, consequent to a rigorous independent risk evaluation guided by Credit Policy, Lending Guidelines, and circular instructions within a limit framework stemming from risk appetite of the Bank.

Market risk

The risk that the fair value or future cash flows of financial instruments will fluctuate due to changes in market variables such as interest rates, foreign exchange rates and equity prices. The Bank classifies exposures to market risk into either trading or non-trading portfolios and manages each of those portfolios separately.

The market risk for the trading portfolio is monitored and managed closely.

Management of market risk

Market Risk Policy, ALM Policy and Foreign Exchange Risk Policy are the three main policies that constitute the framework governing the Market Risk Management function of the Bank.

Due to the business model adopted by the Bank, exposure to equity and commodity risk was kept at bay throughout the year.

However, Interest Rate Risk arising from the Banking Book as well as Trading Book and Foreign Exchange Risk arising from dealing in currencies other than local currency, continued to expose the Bank to associated risk elements.

Volatile interest scenarios experienced by the country during the period impacted the financial market in Sri Lanka and challenged the Net Interest Margin. Interest Rates of the Banking Book was subjected to varying degrees of rate shocks to identify impact on earnings perspective in such rate scenarios. The results reflected predictions which assisted the Bank in formulating strategies to manage the financial position in an effective manner with the limited choices available.

Trading Book too was subjected to Value at Risk (VaR) framework internally carried out by the Bank on a regular basis. The Bank also carried out sensitivity analysis on a regular basis to ascertain the impact on portfolios maintained, mainly in Government Securities and marking to market such portfolios to reflect fair value for decision-making process.

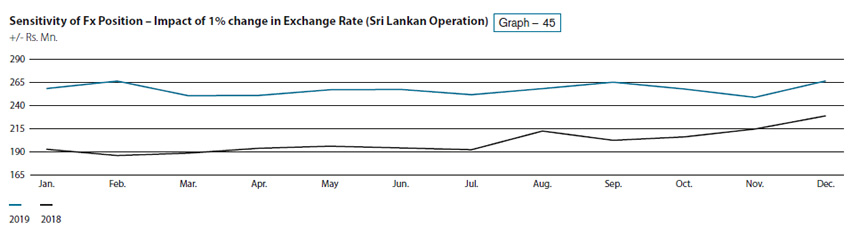

Foreign exchange positions were maintained within the regulatory framework in a market where much volatility was not observed in the major currency, compared to previous year that the Bank deals in, i.e., US Dollars. The positions were subjected to sensitivity analysis to provide insight to possible losses/gains arising from currency appreciation/depreciation, as the reporting currency of the Bank being Sri Lankan Rupees.

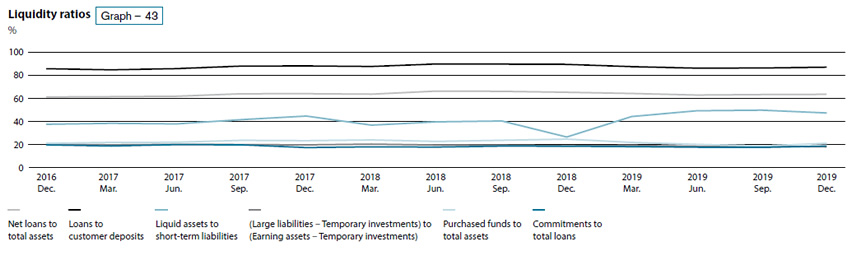

Liquidity risk

The risk that the Bank will encounter difficulty in meeting obligations associated with financial liabilities that are settled by delivering cash or another financial asset. Liquidity risk arises because of the possibility that the Bank might be unable to meet its payment obligations when they fall due under both normal and stress circumstances.

To limit this risk, Management has arranged diversified funding sources in addition to its core deposit base and adopted a policy of managing assets with liquidity in mind and monitoring future cash flows and liquidity on a daily basis. The Bank has developed internal control processes and contingency plans for managing liquidity risk. This incorporates an assessment of expected cash flows and the availability of high grade collateral which could be used to secure additional funding, if required.

Management of liquidity risk

Market Risk Management Policy and the ALM Policy of the Bank approved by the Board of Directors set the tone for managing liquidity risk of the Bank. Liquidity risk of the Bank is given utmost priority when managing a wide range of other risks due to the fact that it is considered as the most critical risk for any financial institution.

The Bank’s Treasury Department is entrusted with managing liquidity of the Bank on real time basis to ensure smooth functioning of business activities of all other business units of the Bank.

Having access to a substantial stable Current Account and Savings Account (CASA) base due to its wide branch network and the top of the mind perception created in the depositors in general, for stability provides immense strength to the Bank in managing liquidity.

