The backbone of our success has always been our commitment to operational excellence. This commitment is more important in today’s world of heightened competition and flux. Today, the market is more saturated with an array of similar pure banking products and services; what sets an organisation apart is its speed, accuracy, and quality of delivery. Meeting these expectations of the customer while remaining cost efficient is a balancing act that requires us to continuously assess and streamline our processes while making the most productive use of our resources.

The general trend of our efforts during the year under review responds to this environment by placing an emphasis on centralising and automating our back office operations, thus allowing us to reallocate staff and resources towards sales and Customer Relationship Management (CRM). Our efforts and these innovations in centralising our SME credit assessment operations (see Customer Centricity for further details) provides a blueprint for how the Bank needs to evolve going forward.

Our industry leading cost to income ratio has been a long standing hallmark of the Bank’s performance, allowing us to maintain a competitive edge year on year. This year, our cost income ratio reflected our need to dedicate a large number of resources towards managing NPLs and saw an increase from 2018, as indicated below:

- The Bank’s Cost to income ratio (including taxes on financial services) deteriorated to 49.41% from 46.35% in 2018.

- Cost to income ratio (excluding taxes on financial services) deteriorated to 38.51% from 36.85% in 2018.

A Commitment to Continuous Improvement

Service standards

One of the Bank’s major ongoing initiatives is striving for superior service standards. During the year under review, we completed the Stage I audit of ISO/IEC 20000 – the most globally recognised standard for exceptional IT Service Management – and we expect to complete the Stage II audit by February 2020. The implementation of this standard will enable us to deliver IT services more efficiently and effectively, both internally and to our customers, and, in turn, allow us to derive more value from our IT investments. We anticipate being awarded the ISO/IEC 20000 Practitioner Qualification Certificate during 2020.

The Bank also obtained the prestigious Payment Card Industry Data Security Standard (PCI-DSS) v3.2.1 certification after an in-depth assessment from SISA, a global Payment Security Specialist and Qualified Security Assessor. PCI-DSS is the global data security standard adopted by payment card brands for all entities that process, store or transmit cardholder data and sensitive authentication data, and the certification confirms that the Bank follows security best practices in all its card operations. This certification was especially significant in supporting the Bank’s strong card growth during the year despite adverse conditions, and will mitigate the risks of security breaches and data theft as we continue to rapidly expand our card base in the coming years.

The Bank understands the need to continuously strengthen its guard against the foreseeable threats that are rapidly evolving. Going well beyond mere compliance, our effort is to ensure data is protected and customer information is secure at all times. Implementation of the Bank wide “Baseline Security Standard” plan initiated in 2018 is progressing well and is to be completed by 2020. This is to be supplemented with a software solution for data leakage prevention which is being currently evaluated for implementation in 2020.

Plans are underway to strengthen the Disaster Recovery Centre making it more dependable in the time of need. Disaster Recovery Centre akin to the live data centre is tested on a regular basis through well structured and co-ordinated drills to warrant its reliance and the outcome is reported to the CBSL and where shortcomings are observed corrective action is taken to avoid repetition.

Enhancing internal processes

The Bank conducted a range of internal process improvements throughout the year which focused on centralisation and automation, resulting in increased efficiency and productivity in our back office operations. The projects concluded this year include centralising the processing of outward cheque clearing and of transfer cheque handling, the automation of post-dated cheque handling, and the bank-wide digitalisation (scanning) of daily vouchers. Continuing our strategy of having our internal customers lead the way in migrating completely to digital banking, we converted all staff current, savings and credit card accounts to e-statements and the automation of staff loan processing has been completed. We hope to automate the staff housing loans during the year 2020.

This year, in addition, we commenced several major projects. We conducted process mapping and re-engineering exercises at the Imports Department and the Card Centre, replacing the traditional ledger-based customer handling systems with a process automation workflow system. In the Card Centre, these efforts were coupled with upgrading the card management system with the latest version, giving us further functionality for data analytics, customer segmentation and targeted promotion. We also implemented a new foreign exchange rate platform that allows branch and department personnel to request special rates from dealers directly through an online portal.

