Financial Review

During the year 2022, the Country and the Bank faced extreme headwinds and heightened uncertainties that demanded an exceptionally high focus on strategies to manage the never-experienced situation and ensure stability of the Bank. Under this context, despite unprecedented changes to the operating environment, the Bank navigated challenges while prioritising business continuity and long-term sustainability of customers and the Sri Lankan economy.

The economic environment that prevailed during the year 2021 was very different to what we experienced during the year under review. During 2021, the Country had followed a low-interest regime with lending rates of 11% to 12%, and deposit rates of around 8%; the Government of Sri Lanka had consistently serviced facilities with no indication of default on Sovereign liabilities; and the SLR was buoyed by a pegged exchange rate while normal rates of inflation were prevalent. At the same time, the Country was in a phase of recovery as tourist arrivals and COVID-19 hit businesses indicated a gradual uptick after the worst of the pandemic.

Despite setting a course for 2022 based on these conditions, what followed was a stark turnaround in the operating environment. Sri Lanka’s historically low interest rates shifted to a high-interest regime; the SLR depreciated heavily after the floated exchange rate; cost-push inflation drove a sharp rise in expenses; and ratings downgrades were consequent to sovereign default. The business environment was further hampered by prolonged disruptions to transport and energy, followed by social unrest in Sri Lanka’s capital and other parts of the Island.

The Bank’s agility in responding to these rapidly changing conditions is commendable. We adopted new processes and took stringent measures to ensure stability of the Bank whilst minimising negative outcomes for our stakeholders.

Therefore, the year 2022 can be named as a year of resilience and resolve for the Bank of Ceylon as our responsible governance and future-focused long-term strategy of supporting customers and communities. The Bank recorded Profit Before Tax (PBT) of LKR 31.0 billion, and growth in the Financial Position by 14% by preserving its industry leadership despite the severely challenging operating environment. This was an outstanding performance by the Bank, especially considering plans were made for a low-interest regime and against a vastly different economic backdrop.

Financial Performance

Total Income

The Bank’s total income grew by 77% to reach LKR 513.1 billion by the end of the year, even as interest expenses grew by 121% to reach LKR 329.9 billion. Significant increase in interest expenses reflect changes to the Bank’s deposit mix in line with the industry. This is primarily due to volatility in the country that resulted in a trend toward shorter-term deposits.

Fund-based Income

68% of the Bank’s fund-based income was derived from interest income from loans and advances. The high interest rate scenario that prevailed in 2022 led to an increase in interest income from loans and advances by LKR 117.1 billion, reflecting 61% growth YoY.

Interest income on investment grew by 117% YoY with the upsurge of investments in government security portfolios.

However, as part of a series of concerted efforts to support customers and prevent the adverse impact of the rate hike, the Bank ensured that fixed rates were not changed to variables, variable linked personal loans were given preferential rates based on the circumstances and requests of the customers and moratoria were extended to special segments of the economy that were hardest hit. The Bank extended the benefits of interest rate rationalisation to customers, contributing to significant savings to businesses and households that were facing intensely difficult conditions brought on by the economic crisis. Concessions and benefits extended to customers are detailed in the Stakeholder Outcomes section of the Annual Report.

The Bank’s focus on rehabilitation of businesses over recovery was expanded during the year. We honoured all concessions recommended by the Central Bank of Sri Lanka (CBSL) and extended the moratorium for crisis-affected borrowers. In addition, we pioneered initiatives to support the Country’s Small and Medium Enterprise (SME) sector with initiatives such as the SME circle, which supported customers to transition their manufacturing and products and excel in the local market when import restrictions were in place. The Bank’s Export Circle further supported export-oriented businesses and to drive export competitiveness of Sri Lankan businesses and help strengthen the Country’s external sector performance.

