Global economy

Global growth was estimated at 2.9% for 2019, representing a significant drop from 3.7% in 2018. This downturn can be traced to a unique confluence of factors. Much of 2019 was defined by the intermittent trade conflict between China and the United States – and heightened trade, social and geopolitical tensions more generally. These tensions have raised concerns and anxieties around the future of established global trading systems and patterns of international cooperation; in turn, business confidence eroded and market sentiment flagged throughout the year. Apart from influencing conditions in the United States and China, these tensions have had spillover effects across the Euro areas and advanced Asian economies, including Hong Kong, Korea, and Singapore.

The impacts on manufacturing and global trade, in particular, have been acute. Weaker external demand has seen a broad-based slowdown in industrial output, and manufacturing declined to levels not seen since the global financial crisis. The services sector across much of the globe, however, continued to remain strong, bolstering labour markets and supporting healthy wage growth in advanced economies, particularly in the United States.

In addition to these pressures, emerging market economies were bedevilled by a range of idiosyncratic factors causing macroeconomic strain. Large emerging economies like Argentina, Iran, Turkey, and Venezuela faced significant economic distress, while countries like Brazil, Mexico, Russia and Saudi Arabia underperformed in comparison to their recent averages. Growth in India, too, slowed, weighed down by corporate and environmental regulatory uncertainty. In addition to the macroeconomic repercussions of the trade conflict, China implemented regulatory measures to rein in debt – all contributing to a growth of 6.1%, its lowest figure in 29 years.

Notably, the United States as well as many other advanced and emerging market economies made a pronounced shift towards increased monetary easing, reversing the trend towards tightening in 2018. The US Federal Reserve, in particular, cut interest rates three times in a span of four months ending October 2019. This accommodative strategy has served to cushion the negative impacts of the US-China trade tensions.

Overview of the world economic outlook projections

Table – 06

| Estimated | Projected | |||

| 2018 % | 2019 % | 2020 % | 2021 % | |

| World output | 3.6 | 2.9 | 3.3 | 3.4 |

| Advanced economies | 2.2 | 1.7 | 1.6 | 1.6 |

| United States | 2.9 | 2.3 | 2.0 | 1.7 |

| Euro Area | 1.9 | 1.2 | 1.3 | 1.4 |

| Japan | 0.3 | 1.0 | 0.7 | 0.5 |

| United Kingdom | 1.3 | 1.3 | 1.4 | 1.5 |

| Emerging market and developing economies | 4.5 | 3.7 | 4.4 | 4.6 |

| China | 6.6 | 6.1 | 6.0 | 5.8 |

| India | 6.8 | 4.8 | 5.8 | 6.5 |

| ASEAN-5 | 5.2 | 4.7 | 4.8 | 5.1 |

| Russia | 2.3 | 1.1 | 1.9 | 2.0 |

Source: IMF World Economic Outlook Update January 2020

Sri Lankan economy

The pressures of these global developments, coupled with a turbulent domestic environment, posed major challenges to the Sri Lankan economy throughout the year. The growth rate declined from a sub-par 3.2% in 2018 to a troubling 2.8% in 2019. While the legacy effects of tight fiscal and monetary policy, stagnant fixed investment, and flagging aggregate demand carried over from 2018 meant that the conditions were already precarious, the sharp downturn was exacerbated by the unfortunate Easter Sunday attacks and the subsequent climate of political and economic anxiety. The attacks had repercussions across all spheres of economic activity, livelihoods of people and the aftershocks continue to reverberate.