Furthermore, we continued our forays in the adoption of Robotic Process Automation (RPA). This year we automated the staff USER ID management and CRIB report procurement and analysis. We also conducted a variety of initiatives that will serve as essential precursors to accelerate RPA in 2020, including data cleansing, purging and data repository creation.

Transforming our branch network

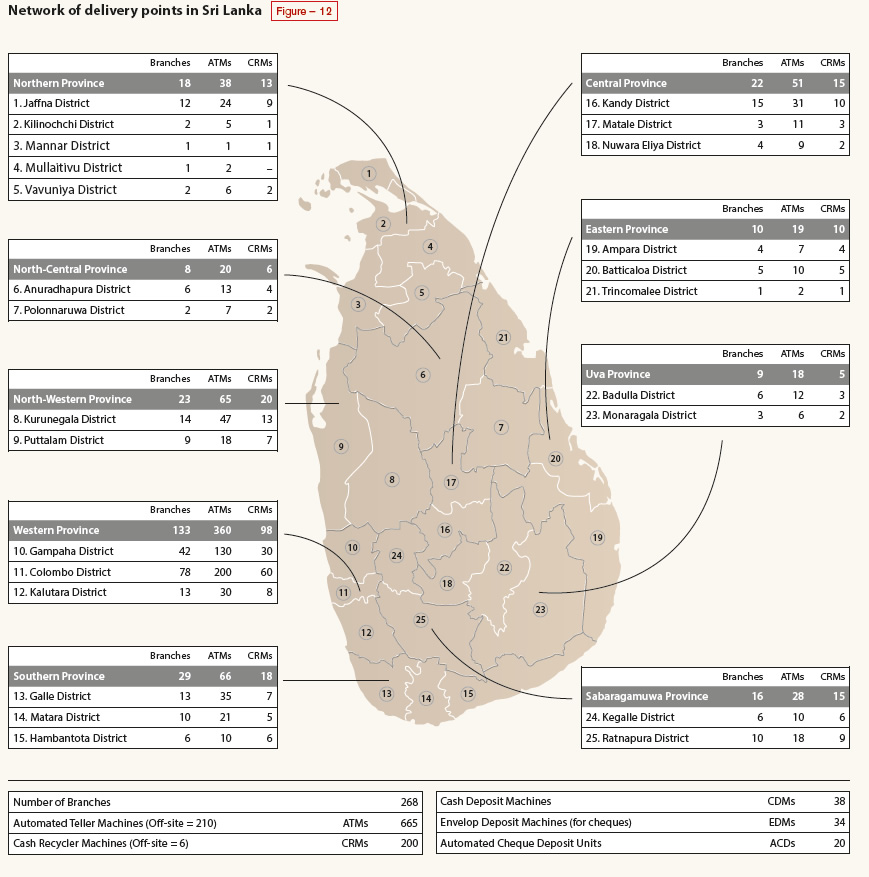

Reflecting our focus on alternate channels and the decision to slow down expansion/consolidate our branch network, we limited the opening of new branches to two, our 266th (Embuldeniya) and 267th (Hettipola). Construction on new buildings for our Jaffna and Trincomalee branches progressed well, as did the refurbishment of our historic Galle branch in the Dutch Fort; all three buildings are scheduled to be opened in 2020 to coincide with our 100th year of operations. Notably, we commissioned a state-of-the-art Automated Banking Centre (ABC) at One Galle Face Mall. Moreover, our ATM and CRM network increased by 35 units this year, bringing our total to 865 units. We are particularly proud of the in-house development of a software tool that helps us monitor and maintain the conditions of our 210 ATMs located outside the branch network. Even at the smallest touch point, we want to provide our customers with the visual sensibility and attention to detail that they expect from the Bank. This tool is provided on a tab to cash officers who can produce a report when they conduct their rounds, which means that no additional staff resources are expended in the monitoring of these ATMs. Service staff can then be deployed efficiently when necessary.

