A diverse customer base is at the centre of BoC’s business model and ability to create long-term value. In a challenging year, Bank of Ceylon displayed valuable commitment to its customers, providing wide-ranging concessions and working diligently to revive and rehabilitate businesses; bolstering value chains and jobs across the Country.

Highlights

2,166

Direct customer touch points

Most Loved Brands– by LMD and Brand Finance –

Ranked 2nd in the Banking category

Best People’s Banking Service initiative

Asian Digital Finance Forum and Awards

Novel concepts

BoC SME Circle, BoC Export Circle, BoC Foreign Circle

Continuing from a challenging business environment in 2021, the new year brought about a plethora of new challenges for the Bank’s customers. Change toward a high interest rate regime and repayment capacity were primary concerns, with the Bank receiving a number of queries regarding these matters during the year.

The Bank prioritised stability of the Bank’s Financial Position and ensured adequate local currency and foreign currency liquidity to meet the urgent ongoing needs of corporate customers, while also providing for national needs in terms of import of essentials. Details of these and other efforts by the Bank are described in the business line reviews and the Community and Environment section.

Operating context |

||||

|

|

|||

The Bank’s response |

||||

|

|

|

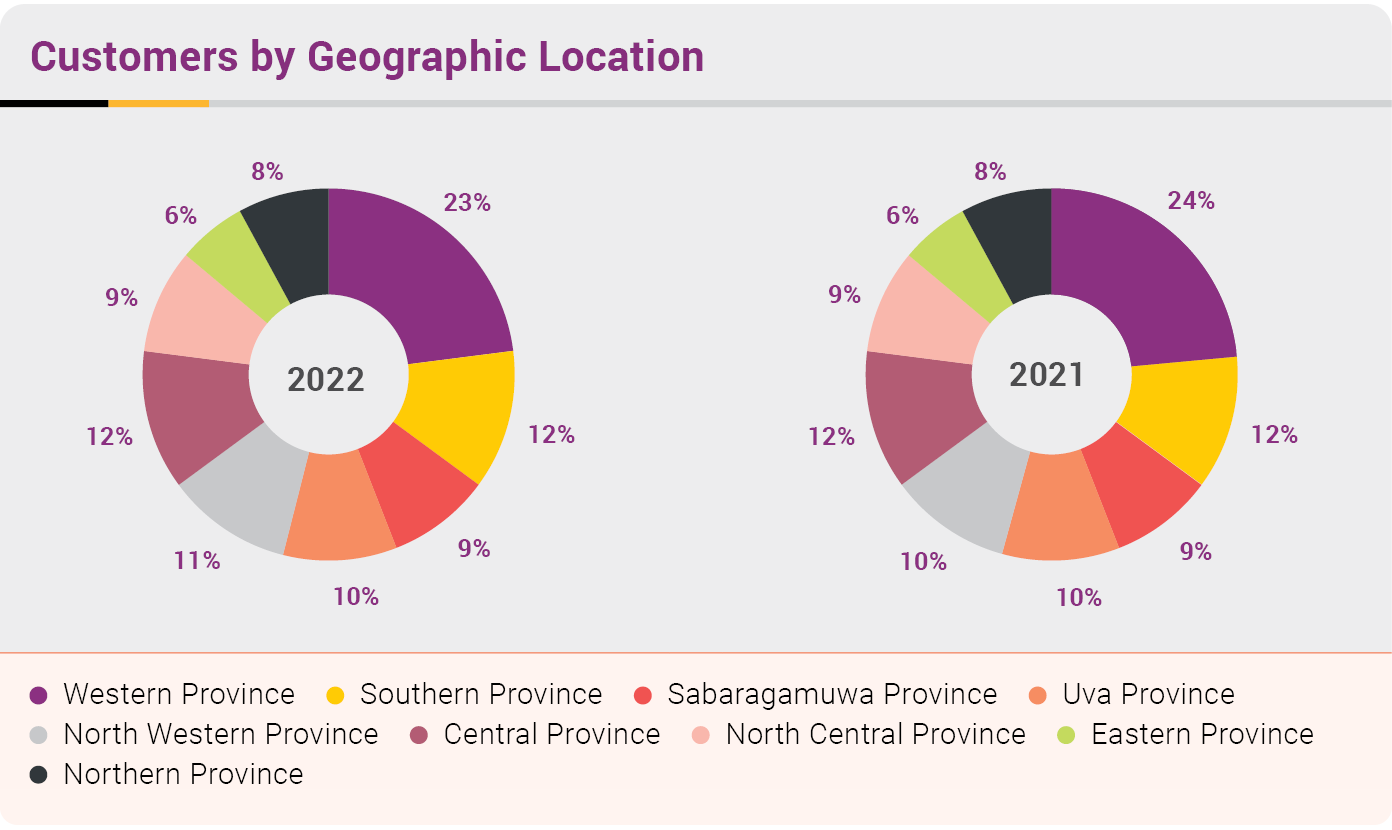

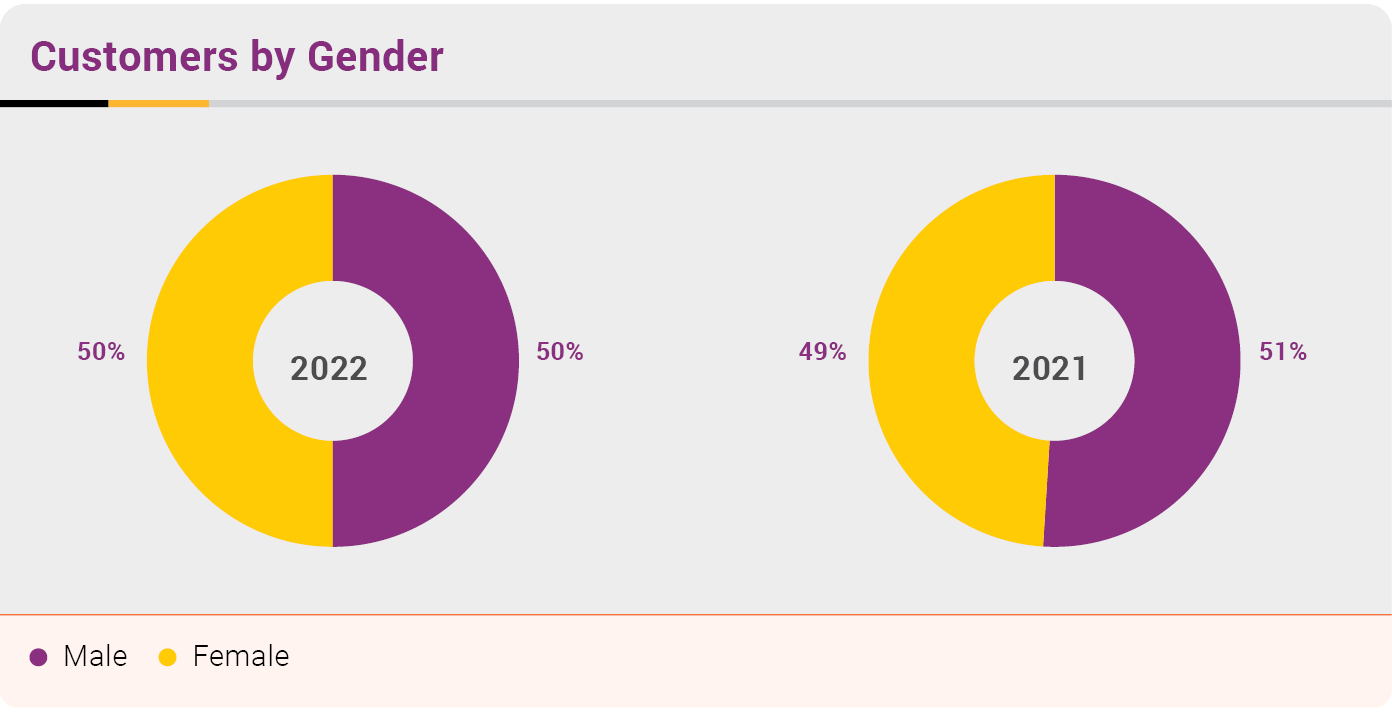

Customer Profile

652,961

new customers

67%

customer penetration

14.9 million

customers

50% female customers

Bank of Ceylon caters to a wide spectrum of over 14 million diverse customers from across Sri Lanka and overseas. This impressive customer base, which translates to an unmatched penetration rate of 67%, comprises individuals, infant to senior citizens, micro-enterprises, small and medium-sized enterprises, large companies, multinational corporations, and state-owned enterprises.

The Bank leverages long-standing relationships with global partners and a comprehensive product-mix to meet the dynamic needs of a rapidly changing economy and delivers outstanding value to its customers.