Having high quality liquid assets at the disposal of the Bank is another plus factor for the Bank. The strength of such was amply reflected in the Basel III computation the Bank carries out for arriving at Liquidity Coverage Ratio and Net Stable Funding Ratio as per the CBSL Directions that recorded very healthy results as compared to regulatory minimum threshold levels.

The Bank has experienced accumulation of liquidity above the minimum regulatory requirements as a result of slowness of economic performance of the country in 2019. However, the Bank has adopted many strategies to invest excess liquidity at optimum yields and thereby to minimise the negative impact on the bottom line.

Contingency funding plans in force, constant monitoring of salient liquidity ratios and scenario based stress testing being carried out regularly, provide the sense of Bank with required indicators enabling the Bank to take proactive measures that could provide time to overcome any adverse liquidity position on a future date.

Operational risk

The risk that the Bank will incur a loss due to systems failure, human error, fraud or external events. When controls fail to operate effectively, operational risks can cause damage to reputation, have legal or regulatory implications or lead to financial loss. The Bank cannot expect to eliminate all operational risks, but it endeavours to manage these risks through a control framework and by monitoring and responding to potential risks.

Controls include effective segregation of duties, access, authorisation and reconciliation procedures, staff education and assessment processes, such as the use of internal audit.

Management of operational risk

Sound Operational Risk Management practices are embedded into the work process through the Bank’s culture, internal policy framework and as per regulatory requirements.

Circular instructions and Operational Risk Management Policy play a major part in bringing together business practices with accepted benchmarks to ensure minimum disruption to processes, personnel, technology and infrastructure.

Internal control framework and audit function with firmly established “three lines of defences” serve the Bank to manage operational risk at current acceptable levels.

IT Risk of the Bank is managed through strict monitoring of Key IT Risk Indicators while Vulnerability Assessment and Penetration Tests are being carried out by both internal and external parties at regular intervals to identify the relevant risks.

Refer Note 69 for “Financial Risk Review”.

A detailed write-up on how the risk management is carried out within the Bank’s Risk Management Framework with due consideration given to factors such as governance, identification, assessment, monitoring, reporting and mitigation are discussed in the Section on “Risk Governance and Management”. The said write-up does not form part of the Financial Statements.

“Fair value” is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date in the principal or, in its absence, the most advantageous market to which the Group has access at that date. The fair value of a liability reflects its non-performance risk.

When one is available, the Group measures the fair value of an instrument using the quoted price in an active market for that instrument. A market is regarded as active if transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis.

If there is no quoted pricing in an active market, then the Group uses valuation techniques that maximise the use of relevant observable inputs and minimise the use of unobservable inputs. The chosen valuation technique incorporates all of the factors that market participants would take into account in pricing a transaction.

The fair value of an asset or a liability is measured using the assumptions that market participants would use the fair value hierarchy when pricing the asset or liability, assuming that market participants act in their economic best interest.

The Group recognises transfers between levels of the fair value hierarchy as of the end of the reporting period during which the change has occurred.

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use. External professional valuers are involved for valuation of significant assets such as land and building.

An analysis of fair value measurement of financial and non-financial assets and liabilities is provided in Note 27.

The Group has consistently applied the Accounting Policies as set out in Notes 6 to 10 to all periods presented in these Financial Statements, except for changes arising out of transition to SLFRS 16 as set out below:

5.1 New and amended standards and interpretations

In these Financial Statements, the Group has applied SLFRS 16, which is effective for the annual reporting periods beginning on or after January 1, 2019 for the first time. The Group has not early adopted any other accounting standard, interpretation or amendment that has been issued but not effective.

5.1.1 SLFRS 16 – Leases

SLFRS 16 issued in 2016, supersedes LKAS 17, IFRIC 4 on “Determining whether an arrangement contains a Lease”, SIC-15 on “Operating Leases – Incentives” and SIC-27 on “Evaluating the substance of transactions involving the legal form of a lease”. SLFRS 16 sets out the principles for the recognition, measurement, presentation, and disclosure of leases and requires lessees to recognise most leases on the SOFP.

One of the most notable aspects of SLFRS 16 is that the lessee and lessor accounting models are asymmetrical. SLFRS 16 has retained LKAS 17’s finance lease/operating lease distinction for lessors but this distinction is no longer relevant for lessees. Hence, the changes introduced in SLFRS 16 are not significant in respect of contracts in which the Group is the lessor. However, SLFRS 16 has introduced fundamental changes to accounting principles when the Group becomes the lessee of the contract.

The Group adopted SLFRS 16 using the modified retrospective method of adoption with the date of initial application being January 1, 2019. Under this method, the standard is applied retrospectively with the cumulative effect of initially applying the standard being recognised at the date of initial application. Due to the adoption of SLFRS 16, deferred tax asset created under LKAS 17 on the liability of straight lining of lease rentals has been transferred directly to equity as of January 1, 2019.