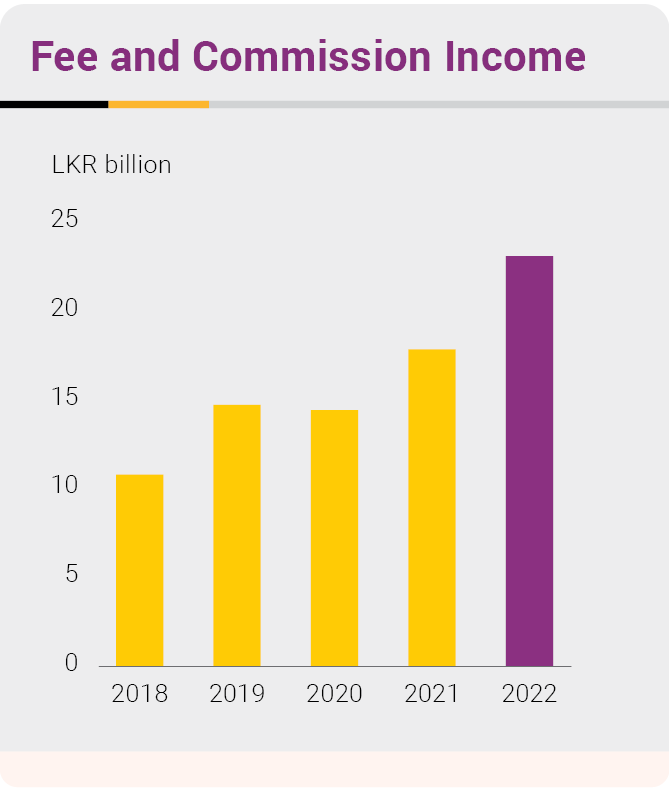

Fee and Commission Income

We recorded a significant growth of 15% in net fee and commission-based income reaching to LKR 16.4 billion in 2022.

This achievement is despite depressed economic conditions and concerted efforts by the Bank to provide concessions to customers who were hard hit by the crisis and interest rate fluctuations.

In line with the Bank and the country’s continued drive for greater digitalisation, we recorded a 65% increase in credit and debit card fee income to LKR 8.9 billion and representing 48% of the total fee income. This reflects success of the Bank’s digitalisation efforts, with BoC also being awarded “Best Bank for Retail Payment” at the LankaPay Technovation awards 2022. Further information of the Bank’s successes in digitalising the customer journey are disclosed in the Stakeholder Outcomes section of this Annual Report.

Further, fee income from travel and remittances also increased by LKR 1.7 billion to reach LKR 3.7 billion during the year, backed by increase in foreign remittances and travel related activities especially during the latter part of the year.

Other Income

The Bank posted a strong performance during the year, with other income amounting to LKR 34.0 billion; primarily due to the floated exchange rate and resulting conversions having a positive effect, as 30% of the Bank’s balance sheet consisted of foreign currency assets.

Almost 81% depreciation of the SLR during the year led to net exchange gains derived from trading activities and currency conversion, which represents a considerable portion of the Bank’s non-fund based income that amounted to LKR 32.9 billion for the year.

Fluctuations in the equity and share market due to the prevailing economic conditions negatively impacted the Bank as mark to market losses of LKR 804.4 million resulted from the equity and unit trust portfolio. However, through proactive engagement, the Bank was able to gain LKR 861.3 million in trading of equity and Government Securities.

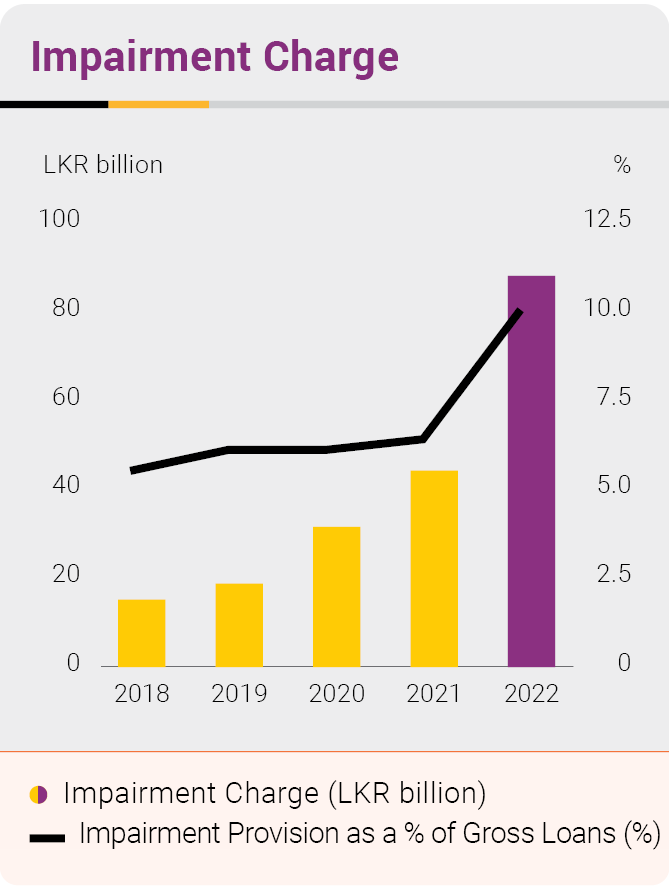

Impairment Charge

The Bank’s corporate customers faced multiple setbacks, including disruption to services and production, which eroded margins amidst depressed economic conditions as Sri Lanka’s economy contracted by 7.8% in 2022. The country’s ongoing economic crisis brought new challenges on the back of two years of pandemic-induced disruption. These factors had a significant effect on asset quality across the financial sector. In this scenario, the Bank’s priority during the year was to support customers through challenges. Revival and rehabilitation of businesses continued to be a key area of focus, with the Bank focusing on long-term sustainability of customers, businesses, and the economy; instead of recovery.