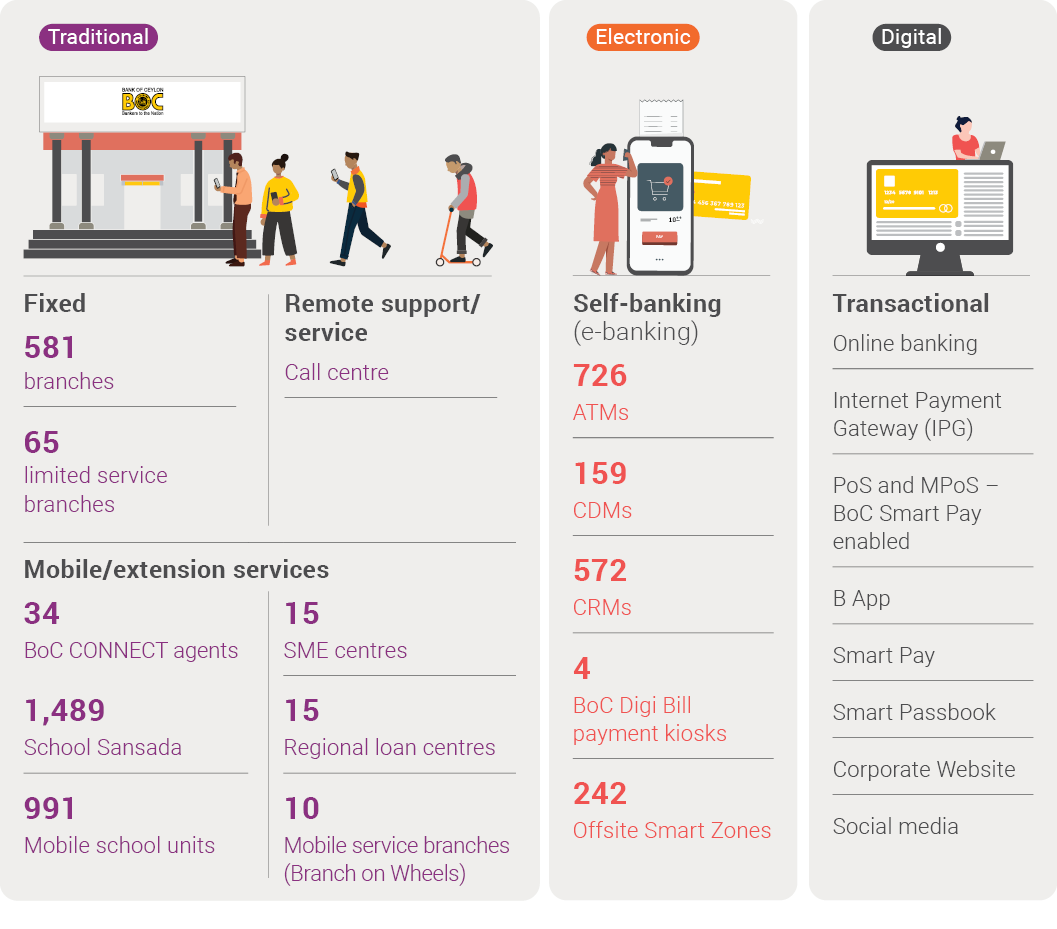

Access to Financial Services

Access to Financial Services

BoC serves all segments of society and reaches customers from all walks of life through the Country’s widest branch network and physical presence, a rich and diverse product-mix, and a rapidly expanding digital footprint. Fuelling economic activity through access to financial services, nurturing a savings culture, and reaching the underserved and underrepresented are essential components of the Bank’s mandate.

Financial Inclusion

Improving access to finance and financial inclusion for the most remote, vulnerable, and historically underserved or unbanked segment of society is a key priority. The Bank’s wide geographic footprint; consisting of an extensive branch network coupled with mobile and limited service branches, ensure financial services are easily accessible and within reach for millions of Sri Lankans.

BoC’s mobile and extension services such as mobile banking through 10 ‘Branch on Wheels’, are critical at ensuring uninterrupted access to banking services for remote locations during the periods of disruption.

Bank of Ceylon’s other efforts to achieve greater financial inclusion, such as targeted development lending to entrepreneurial ventures, MSMEs, and cottage and community industries are detailed in the Community and Environment section.