The Group recognises a lease liability at the date of initial application for leases previously classified as operating leases applying LKAS 17. The lessee shall measure that lease liability at the present value of the remaining lease payments, discounted using the lessee’s IBR at the date of initial application.

The Group recognises as right-of-use asset at the date of initial application for leases previously classified as operating leases applying LKAS 17. The Group opted to measure the right-of-use asset at an amount equal to the lease liability, on a lease-by-lease basis, adjusted by the amount of any prepaid or accrued lease payments relating to that lease recognised in the SOFP immediately before the date of initial application.

The key changes of SLFRS 16 are as set out below:

5.1.1.1 Changes to identification of leases

SLFRS 16 has changed the recognition of leases by replacing the ‘risk and reward’ model in LKAS 17 with a ‘right-of-use’ model for lessees. The Group determines whether a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration.

SLFRS 16 introduces a single on-balance sheet model for lessees similar to the accounting for finance lease under LKAS 17. Accordingly, leases within the scope of SLFRS 16 are brought on to the balance sheet recognising a ‘right-of-use’ asset and related lease liability. As a result, the portion of off-balance sheet finance kept in the form of operating lease is recognised on balance sheet, except for short-term leases (lease term 12 months or less) and leases of low value.

5.1.1.2 Separating components of a contract

The Group determines, the right to use an underlying asset is a separate lease component if both of the following criteria are met.

- The lessee can benefit from use of the asset either on its own or together with other resources that are available to the lessee.

- The underlying asset is neither dependent on, nor highly interrelated with, the other underlying assets in the contract.

For contracts in which the Group becomes the lessee, the consideration in the contract is allocated to each lease component on the basis of the relative standalone price of the lease component and the aggregate standalone price of the non-lease components. On the other hand, when the Group is the lessor, the guidance given in Sri Lanka Accounting Standard – SLFRS 15 on “Revenue from Contracts with Customers” (SLFRS 15) is applied to allocate transaction price to separate components.

5.1.1.3 Determination of lease term

All lease liabilities are to be measured with reference to the estimate of lease term. Accordingly, the Group determines the lease term as the non-cancellable period of a lease, together with both periods covered by an option to extend the lease if the Group is reasonably certain to exercise that option; and periods covered by an option to terminate the lease if the Group is reasonably certain not to exercise that option. In this assessment, the Group considers all relevant facts and circumstances that create an economic incentive for the Group to exercise the option to extend the lease, or not to exercise the option to terminate the lease.

The Group reassesses whether it is reasonably certain to exercise an extension option, or not to exercise a termination option, only upon the occurrence of a significant event or significant change in circumstances that are within the control of the Group as a lessee. In addition, as per SLFRS 16, the Group revises lease term only if there is a change in the non-cancellable period of lease.

Significant accounting policies

The Significant Accounting Policies set out below have been applied consistently to all periods presented in the Financial Statements of the Group except as specified in Note 2.11.

These Accounting Policies have been applied consistently by Group entities.

Set out below is an index of Significant Accounting Policies, the details of which are available on the pages that follow:

Index of significant accounting policies

Table – 28

| Note | Description | Reference to the Notes in Financial Statements |

| 6. | Significant accounting policies – General | |

| 6.1 | Basis of consolidation | |

| 6.2 | Foreign currency | |

| 7. | Significant accounting policies – Recognition of assets and liabilities | |

| 7.1 | Financial instruments – Initial recognition, classification and subsequent measurement |

26 |

| 7.2 | Non-current assets held for sale and disposal groups | |

| 7.3 | Property, plant and equipment | 39 |

| 7.4 | Investment property | 40 |

| 7.5 | Intangible assets | 41 |

| 7.6 | Impairment of non-financial assets | 37 |

| 7.7 | Dividends payable | 25 |

| 7.8 | Employee benefits | 50.2 to 50.5 |

| 7.9 | Other liabilities | 50 |

| 7.10 | Restructuring | |

| 7.11 | Onerous contracts | |

| 7.12 | Bank levies | |

| 7.13 | Financial guarantees, letters of credit and undrawn loan commitments | 59 |

| 7.14 | Commitments | 59 |

| 7.15 | Contingent liabilities and commitments | 59 |

| 7.16 | Stated capital and reserves | 53, 55, 56 & 57 |

| 7.17 | Earnings per Share (EPS) | 24 |

| 7.18 | Operating segments | 63 |

| 7.19 | Fiduciary assets | |

| 8. | Significant accounting policies – Recognition of income and expense | |

| 8.1 | Interest income and expense | 13 |

| 8.2 | Fee and commission income and expense | 14 |

| 8.3 | Net gains/(losses) from trading | 15 |

| 8.4 | Net gains/ (losses) from derecognition of financial assets | 16 |

| 8.5 | Dividend income | 15 & 17 |

| 8.6 | Leases | 34.3, 39 & 50.1 |

| 8.7 | Rental income and expense | 17 & 21 |

| 9. | Significant accounting policies – Tax Expense | |

| 9.1 | Income tax expense | 23, 43 & 49 |

| 9.2 | Crop Insurance Levy (CIL) | |

| 9.3 | Withholding tax (WHT) on dividends distributed by the Bank, subsidiaries, and associates |

