Key Business Line Review – Personal Banking

personal Banking serves over 3.2 mn. customers , facilitating socio-economic progress of all communities in the country processing over 600,000 transactions each day. Core activities include providing access to banking services and supporting wealth creation for our customers through an evolving portfolio of investment, credit and transactional products.

Inclusive Growth

Figure 22

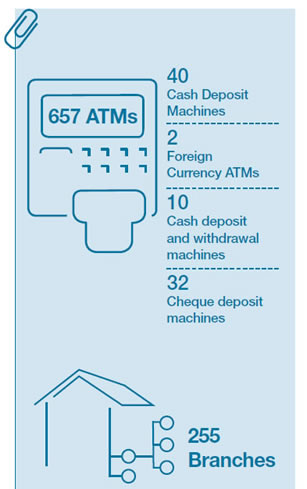

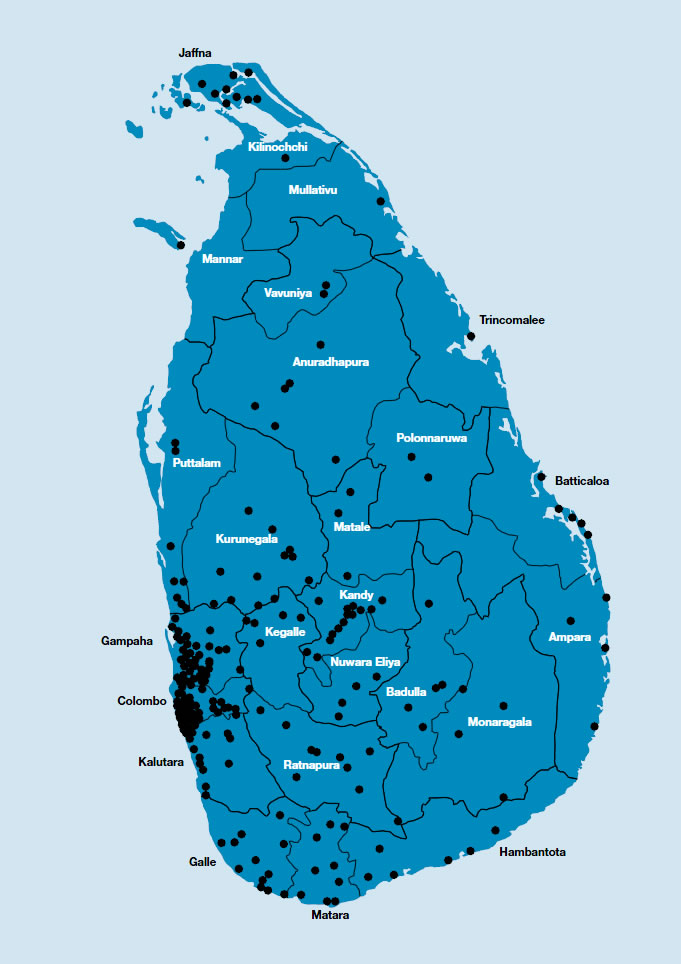

A key driver of growth for the Bank with business strategy closely aligned to the country’s development goals, Retail Banking plays an important role facilitating access to banking. A strong customer franchise supported by a network of 255 branches, 657 ATMs and over 912 customer touch points provides our customers unparalleled reach while increasing digitisation and simplification of processes provide customer convenience and a platform for scalable growth.

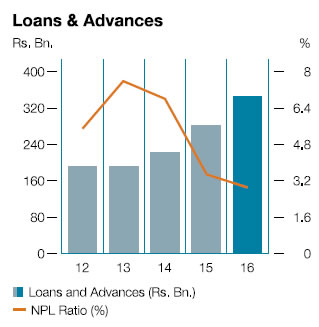

Personal Banking contributed 34.10% to the Bank’s asset growth and 63.86% to liability growth while improving asset quality due to targeted marketing. Rigorous monitoring processes are reflected in the reduced impairment charge and the NPL ratio of 2.9%, an improvement of 3.5% in 2015. NII increased despite narrowing spreads due to volume growth as we maintained our commitment to discourage consumption-based lending, focussing on responsible lending that would create long-term value for our customers. Fee-based income increased during the year driven by growths recorded in trade finance and card-related operations. Client acquisition during the year also augurs well for future growth prospects of Personal Banking as these relationships typically deepen over time.