BoC Connect

A unique innovation in this regard, is the Bank’s grassroots agent-banking network - BoC Connect, which was launched in 2021. This agent-banking service enables customers in remote locations or customers with limited accessibility, to perform a range of financial transactions via assisting agents. Services include cash deposits, cash withdrawals, credit card and bill settlements, and fund transfers. During the year, the Bank recorded a total transaction value amounting to LKR 570.0 million executed through BoC Connect. Further, based on regulatory approval obtained during the year, the Bank plans to onboard 16 new agents in 2023. Thus bringing the total BoC Connect network to 50. With agent screening processes ongoing, the Bank plans to extend this facility to reach even more remote customers in rural areas in the future.

Ensuring Business Continuity

2022 brought several disruptions to economic activity and transport and accessibility across the Island. However, the Bank took all efforts to prioritise business continuity for the benefit of customers; ensuring that no branches were closed even during the fuel crisis. Uninterrupted access to services was also ensured by BoC’s extensive network of touch points.

In addition, the Bank took steps to reach particularly isolated and remote areas with BoC’s mobile banking units during the fuel crisis. These measures that were critical during the COVID-19 pandemic induced lockdowns, proved invaluable in 2022 as well; ensuring remote customers retained access to services even during the fuel crisis.

Further details of the Bank’s efforts to ensure business continuity are detailed in the Retail and Corporate Banking business line reviews.

Expansive Multi-channel Footprint

With 2,166 customer touch points across the Island, BoC has the most expansive geographic reach and footprint in Sri Lanka. In line with global and local trends toward greater digitalisation, the Bank implements a multi-channel strategy that includes greater expansion of its electronic and digital footprint. In 2022, this shift toward electronic and digital transactions resulted in 48% of all customer transactions occurring through digital or electronic banking channels.

Continuous investment in physical and digital infrastructure increases accessibility for customers, while also contributing to customer convenience and overall customer experience. During 2022, the Bank made several enhancements to branches, opened a new branch in the Uva Province, expanded the network of Cash Recycling Machines (CRMs) to key institutions such as hospitals, educational institutions, airports, railways, and tourist attractions.

Channel Developments

Customer-centricity

LKR 74.4 billion

value of moratoriums granted

42,073

customers benefited by granting concessions

12

new products launched

LKR 7,397.2 million

value of facilities rescheduled

2,230

customers benefited by rescheduling

Customer-centricity is a key pillar in Bank of Ceylon’s transformation strategy. The Bank has always maintained a customer-centric approach to doing business, and this was never more evident than in the Bank’s response to customers affected by the ongoing crises in Sri Lanka.

Business Revival and Rehabilitation

GRI 201-1

40

businesses revived

22

businesses under revival support

Approximately

2,500

direct and indirect jobs protected

LKR 11.8 billion

customer cashflows managed by BRRUs

LKR 65.4 billion

customer exposure with revival support

Following disruptions caused by the COVID-19 pandemic, Sri Lanka’s economic crisis in 2022 brought unprecedented challenges for the Bank’s corporate customers. Businesses faced loss of competitiveness, increased cost of capital, major working capital and cash flow issues, and in the worst cases: business failure and closure. This resulted in continuous increase of Non-Performing Credit Facilities (NPCFs).

In response to the ongoing crises, the Bank focused on revival of businesses over recovery; a key component of the Bank's strategy toward implementing a rewarding credit culture and healthy credit portfolio.

During the year, the Bank provided critical and continued support to customers affected by the crises, including extended moratoriums, concessions, and rescheduling and restructuring facilities. Additionally, affected businesses were granted fresh facilities to meet working capital requirements and ensure their survival and long-term sustainability. A key component in the Bank’s efforts was the Business Revival and Rehabilitation Unit (BRRU) established during the previous year.

Key Actions for Business Revival in 2022

Strengthening the function of the BRRU by expanding to all provinces.

Establishing a special committee and holding weekly review meetings chaired by the CFO, to assess and take quick decisions regarding support and relief to corporate customers.

Strengthening the Bank’s oversight and monitoring and evaluation functions for loans and advances at all levels.

Engaging closely with customers; proactive and routine visits to provide business advice, consultancy, and solutions during the crisis.

Customising, rescheduling and restructuring of facilities to suit each customer’s individual cash flows.

Holding regular workshops and revival clinics to build awareness and capacity of staff to respond to varying customer needs and provide quick and dynamic revival measures.