25 |

| 9.4 | Economic Service Charge (ESC) | |

| 9.5 | Value Added Tax on financial services (VAT FS) | 22 |

| 9.6 | Nation Building Tax on financial services (NBT FS) | 22 |

| 9.7 | Debt Repayment Levy on financial services (DRL FS) | 22 |

| 10. | Significant accounting policies – Statement of Cash Flows | |

| 10.1 | Statement of Cash Flows |

6.1 Basis of consolidation

The Group’s Financial Statements comprise, Consolidated Financial Statements of the Bank and its Subsidiaries in terms of the Sri Lanka Accounting Standard – SLFRS 10 on “Consolidated Financial Statements” (SLFRS 10) and the proportionate share of the profit or loss and net assets of its Associates in terms of the Sri Lanka Accounting Standard – LKAS 28 on “Investments in Associates and Joint Ventures” (LKAS 28). The Bank’s Financial Statements comprise the amalgamation of the Financial Statements of the Domestic Banking Unit, the Offshore Banking Centre and the international operations of the Bank.

6.1.1 Business combinations

Business combinations are accounted for using the acquisition method when control is transferred to the Group as per Sri Lanka Accounting Standard – SLFRS 3 on “Business Combinations” (SLFRS 3). The consideration transferred in the acquisition and identifiable net assets acquired are measured at fair value. Any goodwill that arises is tested annually for impairment (Refer Note 7.6). Any gain on a bargain purchase is recognised in profit or loss immediately. Transaction costs are expensed as incurred, except if they are related to the issue of debt or equity securities.

The consideration transferred does not include amounts related to the settlement of pre-existing relationships. Such amounts are generally recognised in profit or loss.

Any contingent consideration is measured at fair value at the date of acquisition. If an obligation to pay contingent consideration that meets the definition of a financial instrument is classified as equity, then it is not re-measured and settlement is accounted for within equity. Otherwise, subsequent changes in the fair value of the contingent consideration are recognised in profit or loss.

6.1.2 Non-Controlling Interests (NCI)

Details of NCI are given in Note 58.

6.1.3 Subsidiaries

Details of the Bank’s subsidiaries, how they are accounted in the Financial Statements of the Bank and their contingencies are set out in Notes 37 and 59.4 (a).

6.1.4 Loss of control

When the Group loses control over a subsidiary, it derecognises the assets and liabilities of the subsidiary, and any related NCI and other components of equity. Any resulting gain or loss is recognised in profit or loss. Any interest retained in the former subsidiary is measured at fair value when control is lost.

Subsequently, it is accounted for as an Associate or in accordance with the Group’s Accounting Policy for financial instruments depending on the level of influence retained.

6.1.5 Associates

Details of associates, how they are accounted in the Financial Statements of the investee, together with their fair values and the Group’s share of contingent liabilities of such associates are set out in Notes 38 and 59.4 (b).

6.1.6 Transactions eliminated on consolidation

Intra-group balances, transactions and any unrealised income and expenses (except for foreign currency transaction gains or losses) arising from intra-group transactions are eliminated in preparing the Consolidated Financial Statements. Unrealised gains arising from transactions with equity accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealised losses are eliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

6.1.7 Material gains or losses, provisional values or error corrections

There were no material gains or losses, provisional values or error corrections recognised during the year in respect of business combinations that took place in previous periods.

6.2 Foreign currency

6.2.1 Foreign currency transactions and balances

Foreign currency transactions are translated into the functional currency, which is Sri Lankan Rupees, using the exchange rates prevailing at the dates of the transactions. In this regard, the Bank’s practice is to use the middle rate of exchange ruling at the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies as at the reporting date are translated into the functional currency at the middle exchange rate of the functional currency ruling as at the reporting date. The foreign currency gain or loss on monetary items is the difference between amortised cost in the functional currency as at the beginning of the year adjusted for effective interest and payments during the year and the amortised cost in foreign currency translated at the exchange rate as at the reporting date.

Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are translated into the functional currency at the spot exchange rate at the date that the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate as at the date of the transaction.