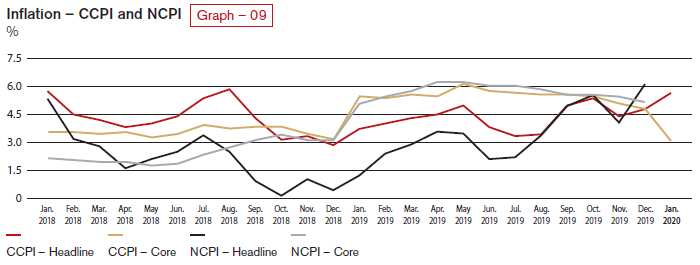

Headline and core inflation remained under control in single digits, but there is concern that these figures are more reflective of weakened aggregate demand and, thus, of a negative output gap denoting an economy performing well below its potential. Nevertheless, forecasts suggest that inflation will hold around 5% in 2020 and beyond.

A marked contraction in imports and a slight increase in exports over the year led to a reduction of the trade deficit from USD 9,642 Mn. to USD 7,214 Mn. (measured from November 2018 – November 2019); this in turn, resulted in a notable contraction of the current account deficit. While tourist arrivals and earnings remained below 2018 levels, the sector showed signs of recovery towards the end of the year, offering some relief from the spillover effects of the Easter Sunday attacks. On the other hand, workers’ remittances declined slightly following trends over the recent past.

Subdued levels of foreign direct investment (FDI) continued to cast a shadow over the financial inflows into the country. Foreign investment in rupee denominated government securities and in the CSE recorded net outflows of USD 234 Mn. and USD 30 Mn., respectively (as of November 2019). In the face of continual current account deficits and inadequate non debt-creating capital inflows, the economy remained reliant on debt-creating facilities. Sri Lanka made two issuances of International Sovereign Bonds (ISBs) in 2019, totaling USD 4.4 Bn. In addition, Sri Lanka successfully underwent the fifth and sixth reviews of the Extended Fund Facility (EFF) of the International Monetary Fund (IMF), consequently receiving the sixth and seventh tranches of disbursements.

The Sri Lankan rupee demonstrated greater stability in foreign exchange markets, and after a substantial depreciation in 2018, appreciated by 0.6% against the USD to close at Rs. 181.75, the first such appreciation since 2010. Gross official reserves are estimated at USD 7.6 billion as of the end of 2019, providing an import cover of 4.6 months.

Sri Lankan banking sector

The macroeconomic environment had major ramifications on the banking sector. A complete assessment of the sector’s performance must begin with trends that emerged in 2018 along with CBSL policy responses to the evolving situation.

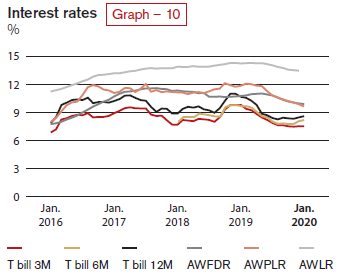

For most of 2018, the CBSL adopted a tight monetary policy, as it had done in the previous year. However, when Open Market Operations proved inadequate to address persistent liquidity deficits in the domestic money market that had taken hold in mid-September 2018, the CBSL reduced the Statutory Reserve Ratio (SRR) applicable on all rupee deposit liabilities of commercial banks from 7.5% to 6.00% in November 2018. In order to counterbalance the effects of the substantial amount of liquidity this measure would release to the banking system – namely, a potential decline in interest rates, excess aggregate demand, and inflationary instability – the CBSL simultaneously raised the Standing Deposit Facility Rate (SDFR) and the Standing Lending Facility Rate (SLFR) to 8.00% and 9.00% respectively. The CBSL reduced the SRR by a further 1.00% in March 2019, and together, these cuts injected approximately Rs. 150 Bn. of additional liquidity into the financial market. These measures represented a subtle shift to a neutral monetary policy stance by the end of 2018 and early 2019.

It is in this context that the turn to an accommodative monetary policy stance in mid-2019 must be understood, when the deterioration in private sector credit growth and asset quality was further exacerbated by the Easter Sunday attacks. Contending that Sri Lanka’s excessively high nominal and real lending rates – especially in comparison to peer economies – were a key reason for the economic slowdown, the CBSL imposed caps on interest rates on Sri Lankan Rupee Deposits in Licensed Commercial Banks (LCBs) and Licensed Specialised Banks (LSBs) in April 2019 in an effort to induce a correlative reduction in lending rates. Similarly, SDFR and SLFR were further reduced by 50 basis points each in May and August 2019.