Focus on Customer Needs

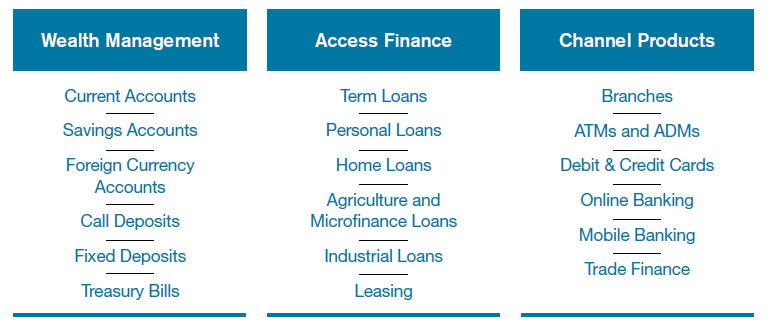

A wide-ranging product portfolio catering to every segment of the population throughout the customer lifecycle has been a core strength for Personal Banking (Figure 21).

Figure 21

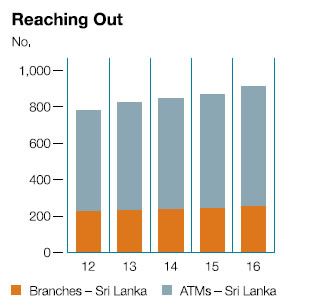

Reaching Out

The branch network expanded by nine new branches in Western, Southern and Eastern Provinces as they are vital to maintaining the customer relationships supporting our growth strategy. We also opened an automated banking centre in 2016 taking the total of our branch network to 255 (Graph 43). Two new Agriculture and Microfinance units were opened in Matara and Pottuvil taking the total of these specialised units to 15. An overall penetration rate of approximately 18% in Sri Lanka is a testimony to our inclusive approach of banking.

We grew the network of ATMs to 657 in 2016 which continues to be one of the largest ATM networks in the country

(Figure 22). Key upgrades to these 24-hour sentinels during the year include:

- Security: We have upgraded the entire ATM network to EMV Chip capability to enhance security against fraud which has been identified as a key risk for the industry.

- Convenience: Expanding the ATM network and enhancing their capability by facilitating deposits and cardless transactions

- Efficiency: Launching of the Over the Air Pin (OTAP) for debit and credit cards, enabling customers to obtain PIN numbers via registered mobile phones.

Bank introduced channel products such as Easy POS – smart phone linked mobile POS system for card transactions, and online real time cash deposit and withdrawal machine to improve the customer convenience during the year.

Graph 43

Customer Centric

The product portfolio was reviewed to meet changing customer expectations resulting in the modification and relaunch of two products and the launch of several new products. ‘Isuru’, the minor savings product was re-launched with enhanced features reflecting customer expectations, contributing to growth of our deposit base. Diribala, a term loan product for SMEs introduced in 2015 gained traction during the year due to extended repayment periods and grace period matching cash flows. This product was extended to Diribala Green Development Loans to support investment in renewable energy solutions and effluent and waste treatment plants for SMEs. Diribala Foreign currency products also enable SMEs to borrow in three major currencies to hedge their foreign currency risks. A new microfinance product was launched during the year to finance micro-entrepreneurs based on cash flows sans guarantees is gaining traction.