Foreign currency differences arising on translation are generally recognised in profit or loss. However, foreign currency differences arising from the translation of the following items are recognised in OCI:

- Equity instruments measured at fair value through other comprehensive income

- A financial liability designated as a hedge of the net investment in a foreign operation to the extent that the hedge is effective; and

- Qualifying cash flow hedges to the extent that the hedge is effective.

6.2.2 Foreign currency translations

The Group’s Consolidated Financial Statements are presented in Sri Lankan Rupees, which is also the Bank’s Functional Currency. The Financial Statements of the Offshore Banking Centre of the Bank and the Financial Statements of the foreign operations of the Bank have been translated into the Group’s Presentation Currency as explained under Notes 6.2.3 and 6.2.4 below.

6.2.3 Transactions of the offshore banking centre

These are recorded in accordance with Note 6.2.1 above, except the application of the annual weighted average exchange rate for translation of the Income Statement and the Statement of Profit or Loss and Other Comprehensive Income. Net gains and losses are dealt through the profit or loss.

6.2.4 Foreign operations

The results and financial position of foreign operations that have a functional currency different from the Bank’s presentation currency are translated into the Bank’s presentation currency as follows:

- Assets and liabilities, including goodwill and fair value adjustments arising on acquisition, are translated at the rates of exchange ruling as at the reporting date.

- Income and expenses are translated at the average exchange rate for the period, unless this average rate is not a reasonable approximation of the rate prevailing at the transaction date, in which case income and expenses are translated at the exchange rates ruling at the transaction date.

- All resulting exchange differences are recognised in the OCI and accumulated in the Foreign Currency Translation Reserve (Translation Reserve), which is a separate component of Equity, except to the extent that the translation difference is allocated to the NCI.

When a foreign operation is disposed of such that the control is lost, the cumulative amount in the translation reserve related to that foreign operation is reclassified to profit or loss as part of the gain or loss on disposal. If the Group disposes of only part of its interest in a subsidiary that includes a foreign operation while retaining control, then the relevant proportion of the cumulative amount of the translation reserve is re-attributed to NCI.

7.1 Financial instruments – initial recognition, classification and subsequent measurement

7.1.1 Date of recognition

The Group initially recognises loans and advances, deposits and subordinated liabilities, etc., on the date on which they are originated. All other financial instruments (including regular-way purchases and sales of financial assets) are recognised on the trade date, which is the date on which the Group becomes a party to the contractual provisions of the instrument.

7.1.2 Initial measurement of financial instruments

The classification of financial instruments at initial recognition depends on their cash flow characteristics and the business model for managing the instruments. Refer Notes 7.1.3 and 7.1.4 for further details on classification of financial instruments.

A financial asset or financial liability is measured initially at fair value plus or minus transaction costs that are directly attributable to its acquisition or issue, except in the case of financial assets and financial liabilities at fair value through profit or loss as per SLFRS 9 and trade receivables that do not have a significant financing component as defined by SLFRS 15.

Transaction cost in relation to financial assets and financial liabilities at fair value through profit or loss are dealt with through the Income Statement.

Trade receivables that do not have significant financing component are measured at their transaction price at initial recognition as defined in SLFRS 15.

When the fair value of financial instruments (except trade receivables that do not have significant financing component) at initial recognition differs from the transaction price, the Group accounts for the Day 1 profit or loss, as described below.

7.1.2.1 “Day 1” profit or loss

When the transaction price of the instrument differs from the fair value at origination and fair value is based on a valuation technique using only inputs observable in market transactions, the Group recognises the difference between the transaction price and fair value in net gains/(losses) from trading. In those cases, where the fair value is based on models for which some inputs are not observable, the difference between the transaction price and the fair value is deferred and is only recognised in profit or loss when the inputs become observable, or when the instrument is derecognised. The “Day 1 loss” arising in the case of loans granted to employees at concessionary rates under uniformly applicable schemes is deferred and amortised using Effective Interest Rates (EIR) in “Interest income” and “Personnel expenses” over the remaining service period of the employees or tenure of the loan whichever is shorter.

Refer Notes 13 and 19.

7.1.3 Classification and subsequent measurement of financial assets

As per SLFRS 9, the Group classifies all of its financial assets based on the business model for managing the assets and the assets’ contractual terms measured at either;

- Amortised cost

- Fair value through other comprehensive income (FVOCI)

- Fair value through profit or loss (FVTPL)

The subsequent measurement of financial assets depends on their classification.