Retail customers were similarly affected; facing cost of living increases alongside a sharp increase in interest rates. In response, Bank of Ceylon provided much-needed relief to customers by providing protection from interest-rate fluctuation, absorbing additional costs, and sharing benefits wherever possible.

Bank of Ceylon’s efforts to revive and revitalise businesses while supporting customers, value chains, and communities, are disclosed in detail in the Stakeholder Outcome section of the Annual Report.

Expecting significant challenges during 2022 and beyond, and in line with Bank of Ceylon’s stringent and prudent provisioning policies, we took steps to prepare for potential shocks with a substantial provision of approximately LKR 87.2 billion for loans and advances and investments in order to mitigate risks and strengthen the Bank’s balance sheet.

From January 2022 onward, impairment provision for loans and advances and investment were provided in compliance with CBSL Directions No.13 and No.14 of 2021 on Classification, Recognition, and Measurement of Credit Facilities and Financial Assets. Thus, the impairment provision for loans and advances and financial investments was calculated to capture the expected losses associated with the customers or the investment instruments based on the possible consequences in current economic conditions, sector specific risk factors, new policy reforms, and present negotiations in foreign and local debt settlements by the Government.

Considering negotiations underway for settlement of foreign and local sovereign debt, the Bank set aside a considerable level of impairment provision for its investments in International Sovereign Bonds and Sri Lanka Development Bonds.

|

Impairment Charge for the year for loans and advances: LKR 70.8 billion (Cumulative impairment provision LKR 259.2 billion) |

|

Stage 3 ratio: 5.3% (2021 – 5.1%) |

|

Stage 3 impairment to stage 3 loan ratio: 59.7% (2021 – 49.1%) |

|

Impairment charge for the year for investments in foreign currency denominated sovereign instruments: LKR 16.1 billion (Cumulative impairment provision LKR 53.5 billion) |

|

Management overlays were applied to identify risk-elevated industries which result in a significant increase in credit risk. Spillover effects of economic turmoil prevailing in the country and exposure to risk-elevated industries assessed as underperforming were taken into account for lifetime credit loss on a prudent basis. |

|

Economic Factor Adjustment (EFA) utilised in calculating expected losses for collectively assessed portfolios was enhanced by capturing the stressed economic conditions. |

|

Individually Significant Loans Customers (ISL customers) were also assessed critically and prudent level of ISL impairment provision was made, given the high degree of uncertainty and extraordinary circumstances in the short and medium-term caused by continuous disruption to businesses. |

Expenditure Management

2022 led to a hyper-inflationary environment with inflation figures peaking in September. However, we were successful in managing our costs, even as operational costs climbed by 14%, primarily due to increase in personnel costs. Amidst double digit inflation, the Bank’s effective cost controlling managed the increase in other expenses below 12%.

Rise in personnel costs reflected the Bank’s decision to invest in employee well-being and retention, by providing a cost of living allowance in consideration of the economic crisis and rampant inflation. The Bank also provided employees with transport during the fuel crisis, ensuring business continuity and smooth operations for customers.

| 2022 LKR ’000 |

2021 LKR ’000 |

|

| Personnel expenses | 28,991,429 | 24,981,940 |

| Depreciation and amortisation expenses | 4,286,899 | 4,146,256 |

| Other expenses | 14,018,161 | 12,552,393 |

Taxation

Value added tax (VAT) on financial services for the year increased by 22% to LKR 11.0 billion as the VAT rate increased from 15% to 18% with effect from 1 January 2022. The Bank also paid LKR 281.3 million to the newly introduced Social Security Contribution Levy of 2.5% during the year, while paying LKR 6.7 billion as the surcharge tax imposed as one-off tax charge during the year. Further, the Bank paid LKR 5.5 billion as income tax during the year.

Deferred tax reversal of LKR 14.5 billion was made during the year mainly due to deferred tax booked on specific provision made on foreign currency denominated sovereign instruments, loans and advances, and adjustment made on current tax rate in line with increase of income tax rate from 24% to 30%. Accordingly, the Bank’s Financial Statements reflected a tax reversal of LKR 995.8 million resulting in profit after tax of LKR 32.0 billion.