Despite these adjustments, however, interest rates of lending products remained stubbornly high. To more swiftly and decisively trigger a reduction in market lending rates, the CBSL removed the deposit caps and replaced them with caps on lending rates in September 2019.

The regulations mandated reductions in nominal interest rates on advances, credit card receivables, and weekly Average Weighted Prime Rates (AWPRs). These measures prompted a marked reduction in lending rates towards the end of the year, and credit flows to the private sector increased in December. Policy rates at the end of the year for SDFR, SLFR, and SRR stood at 7.00%, 8.00%, and 5.00%, respectively.

When compared to 2018, however, overall expansion in credit to both private and public sectors in 2019 remained modest. The assets of the sector grew by only 6.18% to reach Rs. 12.50 Tn. as of end 2019, indicating a trend of growth well below the 2018 rate of 14.60%. Total loans and advances grew by 5.58% to reach a total of Rs. 8.12 Tn., also well below 2018 growth rate of 19.60%. Moreover, loans and advances accounted for 64.86% of total assets, compared with a figure of 65.20% for 2018.

The sector experienced a pronounced deterioration in asset quality – from the already high levels witnessed in 2018 – with the gross and net Non-Performing Loans (NPL) ratios of the banking sector rising to 4.70% and 2.80%, respectively, compared with 3.40% and 2.00% at the end of the previous year requiring higher impairment provisions. Deposit growth of the sector, at 7.89%, was well below the growth rate of 14.78% in 2018 and reached Rs. 9.16 Tn. Furthermore, with low deposit rates in effect throughout the year, there was only a marginal decrease in the CASA ratio from 31.97% in 2018 to 31.36% in 2019.

In this difficult scenario, the profitability of the banking sector, understandably, was negatively affected.

Bangladesh economy

With the incumbent Prime Minister, Sheikh Hasina, securing her third consecutive term as prime minister on December 30, 2018, and her Awami League party winning almost every parliamentary seat on offer, the economy of Bangladesh appears to be in a strong, stable position. The current account deficit in USD terms improved further in the first half of the FY 2019-20 (which runs from July 2019 to June 2020), largely propelled by a robust increase of 17.89% of inflows of workers’ remittances. Bangladesh is projecting inward remittances of USD 20 Bn. in 2020 as against USD 18 Bn in 2019. Revenue collection edged up in the first half of FY 2019-20 by 7.30% YOY. Exports for the first half of the FY 2019-20 was USD 19.3 Bn. against USD 25.0 Bn. for the same period in FY 2018-19, indicating a negative growth of 5.84%. This was largely due to a downturn in the garment sector.

For the second half of the FY 2019-20, Bangladesh Bank kept private sector credit growth targets unchanged at 14.80% against the first half performance of around 10.00%. Inflation for the FY 2019-20 was 5.59% against the target of 5.50% which has been maintained at fairly consistent levels over the past several years. Foreign direct investment rose by 19.47% in FY 2018-19, and the FDI flow has maintained a rising trend in recent years. The government is targeting a FDI/GDP ratio of 3.00% for FY 2019-20.

Bangladesh’s GDP grew by 8.15% in the FY 2018-19 against the target of 7.80%, making the country the fastest growing nation in the Asia Pacific region. The higher-than-expected growth came in spite of headwinds from slowing exports and the drying banking sector liquidity. For the FY 2019-20, the GDP is expected to grow at 8.20%. However, risks of natural disasters, a shaky global trade environment and a struggling domestic banking system (with an NPL of around 11%) may cloud prospects.

Standard & Poor’s credit rating for Bangladesh stands at BB- with a stable outlook. Moody’s credit rating for Bangladesh was last set at Ba3 with a stable outlook, while Fitch credit rating was last reported at BB- with a stable outlook.