In our efforts to productively allocate our resources, we continued our branch re-organisation and renovation programme that commenced in 2017. Under this programme, we are converting our branches to feature a standardised facade and layout that presents an ABC as the first point of contact with customers as they enter the premises. The ABCs feature Automated Teller Machines (ATM), Cash Recycler Machines (CRM), and Cheque Deposit Machines (CDM), offering customers 24-hour access to the Bank’s services. This layout enables and encourages our customers to conduct a range of transactions conveniently and swiftly without needing to proceed further into the Bank’s interior. With counter traffic drastically reduced, our staff can more efficiently turn their attention to customers with complex or non-conventional banking needs. This year, we renovated 26 branches, bringing the total number of branches with this standardised layout to 114. We have seen a reduction in counter traffic and anticipate a further reduction next year as customers increasingly avail themselves of the convenience of our automated facilities.

To promote digital adoption, we launched Digital Experience Zones at selected branches. These zones have a staff member serving as a Digital Assistant to enroll and familiarise customers with our online and mobile banking facilities. They have proven to be a great success; we find that for customers who may be wary or hesitant of digital banking, an in-person demonstration of the functionality and benefits of our apps instils confidence and generates enthusiasm for digital adoption.

/p>

/p>

Safeguarding the environment

Our efforts at continuous improvement and resource optimisation, along with initiatives to promote digital banking, intrinsically have a positive effect on the natural environment by reducing our carbon footprint. In addition, we place a strong emphasis on managing the direct environmental risks and impacts of our internal operations as part of our ambitious goals of becoming the first bank in Sri Lanka with a carbon neutral business operation by end 2020 and completely paperless operation by 2030.

During the year, we expanded our renewable energy programme by installing solar panels in 13 new branches. This brings our number of branches powered partially or entirely by solar energy to 49.

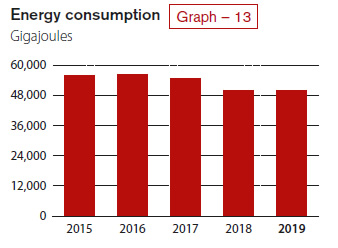

The energy consumption within the organisation saw a marginal increase of 338 gigajoules year-on-year flattening the downward trajectory to record 50,296 gigajoules as opposed to 49,958 gigajoules in 2018. Expansion in the branch network and increased business volumes have contributed to the flattening of the curve. During the year however, the Bank’s exports to the national grid increased to 1,510 gigajoules from 555 gigajoules in 2018, evincing the effectiveness of our renewable energy programme.

A major part of our focus this year was in transforming the culture of sustainability within the Bank. This was important specially for service industries, given their need to provide a superior experience to customers, despite their hesitance to take on such initiatives. This year, we expanded and developed our assessment programme which was introduced in 2018. Under this programme, we meticulously tracked the usage of high-value and high-usage items across our branch network. This provides a holistic picture of the usage of the Bank, and leads to healthy debate and cross-departmental efforts to reduce consumption. A subtle but important aspect of this programme is our publication of ‘Top Ten’ usage lists, which promotes a spirit of positive competition among the staff and best practices throughout the Bank. We also set up a comprehensive e-waste management policy under the rules and guidance of the Ministry of Environment that brings our e-recycling and disposal practices in line with the regulations of the Sri Lanka Data Protection Act.

Investing in Our Employees

Driving our value creation model is our workforce, also referred to, with the utmost respect, as our Human Capital. The latter term is meant to acknowledge that our employees are a resource that needs to be meticulously nourished; just as our 5,062 strong team creates value for the Bank and its stakeholders, the Bank, in turn, is mindful of delivering value to our team.

Our people are tasked with achieving the Bank’s vision and embodying and representing our strong customer-focused culture. They execute the strategy which essentially involves delighting the customer and maintaining operational excellence. They are at the heart of our legacy of success and our future strategy. However, the rapidly changing banking environment also places new demands on our employees. Our team risks obsolescence if they are not well-equipped with the evolving skillsets required in this new digital age. Failure to attract and retain talent hampers succession planning and expansion into new spheres. During the year under review, we concentrated our efforts on assessing and mitigating the new risks to our human capital in order to continue deriving value from and delivering value to them.