7.1.3.1 Business model assessment

The Group makes an assessment of the objective of a business model in which an asset is held at a portfolio level and not assessed on instrument-by-instrument basis because this best reflects the way the business is managed and information is provided to management. The information considered includes:

- the stated policies and objectives for the portfolio and the operation of those policies in practice. In particular, whether management’s strategy focuses on earning contractual interest revenue, maintaining a particular interest rate profile, matching the duration of the financial assets to the duration of the liabilities that are funding those assets or realising cash flows through the sale of the assets;

- how the performance of the portfolio is evaluated and reported to the Bank’s management;

- the risks that affect the performance of the business model (and the financial assets held within that business model) and how those risks are managed;

- how managers of the business are compensated – e.g. whether compensation is based on the fair value of the assets managed or the contractual cash flows collected; and

- the frequency, volume and timing of sales in prior periods, the reasons for such sales and its expectations about future sales activity. However, information about sales activity is not considered in isolation, but as part of an overall assessment of how the Bank’s stated objective for managing the financial assets is achieved and how cash flows are realized.

The business model assessment is based on reasonably expected scenarios without taking “worst case” or “stress case” scenarios into account. If cash flows after initial recognition are realised in a way that is different from the Bank's original expectations, the Bank does not change the classification of the remaining financial assets held in that business model, but incorporates such information when assessing newly originated or newly purchased financial assets going forward.

7.1.3.2 Assessment of whether contractual cash flows are solely payments of principal and interest (SPPI test)

As a second step of its classification process the Group assesses the contractual terms of financial assets to identify whether they meet the SPPI test.

For the purposes of this assessment, “principal” is defined as the fair value of the financial asset on initial recognition and may change over the life of the financial asset (for example, if there are repayments of principal or amortisation of the premium/discount).

“Interest” is defined as consideration for the time value of money and for the credit risk associated with the principal amount outstanding during a particular period of time and for other basic lending risks and costs, as well as profit margin.

In contrast, contractual terms that introduce a more than de minimis exposure to risks or volatility in the contractual cash flows that are unrelated to a basic lending arrangement do not give rise to contractual cash flows that are solely payments of principal and interest on the principal amount outstanding. In such cases, the financial asset is required to be measured at FVTPL.

In assessing whether the contractual cash flows are solely payments of principal and interest on principal amount outstanding, the Group considers the contractual terms of the instrument. This includes assessing whether the financial asset contains a contractual term that could change the timing or amount of contractual cash flows such that it would not meet this condition. In making the assessment, the Group considers:

- contingent events that would change the amount and timing of cash flows;

- leverage features;

- prepayment and extension terms;

- terms that limit the Group’s claim to cash flows from specified assets; and

- features that modify consideration of the time value of money.

The Group holds a portfolio of long-term fixed rate loans for which the Group has the option to propose to revise the interest rate at periodic reset dates. These reset rights are limited to the market rate at the time of revision. The borrowers have an option to either accept the revised rate or redeem the loan at par without penalty. The Group has determined that the contractual cash flows of these loans are solely payments of principal and interest because the option varies the interest rate in a way that is consideration for the time value of money, credit risk, other basic lending risks and costs associated with the principal amount outstanding.

Refer Notes 7.1.3.3 to 7.1.3.5 below for details on different types of financial assets recognised on the SOFP.

7.1.3.3 Financial assets measured at amortised cost

A financial asset is measured at amortised cost if it meets both of the following conditions and is not designated as at FVTPL:

- The asset is held within a business model whose objective is to hold assets to collect contractual cash flows; and

- The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Financial assets measured at amortised cost are given in Notes 7.1.3.3.1 to 7.1.3.3.6 below:

7.1.3.3.1 Loans and advances to banks and other customers

Loans and advances to banks and other customers include amounts due from banks, loans and advances and lease receivables of the Group.

Details of “Loans and advances to banks and other customers” are given in Notes 33 and Note 34.

7.1.3.3.2 Securities purchased under resale agreements (reverse repos)

When the Group purchases a financial asset and simultaneously enters into an agreement to resale the asset (or a similar asset) at a fixed price on a future date (reverse repo), the arrangement is accounted for as a financial asset in the SOFP reflecting the transaction’s economic substance as a loan granted by the Group. Subsequent to initial recognition, these securities issued are measured at amortised cost using the EIR with the corresponding interest income/ receivable being recognised as interest income in profit or loss.

Details of “Securities purchased under resale agreements” are given in the SOFP.

7.1.3.3.3 Debt and other financial instruments measured at amortised cost

Details of “Debt and other financial instruments measured at amortised cost” are given in Note 35.

7.1.3.3.4 Cash and cash equivalents

Details of “Cash and cash equivalents” are given in Note 28.

7.1.3.3.5 Balances with central banks

Details of “Balances with central banks” are given in Note 29..

7.1.3.3.6 Placements with banks

Details of “Placements with banks” are given in Note 30.

7.1.3.4 Financial assets measured at FVOCI

Financial assets at FVOCI include debt and equity instruments measured at fair value through other comprehensive income.

For financial assets measured at FVOCI refer Notes 7.1.3.4.1 and 7.1.3.4.2.