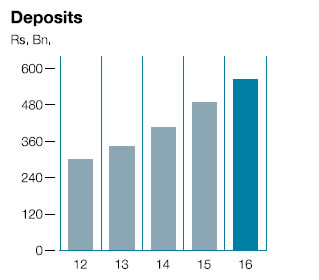

Growing Our Deposit Base

Personal Banking deposit growth was over 16% during the year reaching Rs. 565 Bn. despite a challenging operating environment. The difference between rates for savings and fixed deposits increased in 2016 resulting in a declining proportion of current and savings deposits in the deposit mix. Despite this, the Bank’s CASA ratio of 41.67% remains higher than the industry.

A strong customer franchise coupled with aggressive marketing campaigns enabled us to acquire over 400,000 savings customers which is the typical commencement of a Personal Banking relationship and are confident of our ability to cater to their varying needs as we deepen the relationships. It is noteworthy that we retained majority of fixed deposits due to strong relationships, reputation and financial stability despite intense competition from competitors.

Graph 44

Responsible Lending

Growth in retail loan portfolios was driven by the Bank’s continued commitment to the SME sector in alignment with the Government’s vision, focussed on value creation for individuals through home loans and Microfinance. The Bank worked with reputed developers to provide financing for purchase of condominiums during the year catering to the demand for urban housing. A commitment to responsible lending resulted in diminished pawning activity while increases in border tariffs dampened leasing activity.

Graph 45

Focus on SMEs

Building on our track record as the lead investor in SMEs, we have committed more resources to expanding our role in this vital engine of growth for the country. Accordingly, we have structured a specialised Development Credit Department to focus on developing solutions for SMEs through specialised knowledge and insights in to the challenges faced by the sector. Our core strengths have been strong relationships, targeted marketing, flexibility and efficient service.

Key initiatives implemented during the year include:

- Capacity building programmes for entrepreneurs – As the first private bank to collaborate with Central Bank we conducted seven programmes including dedicated programme exclusively targeting women entrepreneurs benefiting over 850 entrepreneurs in 2016, extending the Diribala Vyapara Pubuduwa programme which commenced in 2011. Since inception, we have completed a total of 59 programmes benefiting 5,229 entrepreneurs.

- Employee capacity building – We conducted intensive training to ensure a continuous pipeline of talent for SME operations. Each branch now has an SME specialist trained to assess and monitor SME customer needs and offer appropriate solutions. They are supported through the intranet which contains up to date information on developments in the sector and industries relevant to the sector. The main beneficiary of this initiative is the client who receives a more informed and efficient service.

- Simplification of loan documentation – Application forms and other documentation were simplified to reduce processing time while ensuring a sufficiency of information for evaluation and regulatory requirements. This initiative was undertaken to reduce the customer burden and further ease their access to finance.

- Collaborative partnerships – We maintained a close rapport with external organisations including Government Agencies to provide technical support for SME’s.

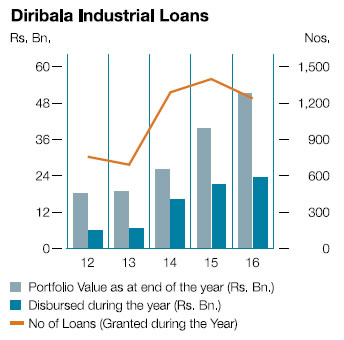

Diribala, the Bank’s branded SME industrial loan is the unmatched market leader in the segment with repayment periods matched to cash flows and attractive interest rates. From the Bank’s perspective, a robust evaluation process facilitated managing asset quality. The loan portfolio is now over Rs. 50 Bn. with NPL’s amounting to less than 1.6% as at the year end. Despite increasing interest rates and non-availability of donor funds which dampened the potential for growth, the Bank was able to grow this portfolio by 30% (Graph 46).

