Global Economy

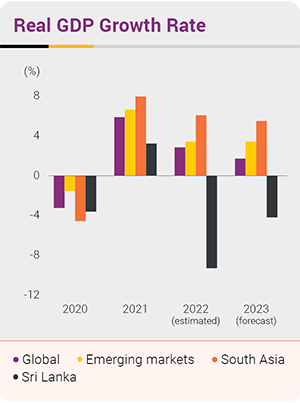

Economic activity, which was severely hampered by the pandemic in the previous years, saw continuation of COVID-19 pressures as China responded to rising caseloads that peaked in late 2022; leading to prolonged lockdowns and delayed reopening of borders. Additionally, escalation of the conflict between Russia and Ukraine into wider geopolitical turbulence, further disrupted global energy markets and intensified pressure on already fragmented supply chains. The conflict in Europe swept the global economy back into crisis mode and affected global growth prospects. However, reopening of economies towards the end of the year, particularly in China, contributed to an uptick as overall GDP growth in 2022 was estimated at between 2.9% and 3.4% .

The ongoing conflict in Ukraine continued to impact prices of key global commodities in 2022 as oil, gas, steel, and grain prices reflected the turbulent geopolitical climate, even as economic sanctions against Russia have added to the market impact. While commodity prices saw a gradual decline towards the end of the year, currency depreciation especially in developing and emerging economies has resulted in persistence of high costs in local currencies.

Rates of inflation reaching the highest point in several decades remained a significant concern for many countries, resulting in a concentrated impact on communities as cost-of-living climbed steeply and impacted household budgets while eroding purchasing power. Inflationary pressures declined somewhat towards the end of 2022, through the concerted efforts of the Central Bank driven monetary tightening and resulting slowdown of economic activity. However, high core inflation has persisted in many countries, setting the stage for continued inflationary pressures to be felt across the globe in the year to come. Continued intervention from central banks in the form of raising interest rates is expected to increase the cost of borrowing for consumers and businesses who are already grappling with higher cost of goods and services.

ii World Bank. 2023. Global Economic Prospects, January 2023. Washington, DC: World Bank.

Sri Lankan Context

On the back of two years of economic challenges following the Easter Sunday attacks and the COVID-19 pandemic, Sri Lanka experienced the fallout of multiple economic shocks that pronounced the effects of long-standing structural issues and fiscal, external sector, and financial sector imbalances. 2022 proved to be the most challenging year for the Country since achieving independence. With estimates indicating Sri Lanka’s economy could have contracted by as much as 9.2% in 2022ii, this stark turnaround reversed the gains of 2021, in which the economy had displayed signs of a slow recovery and an overall GDP growth rate of 3.3%.

The Country’s fiscal position that had been deteriorating over the last two years amidst reduced government revenue and increased expenditure, worsened significantly during the year. 2022 saw the state’s foreign reserves reach precariously low levels as servicing obligations and a growing import bill pressured an already cash-strapped position.

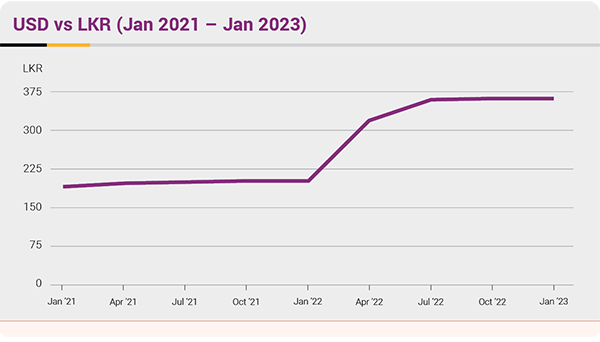

Inward remittances that had seen a decline in the previous years continued to impact the Country in 2022, alongside sluggish recovery in tourism earnings. Following the Central Bank of Sri Lanka (CBSL) decision to float the exchange rate in March 2022, the SL Rupee depreciated sharply. Sri Lanka’s import costs bore the brunt of rising energy prices in line with global trends, and were even more pronounced because of the depreciating Rupee. At the same time, the Government announced default of foreign debt obligations at the beginning of the second quarter, resulting in a downgrade of sovereign credit rating.

Source: Central Bank of Sri Lanka

During this period, shortages in import of essentials such as fuel, gas, and pharmaceuticals were commonplace, leading to disruptions to business and transport, social unrest, public protests, and change in Government at the beginning of the third quarter.

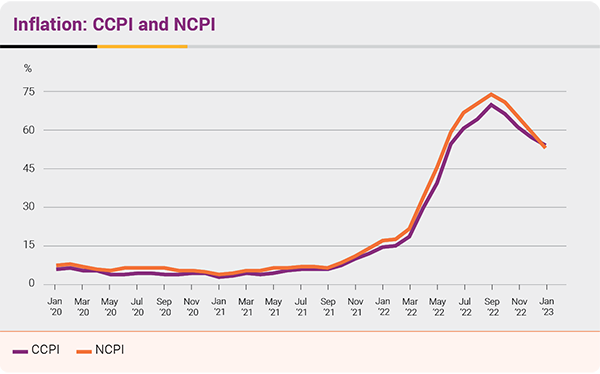

Sri Lanka’s inflation, meanwhile, reached to extraordinary levels, peaking at nearly 70% in the last quarter of 2022. In response to hyper-inflationary pressures, CBSL took steps to tighten monetary policy and raise interest rates by a significant margin.

Source: Central Bank of Sri Lanka

Shift to a high interest rate regime, a depressed economic environment, and rating downgrades placed severe pressure on the Country’s financial sector.