Employees by contract and genderTable – 10

| Sri Lanka | Bangladesh | Total | ||||

| Count | Percentage | Count | Percentage | Count | Percentage | |

| Female | 1,314 | 24.77 | 78 | 27.56 | 1,392 | 24.91 |

| Permanent | 1,117 | 21.06 | 65 | 22.97 | 1,182 | 21.16 |

| Contract | 1 | 0.02 | 13 | 4.59 | 14 | 0.25 |

| Outsourced | 196 | 3.70 | – | – | 196 | 3.51 |

| Male | 3,990 | 75.23 | 205 | 72.44 | 4,195 | 75.09 |

| Permanent | 3,660 | 69.00 | 180 | 63.60 | 3,840 | 68.73 |

| Contract | 1 | 0.02 | 25 | 8.83 | 26 | 0.47 |

| Outsourced | 329 | 6.20 | – | – | 329 | 5.89 |

| Total | 5,304 | 100.00 | 283 | 100.00 | 5,587 | 100.00 |

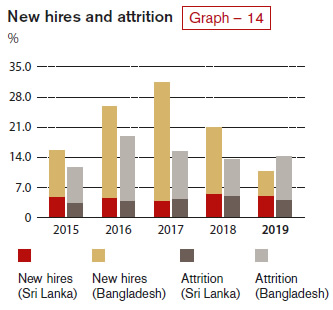

Employee recruitment and retention

Employee recruitment, for the past several years, has proved to be challenging. Young adults entering the workforce are not attracted to banking as a career; indeed, they tend to prefer flexibility and movement rather than being tied to a single institution or sector, and are seeking to rise through the professional ranks more swiftly than the previous generations.

This year, we tackled this challenge with three major recruitment initiatives. First, we raised the intake age of candidates upto 24 years, especially targeting university graduates and those with professional qualifications (rather than only school leavers). We find that candidates in their early 20s, with higher educational qualifications and work and life experience, have a more mature and stable outlook, and are more likely to be invested in building a career with the Bank.

Secondly, we re-started our management trainee programme to attract top-level graduates/professionals by offering them a clear pathway towards career development and advancement. This programme had remained dormant since 2008 because we had a well-established talent advancement pipeline of our own. But we find that precisely because of our robust training programmes, experienced Commercial Bank employees under the age of 30 are in high demand, and attrition rates are higher than average among this group. Therefore, in an era when millennial employees tend to shift careers often, we understood that we needed a new source of young personnel to replace the current tier of middle-management as they graduate to higher positions.

In addition, this year we were more open to recruiting mid-career professionals from outside the banking sector to supplement our intellectual capital and address expertise and capacity gaps. The challenge of any employee strategy is to carefully balance the retention and development of internal talent with the appropriate and healthy infusion of external talent. We believe that a diversified, multigenerational workforce, with varied perspectives and viewpoints contributing to innovation and decision-making at all levels, has the power to boost the Bank’s competitiveness.

The Bank introduced a retirement readiness programme for employees reaching retirement in 2019 and 2020, with the aim of preparing retirees to be able to manage the financial and personal consequences of a post-retirement life. Under this initiative two programmes were conducted during the year titled “New Life after Retirement”.

Employee training, development, and advancement

Our training initiatives this year revolved around the crucial need of the moment: converting our employees into digital bankers. Our focus is on structured talent development, and we are particularly sensitive to the learning patterns of our millennial employees. Studies have shown that in this digital age, when information is just a quick internet search away, employees retain information in varying form. For this reason, the Bank utilises a variety of innovative learning tools and channels like chat bots, apps, artificial intelligence, Branch TV programmes, and online training modules so that employees have information and guidance material at their finger tips. The emphasis is on a continuous ‘anywhere-anytime’ learning experience, rather than isolated training activities. We are in constant process of evolving our approach to training and development in order to provide our employees with agile and future-proofed skill-sets.

Enhancing employee experience

In this rapidly changing environment, we believe that upholding recognised standards and principles for labour practices, human rights and occupational health and safety is vital. We strive to ensure safe and fair working conditions and practices, and to create an environment that allows our employees to flourish.

In this respect, we see our efforts at enhancing productivity and profitability as entirely compatible with employee well-being. Centralisation, automation, and digitalisation enable the Bank to become cost-efficient by facilitating our growth while maintaining current staff numbers. But they also provide many benefits to the working experience of employees by delegating mundane, repetitive tasks to RPAs and making operational processes more streamlined. This reduces the demands and pressures on our people, enabling them to work more efficiently and productively; and in turn, staff fatigue and exhaustion is reduced, while enabling morale and motivation to remain high. And in line with this increased emphasis on employee well-being, for the first time we provided staff with the facilities of external counselors. We believe that in the fast-paced business context of banking, promoting mental health is paramount.