Reviewing the Bank’s recovery policies and guidelines.

| Business revival | 2022 | 2021 |

| Businesses revived | 40 | 16 |

| Businesses under revival support | 22 | 6 |

| Number of employment secured (approximately) | 2,500 | 4,900 |

Supporting Retail Customers

LKR 67.9 billion

Interest rate rationalisation for "Personal and Pensioners Loan Schemes"

Interest rate fluctuations in 2022 and the ongoing high interest rate regime had a drastic effect on personal loan customers who obtained credit on variable interest rates (VIR). The Bank made an internal decision and accommodated regulator recommendations to support crisis-affected personal borrowers. Where appropriate, a concessionary interest rate was extended to VIR borrowers and credit granted at fixed rates was honoured in line with regulator requirements, with the Bank absorbing the additional funding cost. Further, information on support to retail customers is detailed in the business line reviews.

Innovation and Responsiveness to Customer Needs

The Bank continuously engages with customers, remains responsive to their concerns, accommodates regulator recommendations and carries out market research to provide a richly diverse product-range that caters to the full volume of the market. In response to the crisis and the changing needs of customers, the Bank launched a number of new products including time deposits that enabled customers to meet their investment needs in line with interest rate movements. An affinity card for state sector employees and a Health Savings Account, the first of its kind in Sri Lanka, were some of the new products and services extended to customers during the year. More information on products is available in the business line reviews

Innovation to meet the needs of customers and country is at the heart of Bank of Ceylon’s business model. The Bank has pioneered a number of initiatives to support key customer segments to diversify their offering, access new markets, expand their business and gain local and international exposure. Key amongst these are the BoC Export Circle launched the previous year, and the new SME Circle, launched in January 2022. More details of the Bank’s development lending are available in the Community and Environment.

Export Circle

LKR 1.2 billion

loans disbursed under export circle

191

exporters canvassed under export circle

The BoC Export Circle supports export-oriented businesses, particularly SMEs, with networking opportunities and capacity building, in addition to the financial support. The Bank works closely with key state and industry agencies such as Export Development Board (EDB), National Enterprise Development Authority (NEDA), to provide customers with crucial, timely, and continued support. These efforts also addressed the Country’s urgent need for increased foreign exchange inflows through improved competitiveness of exports.

SME Circle

Provide information and advisory services in addition to credit

Focuses on export oriented, SME innovators, inventors and tech startups

Introduced in January 2022, the BoC SME Circle focuses on Small and Medium Enterprises (SME) export-oriented businesses, innovators, inventors, and business and tech startups; providing information and advisory services in addition to access to credit in the form of business startup and seed funding. During the year, the Bank launched a dedicated mobile application and web-portal to allow customers to apply for loans and raise requests.

Foreign Circle

5,446

customers served

21

awareness programmes conducted focusing customers

To commemorate the 83rd anniversary, Bank of Ceylon launched its International Customer Service Support Unit, 'BoC Foreign Circle'. The unit, launched by the Bank's International Division, aims to provide maximum convenience to BoC customers who work and live abroad. Whilst new unit's representatives will engage with customers in Asia, Europe, the Middle East, and other countries to ensure they could quickly and conveniently access services in Sri Lanka. Customers are able to experience the services such as instant account opening, obtaining ATM and other cards, loans, and online banking services, along with numerous other convenience-driven products and services.

Customer Experience

Excellence in customer experience is one of the Bank’s strategic pillars, which ensures the Bank's ability to maintain a distinct and differentiated presence in the sector, while ensuring retention of customers and attracting new business.

BoC’s Customer Experience Unit serves as a dedicated team to handle customer complaints and addresses service-related issues, whilst identifying areas for capacity enhancement of front line staff. The Bank’s dedicated research unit conducts surveys to assess customer satisfaction and identify pain points for improvement of customer experience. These elements have helped to create a service-oriented culture within the Bank.

During the year, the Bank carried out a number of initiatives to improve customer experience and service delivery across branches, business lines and customer touch points.

- Customer Experience Unit was strengthened and staff capacity improved.

- Branches and Smart Zones were improved to be consistent with BoC’s brand and branch standards.

- Implementation of 5S at branches monitored and improved. Physical assessments carried out, followed by competitions and challenges to improve adoption and adherence.

- Branch-level performance and motivation measures carried out, including financial incentives and real-time leaderboards contributing to reduced errors and improved service delivery.

- Intra-bank awards and challenges conducted (Spirit Awards and Challenge Awards) to drive motivation and ensure service delivery standards.

Internally, the Bank has continued to invest in and implement Robotic Process Automation (RPA) for processes that improve customer convenience. These investments have improved turnaround times, and the customer experience.