Economic Stressor

Float of exchange rate

Stakeholders impacted

Floating of the exchange rate narrowed influence of the kerb-market and incentivised inward remittances through formal channels. Further relaxing of FOREX related restriction in 2023 indicates continued moves towards a market-driven exchange rate.

Export customers recognised an increase in margins and enjoyed the benefits of greater price-competitiveness, as did the Country’s tourism sector.

However, import-reliant customers recognised an increased expenses and demand decline that eroded margins. Import restrictions also hampered business. Heavy reliance on imported inputs also impacted a much wider range of local industries and contributed to cost-push inflationary pressure. Customers representing local industries benefited by import substation saw new growth opportunities.

Retail customers recognised an increased cost of goods and services that had an import footprint, and price increases across the board due to rising transport costs. Communities saw commodity shortages and price escalation that placed pressure on food security. Price escalation even affected what was considered basic foods: such as dhal, rice, and dried fish, all of which had a significant import footprint.

Hyper-inflationary environment

Stakeholders impacted

Extraordinary inflationary pressures resulted in significant increase in cost of living felt by all citizens of the Country. Corporate customers were also affected by inflationary pressures as cost of services and utilities increased dramatically.

Foreign exchange liquidity crisis

Stakeholders impacted

Forex became one of the most critical and limited resources in the Country, during 2022.

Lack of foreign exchange liquidity led to shortages of essential goods. The impact was felt broadly, including in transport, power and energy, food, and healthcare. Disruptions to transport and electricity hampered communities across the Country and placed heavy pressure on business continuity for customers.

The FOREX liquidity crisis also placed pressure on customers with regard to servicing obligations and making essential payments.

Sovereign default and ratings downgrade

Stakeholders impacted

Default on sovereign debt obligations during 2022 led to downgrade of Sri Lanka’s Sovereign rating, and ratings downgrades for financial institutions and many corporate customers across the board.

High-interest regime

Stakeholders impacted

Sri Lanka transitioned from a low-interest to a high-interest regime almost overnight, as the Central Bank of Sri Lanka (CBSL) increased policy rates by 7% in April 2022. Policy rates were a primary tool utilised by the CBSL in managing inflation during the year. Further measures by the regulator to raise the SDFR and SLFR in 2023, are in line with continued monetary policy measures to curb inflation.

A three-fold increase in AWPLR lending rate to corporate customers – served as a dampener for credit growth to the private sector, which also saw reduced demand due to other external economic stressors. Corporate customers faced severe escalation in funding cost and margin requirements, with largest impact felt by highly leveraged businesses.

Retail borrowers were sandwiched by escalated cost of living and increased loan repayment rates. Borrowers on variable interest rates (VIR) were hard hit, but were supported by regulator-driven concessions such as rescheduling and restructuring of facilities and concessionary rate adjustments.

Meanwhile, depositors saw gains from higher interest rates and the market saw increased interest in time deposits.

Banking Sector

Sri Lanka’s Banking sector saw deterioration of asset quality across the board as borrowers were hard hit by the Country’s economic crisis, further compounded by high interest rates. The year saw Licensed Commercial Banks (LCBs) impacted by higher provisions, coupled with increased expenses and taxes; all of which impacted profits.

Erosion of disposable income, deteriorating business prospects amidst the breakdown of economic fundamentals, fuel and energy crises, social unrest, and political instability severely affected business activity. Apart from limiting credit growth in the private sector, these economic pressures also resulted in higher provisioning in loans and advances. As a result of these changes, and continued uncertainties, Stage 3 loans ratio grew significantly.

However, banks saw a significant increase in Net Interest Income (NII) during the course of the year, in line with increasing interest rates. At the same time, depreciation of the Sri Lankan Rupee positively affected Bank’s Income Statements by way of revaluation gains.

Amidst pressures on liquidity and capital adequacy, the banking sector was given a reprieve as the regulator permitted LCBs to drawdown on capital conservation buffers.

Challenges faced by the Banking Industry

|

Access to foreign currency funding sources limited due to sovereign downgrade |

|

Decline in CASA ratio resulting in higher cost of funds |

|

High interest rates resulting in narrower margins |

|

High inflation leading to escalation in operating cost |

|

Erosion of customer cashflows led to deteriorated asset quality |

|

Limitations to loan growth due to low demand for credit and high interest rates |

|

Continuous disruption to operations due to COVID-19, fuel crisis, and political and social unrest |

|

Slower growth in capital investments and expansion |

|

Fee income affected by import and export restrictions |

Our Response

|

Drive remittances to the country |

|

Facilitated to manage the foreign currency flow of the country |

|

Provided moratoria to customers in need |

|

Introduced a revival mechanism instead of recovery |

|

Ensured continous banking services amidst socio-economic crisis |

|

Employees are compensated for increasing cost of living |

|

Strategically managed the liquidity stress |

|

Strengthened the Balance Sheet through prudential provisioning |

The global economy is projected to experience a decline in growth in 2023, with growth rates predicted to fall to 2.9%i. The continued response of central banks to inflationary pressures, especially in advanced economies where monetary authorities are attempting to balance management without triggering a recession, would be critical to Global economic prospects. Persistence of the conflict in Ukraine is another factor that would have a decided impact on economic activity across the globe in 2023 and beyond.

While global inflation is projected to decline to 6.6% in 2023, it is expected to remain well above pre-pandemic levels. At the same time, some emerging markets and developing countries will continue to experience extraordinarily high levels of inflation. In this scenario, protecting communities from rising costs will be a point of focus for Governments across the Globe.

i International Monetary Fund. 2023. World Economic Outlook Update, January 2023