Global Economy

The global economy, which had shown remarkable resilience during its post-pandemic recovery, went into a tailspin once again following Russia’s invasion of Ukraine, and its widespread fallout on many fronts. The International Monetary Fund (IMF) projects global growth to slow down from 6.0% in 2021 to 3.4% in 2022, and plunging further to 2.9% in 2023. It also forecasts global inflation to rise from 4.7% in 2021 to 8.8% in 2022, declining to 6.6% in 2023, and 4.3% by 2024.

Mirroring the views of its Bretton Woods twin, the World Bank (WB) states, “As central banks across the world simultaneously hike interest rates in response to inflation, the world may be edging toward a global recession in 2023 and a string of financial crises in emerging markets and developing economies”.

Morgan Stanley expects global GDP growth to reach a modest 2.2%, narrowly defying recession, while offering growth predictions for the following regions for 2023:

| Country | GDP (%) |

| US | 0.5 |

| Euro Area | -0.2 |

| UK | -1.5 |

| Japan | 1.2 |

| Emerging Markets | 3.7 |

| China | 5.0 |

| India | 6.2 |

| Brazil | 1.2 |

Similarly, Standard & Poor (S&P) expects the Asia-Pacific region to achieve real growth of about 4.3% in 2023, while Europe and the U.S. could face recession. Economic growth in the Asia-Pacific region, which produces 35% of world GDP, will be supported by regional free-trade agreements, efficient supply chains, and competitive costs.

Sri Lankan Economy

According to the World Bank’s latest South Asia Economic Focus and the Sri Lanka Development Update, real GDP is expected to fall by 9.2% in 2022 and a further 4.2% in 2023. “The fluid political situation and heightened fiscal, external, and financial sector imbalances pose significant uncertainty for Sri Lanka’s economic outlook”, the report further states.

However, the Asian Development Bank (ADB) remains upbeat over Sri Lanka’s progress towards economic recovery, as the Government has been working on a stabilisation plan, which it described as being “very comprehensive”.

In fact, the Government has also discussed a policy loan amounting to USD 700 Mn with the World Bank, along with a further USD 1.2 Bn from the ADB. Once the IMF programme amounting to USD 2.9 Bn is finalised, the Government could work towards achieving debt sustainability.

Going a step further, the World Bank has approved Sri Lanka’s request to access concessional financing from the International Development Association (IDA). This will help implement reform programmes aimed at stabilising the economy and protecting millions of people facing poverty and hunger.

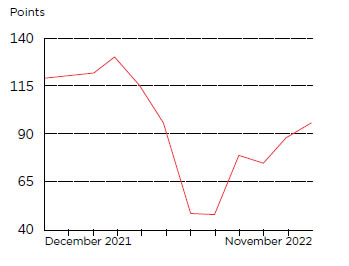

As a reflection of all these positive developments, including implications of the Budget that has just been presented, the LMD-NielsenIQ Business Confidence Index (BCI) has climbed nine basis points from 89 in October to 98 a month later, which is only 11 basis points shy of where it stood last year, at 109.

Banking Industry

Sri Lanka’s default of its foreign debt in April 2022 after two years of money printing triggered the worst currency crisis in the history of the country. This was worsened by the SLR falling from 182 to 360 to the US dollar within two years and inflation hitting 70%.

International Banker, the respected industry publication, commenting on the Sri Lankan banking sector states, “the dearth of foreign-exchange reserves that banks now hold has become so acute that supporting the necessary import purchases is severely straining their cash flows”, and therefore undermining their ability to perform their supporting role in stabilising the economy.

Commenting on Non-Performing Loans (NPLs), the Central Bank of Sri Lanka (CBSL) has stated, “Asset quality of the sector deteriorated in terms of stage 3 loans to total loans ratio. Stage 3 loans increased by LKR 475.1 Bn, recording a growth of 56.9 % and reached LKR 1.3 Tn as at end August 2022”.

On a positive note, the banking industry is expected to improve, as there are several factors favouring a drop in market interest rates, despite fears of domestic debt restructuring. This includes a fall in inflation, improvements in liquidity in the dollar market, and reduction in inter-bank liquidity shortage. The government has also raised taxes and private credit has fallen.

Looking Forward

The Sri Lanka Government’s budget for 2023 aims for an ambitious economic growth of 7–8%, increasing international trade as a percentage of GDP by more than 100%, annual growth of USD 3 Bn from new exports from 2023 to 2032, FDIs of more than USD 3 Bn in the next 10 years, and creating a highly skilled internationally competitive workforce during the same period. The budget also plans to bring inflation down in the medium term.

The government proposes to increase personal and corporate income tax from 24% to 30%, which could see an improvement in revenue. However, reducing expenditure could be difficult as total spending by the Government for the coming year could be in the region of LKR 5.9 Tn, with capital expenditure making up 20.9% of that amount.

The budget is further intended to increase tax revenue by 69%, which could bring in SLR 3,130 Bn, which could lead to a budget deficit of 7.9% in 2023 as compared to 9.85% this year. Restructuring of some of the largest loss-making State-Owned Enterprises (SOEs) is also on the cards, which could rein in state expenses further.

While these are positive developments in terms of boosting the state’s coffers, earning more foreign exchange is the need of the hour, with several new developments anticipated by the Government in this regard.

Though workers’ remittances have fallen 31% to USD 3.8 Bn in 2023, the Government hopes to earn USD 1 Bn per month by the end of 2023, as the number of individuals seeking overseas employment has risen considerably.

Despite a sizable drop in tourist arrivals this year, Sri Lanka tourism has set an ambitious target of 1.5 Mn for next year and 3 Mn for 2024. A revenue target of USD 5 Bn is expected from high-end travellers, and a 10-year tourism plan is to be unveiled next year. Moratoriums extended to the tourism sector, while causing complications in the banking sector, are expected to help SMEs in tourism to make a successful comeback in the coming year.

While these are positive developments, the final word on the nation’s economic outlook should be left to the CBSL. To quote: “The IMF-EFF programme will provide an opportunity to embark on much needed and long neglected structural adjustments in a more structured and timely manner, which will be instrumental in shaping the economy to progress on a trajectory of greater stability and sustained growth”. CBSL further adds: “Considering the progress that has been made thus far in relation to the IMF-EFF programme and debt restructuring negotiations, and the reforms that have already been undertaken, and those that are to be implemented in the period ahead, the economy is expected to transition on to the path to recovery from the latter part of 2023”.