A key step in improving customer experience was the introduction of new digital services that provide increased convenience and reliability for customers. These include automations for transactions that can be carried out seamlessly through a number of the Bank's digital platforms including online banking and mobile banking. Additionally, continuous improvements to the digital customer journey have resulted in large gains for customer service and customer experience.

Process Improvements as a Result of Workflow Automation via DMS

| Process | Previous position | Current position |

Debit card reactivations |

Handled centrally Turnaround time – 3 Days |

Reactivations are done at branch level and turnaround time – 10 minutes |

Online application for credit cards |

Feature not available |

Customers can request credit cards through BoC’s web portal |

Covering approval for pawning |

Manual process Turnaround time – 3 Days |

Automated paperless process Turnaround time – 1 hour |

Improvements to prior approvals in corporate segment |

Timeout issues existed |

Process improvement made |

Improvements to near cash loans |

||

Improvements to generic approval process |

Improved case search options and identified issues were rectified |

|

Improvements to |

Special rate upper limit validated Data quality index validations not available |

Special rate upper limit parameterised Integrated to data quality Index validation engine Product level total FD amount validations added |

Additionally, continuous improvements to the digital customer journey have resulted in large gains for customer service and customer experience.

The Bank’s complaints handling procedure ensures transparency and accountability with all stakeholders. Feedback is encouraged at every touchpoint, with the perspective of providing quality service to stakeholders.

| 2022 | 2021 | |

| Number of complaints B/F | 39 | 36 |

| Customer complaints received during the year* | 3,054 | 2,159 |

| Customer complaints addressed during the year | 3,069 | 2,156 |

| Number of complaints C/F | 24 | 39 |

| Net Promoter Score (NPS) | 35 | 40 |

| Customer satisfaction rate (%) | 78 | 79 |

* Number of complaints in year 2022 increased by 41% compared to 2021, primarily due to:

