Bank of Ceylon is the Country’s first state-owned Commercial Bank, and remains fully owned by the Government of Sri Lanka. The Bank also attracts investments from individuals and organisations who purchase its debt securities, as well as lenders who provide crucial financial support. Additionally, the Bank also functions as a Participatory Financial Institute (PFI); leveraging bilateral and multilateral funding from international agencies and engaging in refinancing to directly support targeted industries and segments of society. These partnerships enable Bank of Ceylon to enhance its services and contribute to National development.

Highlights

LKR 6.5 billion

BASEL III compliant subordinated Tier II debenture fully subscribed.

Capital infusion of

LKR 730 million

made by the Government Treasury during the year

Dividend policy focused on preserving profit generated for internal capital generation.

29% cost-to-income ratio reflects effective cost management despite hyper-inflationary pressures.

Ensured strength of the Balance Sheet by covering

10%

of the loans and advances by impairment provision to face

future shocks

LKR 10,167.37

net assets value per share

Operating Context

Despite the challenging operating environment, the Bank of Ceylon remained steadfast in fulfilling its commitments to the shareholder. BoC successfully navigated unprecedented challenges to deliver a noteworthy performance that underscores the Bank’s sustainable business model, strategic decision-making, and dynamism and agility in responding to crises.

Throughout the year, focus remained on delivering sustainable value to stakeholders, delivering on commitments, and upholding the Bank’s proposition.

The Bank's performance in this regard is described in detail in the Financial Review, and the Business Line Reviews.

Profitability

Profit before tax of

LKR 31.0 billion

14%

growth in Net Interest

Income (NII)

91%

growth in non-fund based income supported by

FOREX gain

15%

increase in net fee and commission income

LKR 87.2 billion

impairment provision against loans and advances, and foreign currency denominated Government Securities

29%

cost to income ratio

Balance Sheet Strength

Assets growth of 14% against negative GDP growth

10% growth in private sector loan portfolio

43% growth of investment book

10% impairment provision as a percentage of gross loans and advances

Capitalisation

Capital buffers maintained throughout the year

LKR 24.9 billion

internally generated capital during the year

LKR 6.5 billion

Tier II compliant debentures issued to strengthen Total Capital

Shareholder Return

14.1%

Return on equity

LKR 1,279

Earnings per share

LKR 13.86

Dividend per share

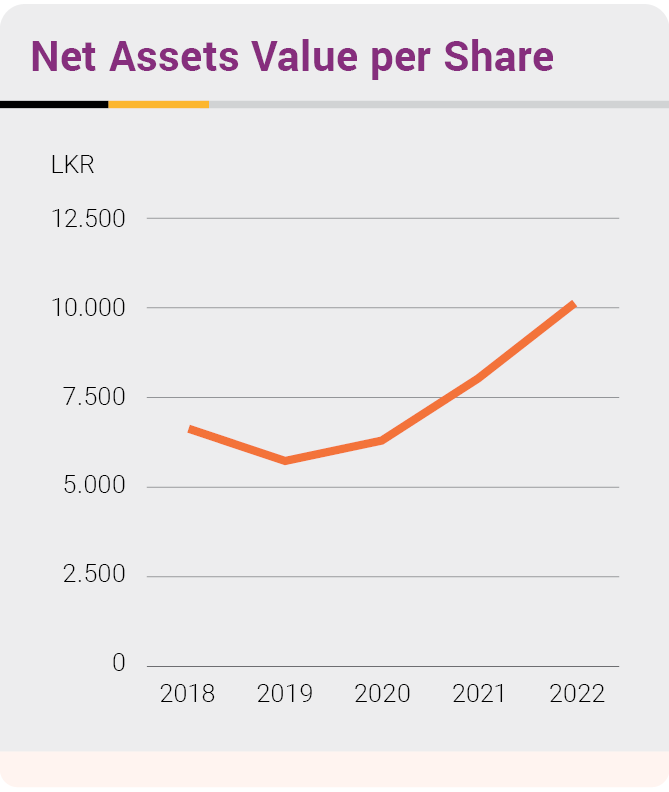

Net Assets Value per Share

Indicating the Bank’s stability and strength the Net Assets Value (NAV) per share of the Bank has been increased over the years. During the year 2022, NAV per share has been increased by 27% in line with the 14% growth reported in the assets base.

Earnings per Share

The year 2022 was also a challenging year for the Bank which brought down the Profit After Tax for the year by 15% comparing to 2021. In line with the drop in PAT, the EPS of the Bank for the year also declined by 15%.

Dividend per Share

The Bank’s Dividend per share decreased by 81% during the year as the internally generated capital was preserved to ensure the stability and future growth of the Bank with the agreement of shareholder while adhering to the prudential directives given by the regulator.

Way Forward

Considering uncertainties in the economic climate in 2023 and beyond, Bank of Ceylon is prioritising strengthening of the balance sheet in order to pursue long-term sustainability and value-creation potential of the Bank.

The Bank expects to unlock gains from technology adoption, leverage synergies, and maximise on opportunities in order to achieve moderate growth in key areas, in the year ahead.

The Bank is committed to continue meeting its obligations and commitments in the short, medium, and long-term; on the back of successful liquidity management. As a responsible participatory financial institution, the Bank has taken steps to weather this challenging period and position itself to support Sri Lanka’s economy, industry, and institutions alongside the Country’s economic revival.

BoC is committed to consistent scale-up of Environment & Social (E&S) assessment, in line with the Bank’s ESMS policy that is in accordance with major multilateral and bilateral guidelines.