Profitability

During the year, Bank of Ceylon’s main focus was to strengthen the balance sheet and support customers as they grappled with unprecedented challenges due to the country’s economic turmoil. The Bank compromised its net interest income growth to 14% and reported a PBT of LKR 31.0 billion as the industry highest.

Other Comprehensive Income (OCI)

Bank of Ceylon’s other comprehensive income (OCI) grew by 233% to LKR 27.8 billion, while total comprehensive income reached LKR 59.8 billion, reflecting a 30% increase YoY. Depreciation of the Rupee against the US Dollar resulted in recognition of a considerable hedge reserve relating to USD/LKR funding swaps amounting to USD 90 million which has been recorded under hedge accounting treatment.

Financial Position

Assets

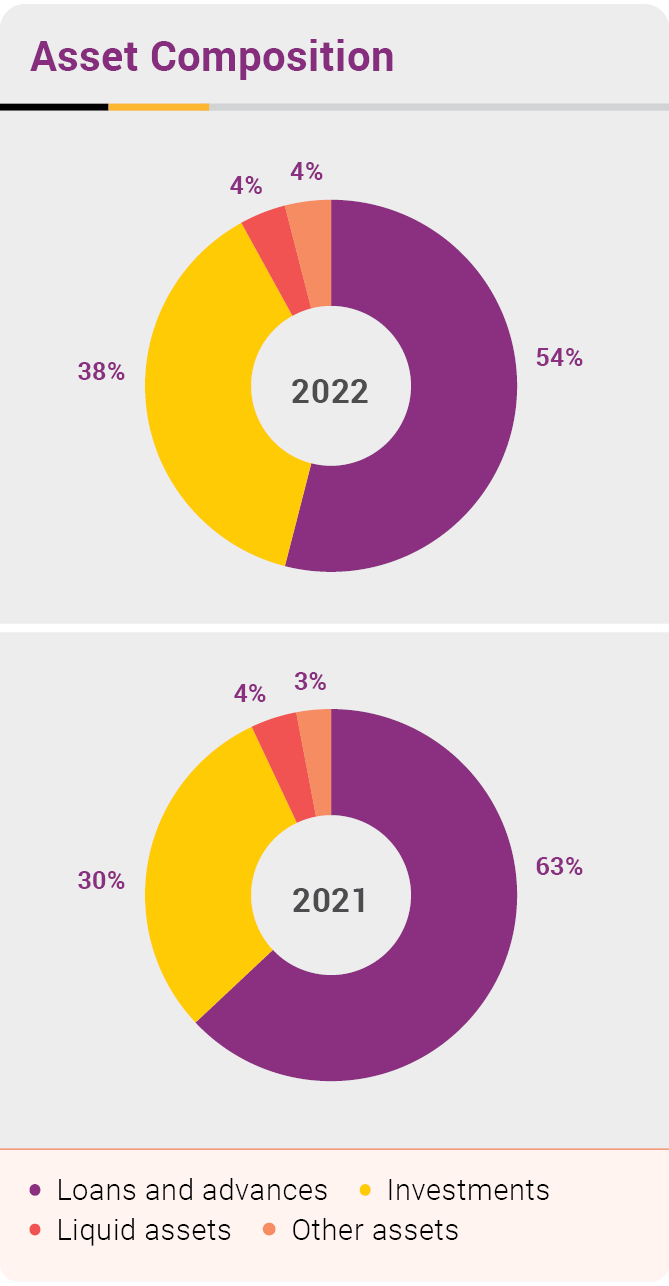

Bank of Ceylon’s total assets grew by 14% during the year, to reach LKR 4.3 trillion, and is on track to achieve our rationalised growth targets. The Bank’s asset composition remained relatively unchanged reflecting long-term sustainability of the Bank’s core business despite challenging conditions.

While debt and other instruments grew by a significant 44% to LKR 1.6 trillion in 2022, net loans and advances saw a decline of 4%, primarily driven by the high interest regime and challenging economic conditions that resulted in a moderate credit appetite.

Asset Quality

Asset quality was a primary point of focus during the year, as deterioration of asset quality was noticeable across the industry due to slow down in the economy. The Bank’s Stage 3 loans and advances amount also increased by 29% to LKR 324.9 billion. The Bank exercised stringent measures to monitor and moderate the risks and took a proactive approach by making a significant impairment provision during the year. The Bank’s impairment provision almost doubled in 2022 due to significant increase in credit risk. Exposure to customers in elevated risk industries remains a concern, as does exposure to Government in the form of investment and lending to state-owned enterprises. Multiple years of economic stress and the Government’s defaulting or delaying in honouring of commitments contribute significantly for impairment provisioning in 2022.