Graph 46

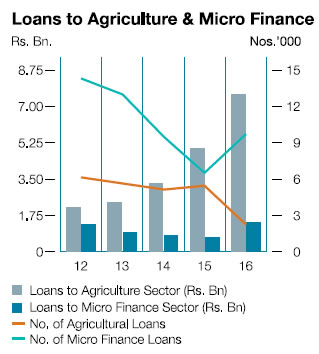

The agriculture loan portfolio was segregated to agri SMEs and agri Microfinance to facilitate better solutions to new segments resulting in a transfer of approximately Rs. 500 Mn. to the microfinance portfolio. The sector witnessed renewed interest from entrepreneurs as Government credit lines spurred activity particularly in dairy farming. Commodities exporters and agristockists also grew their businesses. Large scale investments in the sector have also spurred activity in the SME segment. These factors enabled the growth over 65% of the streamlined agriculture portfolio. The Bank’s activities in this segment are supported by 15 Agriculture and Microfinance Units and a centralised Agricultural Loans unit with highly specialised teams with an understanding of the industry contributing to enhanced the scope of assessment, monitoring and customer service. It has also served to maintain asset quality with less than one percent NPL ratio.

Focus on Microfinance

The microfinance portfolio comprising loans below Rs. 500,000/- which now includes agro loans demonstrated a strong growth of nearly 20% in 2016. Learning from our past experiences, our current microfinance products are linked to supply chains rather than groups which has enabled us to significantly improve the asset quality in this portfolio (Graph 47).

Adopting a holistic approach, the Bank introduced a micro savings product DiviSaru to support the customer life cycle approach to building our microfinance customer base. This also resulted in increasing the customer base by nearly 20,000 in 2016 supporting deposit mobilisation efforts of the Bank with a portfolio growth of over 15%. The above changes will facilitate building a microfinance customer-base within the Bank.

Graph 47

Enhancing Our Customer Experience

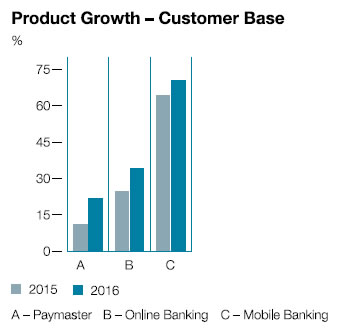

Customers increased their usage of the electronic banking channels during the year resulting in high growth rates for online banking, mobile banking and the Bank’s flagship product for corporates and SMEs, Paymaster. Key trends supporting growth in this area included the declining trend in prices of tablets, smartphones and computers resulting in higher penetration levels.

Online Banking, the Bank’s internet-based payment system witnessed a positive growth of around 10% in the value of transactions and around 30% in the number of transactions evincing growing customer confidence and familiarity with this channel. Developed on the Microsoft. Net platform, it consists of the Personal and Corporate Banking solutions (Graph 48).

The focus in 2016 was to enhance the corporate payments platform such as bringing in the bulk payment options to online banking platform, thus enabling the corporate clients to automate all of their single entry payments and also to avail themselves with payment limits according to their signature rules. Coupled with the features such as Multilevel Authorisation, Administrator User, Single User ID for several company accounts – shared ID etc., enhanced an already robust product.

Graph 48

Island wide product awareness campaigns to promote the features of Corporate and Personal Banking solutions to encourage usage, were a key factor in driving growth in Online Banking. Furthermore, free registration campaigns through the branch network, User activation campaigns with cash/iPhone rewards and continuous text/EDM circulations on product features propelled usage as well the new registrations. Unique features such as the ability to view the images of the deposited cheques (single or bulk) and paid cheques along with scheduling of bill payments for future dates (on the actual due date) provide a competitive advantage to our product. At present, Commercial Bank is the only Sri Lankan Bank to provide online cheque viewing facilities to customers.

The Bank’s performance in the mobile banking segment is noteworthy, especially taking in to consideration the unprecedented growth achieved in 2015. The launch of yet another unique feature titled ‘e passbook’ was a contributory factor towards the mobile banking growth in 2016. Progress in this segment is vital for the remittance business of the Bank as mobile banking provides the required connectivity.