7.1.3.4.1 Debt instruments measured at FVOCI

Debt instruments are measured at FVOCI if they are held within a business model whose objective is to hold for collection of contractual cash flows and selling financial assets, where the asset’s contractual cash flows represent payments that are solely payments of principal and interest on principal outstanding. Details of “Debt instruments at FVOCI” are given in Note 36.

7.1.3.4.2 Equity instruments designated at FVOCI

Upon initial recognition, the Group elects to classify irrevocably some of its equity instruments held for strategic and regulatory purposes as equity instruments at FVOCI. Details of “Equity instruments at FVOCI” are given in Note 36.

7.1.3.5 Financial assets measured at FVTPL

All financial assets other than those classified at amortised cost or FVOCI are classified as measured at FVTPL. Financial assets measured at FVTPL include financial assets that are held for trading or managed and whose performance is evaluated on a fair value basis are measured at FVTPL because they are neither held to collect contractual cash flows nor held both to collect contractual cash flows and to sell financial assets. Financial assets measured at FVTPL are discussed in Notes 7.1.3.5.1 and 7.1.3.5.2 below.

7.1.3.5.1 Financial assets held for trading

Details of “Financial Assets held for trading” are given in Note 32.

7.1.3.5.1.1 Derivatives recorded at FVTPL

Details of “Derivative financial assets” recorded at fair value through profit or loss are given in Note 31.

7.1.3.5.2 Financial assets designated FVTPL

On initial recognition, the Group may irrevocably designate a financial asset that otherwise meets the requirements to be measured at amortised cost or at FVOCI as at FVTPL when such designation eliminates or significantly reduces an accounting mismatch that would otherwise arise from measuring the assets or liabilities or recognising gains or losses on them on a different basis.

Financial assets designated at FVTPL are recorded in the SOFP at fair value. Changes in fair value are recorded in “Net gain or loss on financial assets and liabilities designated at FVTPL”. Interest earned is accrued in “Interest Income”, using the EIR, while dividend income is recorded in “Other operating income” when the right to receive the payment has been established.

The Group has not designated any financial assets upon initial recognition as at FVTPL as at the end of the reporting period.

7.1.4 Classification and subsequent measurement of financial liabilities

The Group classifies financial liabilities, other than financial guarantees and loan commitments into one of the following categories:

- Financial liabilities at FVTPL, and within this category as –

- Held-for-trading; or

- Designated at FVTPL;

- Financial liabilities measured at amortised cost.

The subsequent measurement of financial liabilities depends on their classification.

Refer Notes 7.1.4.1 and 7.1.4.2 as detailed below:

7.1.4.1 Financial liabilities at FVTPL

Financial liabilities at FVTPL include financial liabilities held for trading and financial liabilities designated upon initial recognition as at FVTPL. Refer Notes 7.1.4.1.1 and 7.1.4.1.2 below.

7.1.4.1.1 Financial liabilities held for trading

Details of “Derivative financial liabilities” classified under financial liabilities held for trading are given in Note 46.

7.1.4.1.2 Financial liabilities designated at FVTPL

Financial liabilities designated at FVTPL are recorded in the SOFP at fair value when

- The designation eliminates, or significantly reduces, the inconsistent treatment that would otherwise arise from measuring the assets or liabilities or recognising gains or losses on them on a different basis, or

- A group of financial liabilities or financial assets and financial liabilities is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information about the group is provided on that basis to entity’s key management personnel, or

- The liabilities containing one or more embedded derivatives, unless they do not significantly modify the cash flows that would otherwise be required by the contract, or it is clear with little or no analysis when a similar instrument is first considered that separation of the embedded derivative(s) is prohibited.

Changes in fair value are recorded in “Net fair value gains/ (losses) from financial instruments at FVTPL” with the exception of movements in fair value of liabilities designated at FVTPL due to changes in the Bank’s own credit risk. Such changes in fair value are recorded in the own credit reserve through OCI and do not get recycled to profit or loss. Interest paid/payable is accrued in “Interest expense”, using the EIR.

The Group has not designated any financial liabilities as at FVTPL as at the end of the reporting period.

7.1.4.2 Financial liabilities at amortised cost

Financial liabilities issued by the Group that are not designated at FVTPL are classified as financial liabilities at amortised cost under “Due to banks”, “Due to depositors”, “Securities sold under repurchase agreements”, “Other borrowings” or “Subordinated liabilities” as appropriate, where the substance of the contractual arrangement results in the Group having an obligation either to deliver cash or another financial asset to the holder, or to satisfy the obligation other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of own equity shares. The Group classifies capital instruments as financial liabilities or equity instruments in accordance with the substance of the contractual terms of the instrument.

After initial recognition, such financial liabilities are subsequently measured at amortised cost using the EIR method. Amortised cost is calculated by taking into account any discount or premium on acquisition and fee or costs that are an integral part of the EIR.