Liquidity and Investments

Liquidity was a key point of concern across the financial sector in 2022. However, the Bank was able to maintain its local and foreign currency liquidity positions above regulatory minimums. Close management of the Bank’s position was coupled with detailed cash and liquidity forecasting, which enabled us to respond suitably to regulator and industry demands in a challenging environment.

Foreign currency liquidity position of the Bank was allocated suitably in order to cater to national requirements and meet customer demands. We also focused on incentivising and driving remittance through a variety of measures during the year. Resulting remittance inflows and continued market leadership in this area supported the Bank’s foreign currency liquidity.

Investment in Government Securities grew by 45% to LKR 1,566.0 billion during the year.

Liabilities and Capital

Total liabilities grew by 13% to LKR 4.1 trillion during the year, buoyed by strong performance of the deposit book which saw significant growth of 16%. The Bank’s deposit base reached to LKR 3.3 trillion by the end of the year, displaying continued customer confidence and BoC’s market leadership position. This also reflects a shift of customer interest to time deposits and increase in local currency deposits coinciding with increased rates, high inflation, and volatility in the equity market. Increased appetite for time deposits led to growth in the LKR time deposit base to LKR 1.6 trillion in 2022 from LKR 1.4 trillion in the previous year. Coinciding decrease in savings base due to higher cost of living caused the Current and Savings Account (CASA) ratio to decrease from 36% to 29% during the year. However, the Bank managed its liquidity position strategically despite liquidity stress prevalent in the market.

In line with distressed economic conditions and the Government’s fiscal position that was not conducive to infusion of capital, the Bank sought to strengthen its capital base through internally generated funds and management of dividend payments. Growth prospects were constrained due to stresses on capital requirements aligned with deterioration of asset quality across the sector.

The Bank’s Tier II capital was enhanced by issuing LKR 6,490 million of BASEL III compliant subordinated Tier II debentures in 2022.

CBSL provided direction during the middle of the year, permitting draw down on capital conservation buffers and minimum capital requirements. However, we were able to navigate the year while maintaining capital adequacy ratios without utilisation of buffers.

Group Performance

Contribution of subsidiaries to the Group’s performance remains below 1%. The Bank manages its subsidiaries through a well-defined subsidiary charter, which sets out management processes and standards for subsidiaries, including systems for addressing the areas of Risk, Governance, Finance, Internal Controls, and Legal matters.

During the year, Property Development PLC, which was a subsidiary of Bank of Ceylon, has been delisted from the official list of the CSE with effect from 27 October 2022. A total of 1,573,272 shares have been repurchased by the Company for a total consideration of LKR 287.9 million under the delisting process. As at 31 December 2022, the issued and fully paid number of ordinary shares stood at 64,426,728. With the delisting process, the shareholding of BoC was adjusted to 97.89% from 95.55%.

Further, Merchant Bank of Sri Lanka and Finance PLC issued LKR 67.7 million unsecured, subordinated, redeemable, listed debentures during the year.

Sri Lanka’s economic recession presents a number of challenges for the Bank as we look forward to 2023 and beyond, with the full impact of the ongoing economic crisis yet to be seen. Amidst these uncertainties, and possible contraction of the economy in the forthcoming year, the Bank will focus on medium-term moderate growth in 2023 that would ensure it is well positioned to accelerate alongside the Country’s revival trajectory.

As a state bank and responsible corporate citizen, we have aligned the Bank’s strategies and plans with national priorities. We are gearing the Bank’s business model to best serve our stakeholders in 2023 and beyond. Priority allocation of liquidity and capital will cater to the country’s essential requirements by optimising stakeholder expectations. The Bank has plans in place to continue scaling up efforts to engage with customers, support their business revival, and provide for their long-term sustainability.

We plan to scale up green lending and rollout of ESMS practices driven by the Bank’s ESMS policy and adhering to CBSL roadmap for Sustainable Finance.

MSME sector will be a highly focused sector on growth prospects of the Bank by serving both traditional and millennial customers.

The Bank’s financial reporting and internal processes are undergoing continued digitalisation and we expect them to play a key role in supporting informed and timely decision-making in the years ahead. In addition, we remain committed to upholding international best practices in financial and sustainability reporting in line with the Bank’s ethos of transparency, accountability, and corporate responsibility.

The Bank will focus on resilience in 2023 and beyond, remaining watchful with balance sheet growth and prioritising stability of the Bank and strength of the balance sheet over short-term profit.