Employees by category and genderTable – 11

| Age 18-30 years | Age 31-50 years | Age over 50 years | Total | Percentage | ||||

| Male | Female | Male | Female | Male | Female | |||

| Corporate Management | – | – | 5 | – | 19 | 4 | 28 | 0.55 |

| Executive Officers | 113 | 42 | 1,407 | 345 | 158 | 79 | 2,144 | 42.35 |

| Junior Executive Assistants & Allied Grades | 1,006 | 307 | 752 | 258 | 21 | 62 | 2,406 | 47.53 |

| Banking Trainees | 324 | 98 | 4 | – | – | – | 426 | 8.42 |

| Office Assistants & Others | – | – | 20 | 1 | 37 | – | 58 | 1.15 |

| Total | 1,443 | 447 | 2,188 | 604 | 235 | 145 | 5,062 | |

| Percentage | 28.51 | 8.83 | 43.22 | 11.93 | 4.64 | 2.86 | ||

The Bank remained committed to the principles of equal opportunity irrespective of gender, age, race or religion in all our processes from recruitment to career development and progression. Here, our focus on women’s empowerment in our external customers (see Customer Centricity) extends to our internal staff as well. Improving female representation on our team has been difficult; issues like transferability have normally deterred recruitment of women into the banking sector. Nevertheless, the proportion of female employees receiving training, promotion and representation at Senior Management levels in comparison to the overall staff mix demonstrates our commitment to equal opportunity. In addition, the Bank continues to ensure that the ratio of basic salary and remuneration of women and men across all locations of operation and all employee categories remains equal.

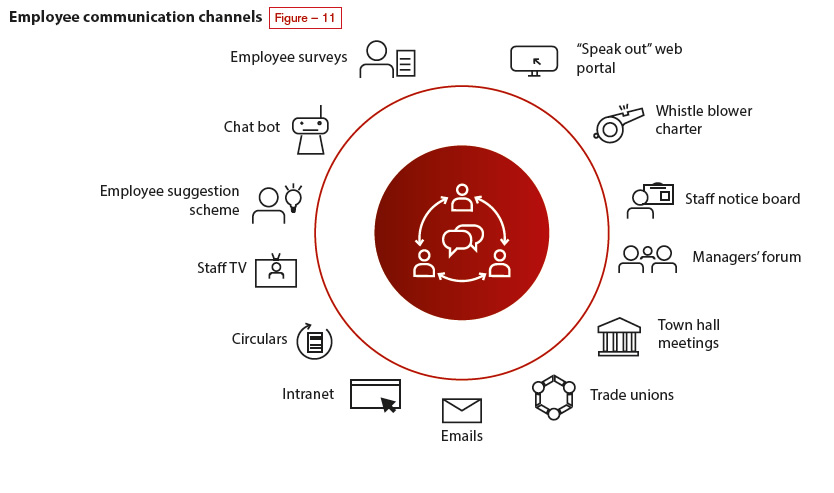

We engage with our staff on an ongoing basis at all levels through a variety of forums and channels including staff circulars, magazines, etc. Feedback and input from our staff members assist us in understanding and responding to their needs and concerns, and improving their working environment and experience. Regular communication also provides our team with strategic direction and keeps them abreast of the latest innovations in technology and processes. We believe that these open lines of communication are vital in creating a unified culture within the Bank.

We maintain a healthy relationship with our branch of Ceylon Bank Employees’ Union and the Association of Commercial Bank Executives which plays a pivotal role paving the way for an effective engagement with our staff. 68% of our employees in the Sri Lankan operation are members of the Ceylon Bank Employees’ Union (CBEU) while 19% are members of the Association of Commercial Bank Executives. Our employees in Bangladesh operations do not hold membership in any trade association. All members of the branch union of the CBEU are covered by the Collective Agreement which is reviewed every three years.

Arrangements to re-establish a pension fund for employees recruited after the year 2000 (shortly before the previous pension scheme was discontinued) are being finalised. The Bank is confident of having this in place during the year 2020.