– Significant increase in complaints regarding the increased loan interest rates

– Loan recovery issues

– Interest rates applicable to early redemption of fixed deposits/penalty rates

Digitalising the Customer Journey

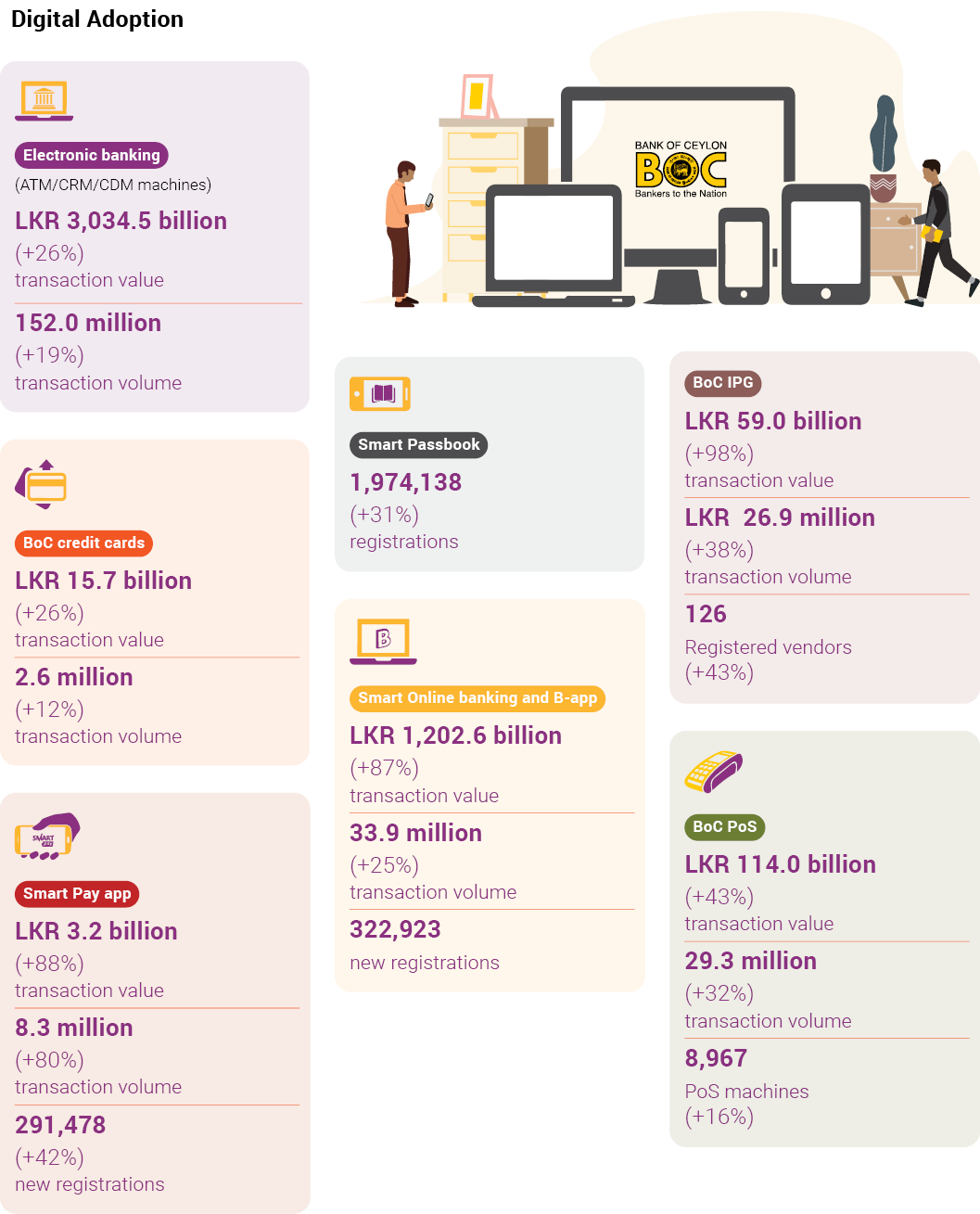

Bank of Ceylon recognises the crucial role of digitalisation in meeting the modern demands of the banking sector whilst enhancing customer experience and ease of banking. As such, Digital Excellence is a cornerstone of the Bank’s strategy for medium to long-term sustainability. The Bank continues to invest in digital infrastructure and solutions that cater to the diverse needs of its customers. As a result, there has been significant adoption of digital channels resulting in 48% of all customer transactions occurring through digital or electronic banking channels in 2022.

Highlights of the Bank’s efforts for greater digitalisation of the customer journey in 2022:

- Introduction of Digital KYC to all branches, including paperless customer onboarding with e-signatures.

- Expanded merchant network equipped with BoC’s SmartPay enabled PoS and MPOS machines.

- Initiated new partnerships with state institutions, fuel stations, and charities to enable cashless transactions through SmartPay.

- Retained status of number one e-commerce acquirer by onboarding new vendors for BoC’s Internet Payment Gateway (IPG).

- Introduced apply online facilities for a variety of new banking transactions, including personal loan products, home loans, savings accounts, and credit cards.

- Oriented customers with the Bank’s digital products through branch-level initiatives, including real-time digital dashboards and physical “Meeter-Greeters” engaging with customers and providing a walk-through of digital products.

- Introduction of new automated modules for debit card cancellation, covering approvals for TOD, covering approvals for pawning, DQI validation, etc.

- Facilitation of digital updating of life certificates for pensioners via BoC branches.

- Automation of large-value merchant payments via SLIPS.

- Automated customer notification and updating system.

Investment in Digital Infrastructure

In line with greater adoption of digital products and services resulting in increased share of digital transactions, the Bank continued to invest in strengthening digital infrastructure to ensure reliability, system-availability (uptime), and security across multiple channels. System uptime is measured regularly and incorporated as a KPI for key business units and staff.

Highlights of investments in digital infrastructure in 2022, to uplift customer service:

- Strengthened back-end to support increased load of online banking transactions

- Automation of several workflows, including debit card re-activation, FD opening, DQI validations, near cash loans, etc.

- LKR 810 million Investment during the year, pertaining to hardware infrastructure catering to the high volume of digital transactions.

- Provisions to ensure business continuity via remote-working and WFH for bank employees.

- Enhancement of BoC SmartPay features to meet the needs of different vendors and sectors, including extension of Lanka QR for payments to state institutions, fuel stations, charitable payments, and Web QR payments.

- Introduction of Dynamic QR and a Merchant Portal (with Dynamic QR, comprehensive detail reports, and interoperability of Web QR)

- Introduction of new features for BoC Connect and expansion to wider agent-network.

- Introduction of multilingual support for BoC Smart Passbook.

- Implementation of internet and mobile banking systems for the Bank’s overseas branches.

- Introduction of a new Trade Finance system.

- Recruitment of new personnel and engineers for the Bank’s IT division.

- Digi-pads expanded to all branches.

- Streamlined goAML reporting as part of the Bank’s efforts to prevent financial crime.