The EIR amortisation is included in “Interest expense” in the Income Statement. Gains and losses too are recognised in the Income Statement when the liabilities are derecognised as well as through the EIR amortisation process.

7.1.4.2.1 Due to banks

Details of “Due to banks” are given in Note 45.

7.1.4.2.2 Due to depositors

Details of “Due to depositors” are given in Note 47.

7.1.4.2.3 Securities sold under repurchase agreements (repos)

When the Group sells a financial asset and simultaneously enters into an agreement to repurchase the asset (or a similar asset) at a fixed price on a future date (repos), the arrangement is accounted for as a financial liability in the SOFP reflecting the transaction’s economic substance as a deposit. Subsequent to initial recognition, these securities are measured at amortised cost using the EIR with the corresponding interest payable being recognised as interest expense in profit or loss.

Details of “Securities sold under repurchase agreements (repos)” are given in the SOFP.

7.1.4.2.4 Other Borrowings

Details of “Other Borrowings” are given in Note 48.

7.1.4.2.5 Subordinated liabilities

Details of “Subordinated liabilities” are given in Note 52.

7.1.5 Derivatives held for risk management purposes and hedge accounting

Derivatives held for risk management purposes include all derivative assets and liabilities that are not classified as trading assets and liabilities. Derivatives held for risk management purposes are measured at fair value in the SOFP.

The Group designates certain derivatives held for risk management as well as certain non-derivative financial instruments as hedging instruments in qualifying hedging relationships. On initial designation of the hedge, the Group formally documents the relationship between the hedging instrument and hedged item, including risk management objective and strategy in undertaking the hedge, together with the method that will be used to assess the effectiveness of the hedging relationship. The Group makes an assessment, both at inception of the hedge relationship and on an ongoing basis, of whether the hedging instrument is expected to be highly effective in offsetting the changes in fair value or cash flow of the respective hedged item during the period for which the hedge is designated, and whether the actual results of each hedge are within a range of 80% to 125%. The Group makes an assessment for a cash flow hedge of a forecast transaction, of whether the forecast transaction is highly probable to occur and presents an exposure to variations in cash flows that could ultimately affect profit or loss.

The Group currently uses cash flow hedging relationships for risk management purposes as discussed in Notes 7.1.5.1 to 7.1.5.5 below:

7.1.5.1 Fair value hedges

When a derivative is designated as the hedging instrument in a hedge of the change in fair value of a recognised asset or liability or a firm commitment that could affect the profit or loss, changes in the fair value of the derivative are recognised immediately in profit or loss in the same line item as the hedged item that is attributable to the hedged risk.

If the hedging derivative expires or is sold, terminated or exercised, or the hedge no longer meets the criteria for fair value hedge accounting, or the hedge designation is revoked, then hedge accounting is discontinued prospectively. However, if the derivative is novated to a central counterparty by both parties as a consequence of laws or regulations without changes in its terms except for those are necessary for the novation, then the derivative is not considered as expired or terminated.

Any adjustment up to the point of discontinuation to a hedged item for which the effective interest method is used is amortised to profit or loss as part of the recalculated EIR of the item over its remaining life.

7.1.5.2 Cash flow hedges

When a derivative is designated as the hedging instrument in a hedge of the variability in cash flows attributable to a particular risk associated with a recognised asset or liability that could affect the profit or loss, the effective portion of changes in the fair value of the derivative are recognised in OCI and presented in the hedging reserve within equity. Any ineffective portion of changes in the fair value of the derivative is recognised immediately in profit or loss.

The amount recognised in OCI is reclassified to profit or loss as a reclassification adjustment in the same period as the hedged cash flows affect profit or loss, and in the same line item in the Statement of Profit or Loss and OCI.

If the hedging derivative expires or is sold, terminated or exercised, or the hedge no longer meets the criteria for cash flow hedge accounting, or the hedge designation is revoked, then hedge accounting is discontinued prospectively. However, if the derivative is novated to a central counterparty by both parties as a consequence of laws or regulations without changes in its terms except for those are necessary for the novation, then the derivative is not considered as expired or terminated.

Details of “Cash flow hedges” are given in Note 31.1 and Note 46.1.

7.1.5.3 Net investment hedges

When a derivative instrument or a non-derivative financial liability is designated as the hedging instrument in a hedge of a net investment in a foreign operation, the effective portion of changes in the fair value of the hedging instrument is recognised in OCI and presented in the translation reserve within equity. Any ineffective portion of changes in the fair value of the derivative is recognized immediately in profit or loss. The amount recognised in OCI is reclassified to profit or loss as a reclassification adjustment on disposal of the foreign operation.

7.1.5.4 Other non-trading derivatives