Customer Education

1,019

customers directly benefited through education and awareness raising programmes

Bank of Ceylon is committed to conducting ongoing customer education and awareness programmes that target a diverse range of groups, including SMEs, MSMEs, women entrepreneurs, students, and public servants.

During the year, the Bank conducted a variety of programmes to education, raise awareness, fight disinformation, and contribute to financial literacy:

- Financial Literacy programmes targeting Development Assistants and Development Banking Staff.

- Financial Literacy with the Central Bank of Sri Lanka (CBSL) for Domestic, Agriculture and Development (DAD) custOmers.

- Education programmes for nursery growers registered with the Department of Export Agriculture.

- Awareness raising programmes with fisheries communities about the Bank’s concessionary Diyawara Diriya loan scheme.

- Education and awareness-raising programmes about inward remittances through formal channels.

- Awareness programmes about children’s banking products and green savings products: e-thuru, Diyavara Kekulu, Haritha Kekulu.

- Integrated communications and multi-channel campaigns to fight disinformation and build confidence in Sri Lanka’s banking industry.

Responsible Banking

Bank of Ceylon practices transparency and accountability in all interactions with customers, and is committed to providing clear and accurate information about all products and services. The Bank clearly communicates all relevant information to customers in a language of their preference, including details such as interest rates, maturity periods, and all terms and conditions. Banking practices and customer engagement are fully aligned with the CBSL Customer Charter, which outlines the obligations and standards that customers can expect.

Data Privacy and IT Security

In line with moves toward greater digitalisation and online and mobile transactions, the Bank considers information security and data privacy as key focus areas of its responsibility toward customers. The Bank is committed to safeguarding the privacy and security of customers' personal and financial information through rigorous IT security policies and procedures and a risk-conscious organisational culture.

GRI 418/FN-CB-230a.1

No complaints were received concerning breaches of customer privacy. No data breaches were identified during the year, no Personally Identifiable Information was subject to data breaches, and no account holders were affected by data breaches.

FN-CB-230a.2

During the year, in addition to investing in digital infrastructure, the Bank took measures to strengthen IT Security by revising policies, conducting regular vulnerability testing, and improving alignment with leading IT and cyber security standards and frameworks. The Bank’s efforts to manage IT risks are further detailed in the Risk Management Report.

Highlights of the Bank’s actions to improve data privacy and IT security in 2022:

- Complied with industry standards and enabled two-factor authentication (2FA) via 3DS 2.0 authentication protocol, to maximise security of customers.

- Implemented deception technology at the Bank’s overseas branch in Chennai.

- Security Operations Centre (SOC) and Network Operations Centre (NOC) set up.

- Process initiated to obtain ISO 20001 certification for Information Technology service management.

- COBIT IT governance framework implementation initiated.

- Cyber-security training and awareness raising programmes conducted for staff across a variety of business lines.

- Data security policies and processes reviewed.

- Implementation of Data Loss Prevention (DLP) and data leakage prevention solutions underway at the Bank’s Head Office and overseas branches, with plans to expand to all branches.

GRI 418-1

| 2022 | 2021 | |

| Data breaches (Numbers) | Nil | Nil |

| Percentage of data breaches involving Personally Identifiable Information (PII) (%) | Nil | Nil |

| Account holders affected by data breaches (Numbers) | Nil | Nil |

Way Forward

The Bank is positioning itself to support customers during 2023 too. Even as moratoriums come to an end in December 2022 and crisis-affected businesses face repayment pressures, Bank of Ceylon remains committed to working with customers in line with expected regulator recommendations for further concessions to affected borrowers during the upcoming year.

Key priority areas for the Bank in 2023 and beyond:

- Continued focus on scaling up digitalisation and adoption of digital products and services including continuous improvement and adoption of process automation.

- Strengthening internal controls and investment in capacity building of workforce to deliver sustainable value to customers.

- Strengthening of central BRRU and decentralised BRRUs to handle larger volumes and participate in the revival of businesses and the economy and creating a Business Revival culture within the Bank.

- Exploration of benefits and convenience features for BoC cardholders, including improvements to self-service.

- Further enhancements to security infrastructure, network infrastructure, and remote-working capabilities.

- Enhancing green lending and green products.

- Exploration of AI and machine-learning to support predictive capabilities and functions of the Bank.

- Launch of new website with greater accessibility and other features.

- Exploration of new non-traditional social media platforms and customer touch points.