Performance of PayMaster, has been particularly pleasing with a growth of 22% during the year and this was driven by increased customer migration and usage. Planned enhancements for 2017 are expected to empower corporate customers to initiate and complete more transactions with enhanced security features and analytical capability.

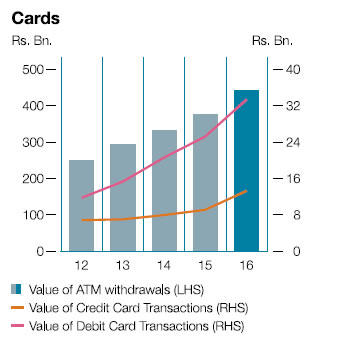

Cashless Payments

Cashless payments using debit cards and credit cards in Sri Lanka increased by over 16% and 13% supported by growths in POS terminals and customer acquisition. Card usage measured by the number of debit and credit card transactions increased around 25% each respectively while the value of transactions grew by 25% and 22% by the 3rd quarter of 2016 reflecting the increased popularity of debit cards. POS terminals in the country increased by 7% to 41,283 by the 3rd quarter of 2016 supporting the increased use of cards. ATM transactions in the country also increased by 9% in volume and 18% in value up to September 2016 supporting the overall infrastructure in the country for card based transactions.

Card operations at the Bank gained a new vibrancy as we set out to aggressively grow our credit and debit card portfolios. The Bank continues to be the market leader in debit card spending recording over 30% growth in 2016 supported by approximately 30% increase in cards issued during the year. We focussed on aggressive expansion of our credit card business achieving exponential growth in the cards issued and a substantial growth in credit card spend in 2016. The credit card portfolio also grew by approximately 40% and the total credit card outstanding to reach Rs. 6.7 Bn. at the year end as we captured market share (Graph 49).

Graph 49

Growth in card operations was supported by the launch of premium cards such as Visa Infinite, Signature and Master Card World which were launched to address the lifestyle requirements of the affluent customers. Customer convenience was facilitated through the issuance of Near Field Communication (NFC) enabled cards for all credit cards and new debit cards reducing transaction times for the mutual benefit of the customer and the merchant. Introduction of OTAP for credit and debit cards expediting the dispatch and receipt of the PIN by the cardholder in a secure manner was an innovation in the entire industry.

Issue of the Ransalu privilege card for the apparel sector employees jointly with the Joint Apparel Association Forum and Channel 17 enabled them to access discounts for essential items, hospitalisation, pharmaceutical products, clothing and other products. The Bank also issued the Smart Tea Card facilitating automation of the procurement of tea leaves and settlement for bought leaf using Sony ‘FeliCa’ Near Field Communication (NFC) technology in the market, enabling its promoter Smart Metro (Pvt) Ltd. to deploy a Debit Card cum Identification Card for tea leaf suppliers.

Bancassurance

Growth in Bancassurance fee income and number of policies were over 12% and 25% respectively reflecting challenging market conditions. The Bank worked with eight partners for Life Insurance and eight partners for General Insurance following the recent segregation of activities. Offering unmatched reach to partners through our network of branches, it enables the Bank to provide a seamless service to its customers for their entire range of financial needs. Internal competitions and the issue of DTAP for pensioners supported the growth of the product. Pressure from Brokers associations and possible changes in legislation are key threats to the growth of this business line together with intense competition from both insurance brokers and other banks.

Network of Delivery points in Sri Lanka

Western Province

Colombo

ABC* M

Athurugiriya

Attidiya

Avissawella

Bambalapitiya

Bambalapitiya (Majestic City) K

Baseline Road

Battaramulla

Battaramulla (Arpico Super) K

Bokundara (Minicom) K

Boralesgamuwa

Boralesgamuwa (Laugfs Super) K

Borella A

City Office

Colombo 07 G

Colombo Gold Centre

Dehiwela

Dehiwela (Arpico Super) K

Delkanda

Duplication Road

eBanking

Elite A

Foreign D

Grandpass

Hanwella

Homagama

Hulftsdorp

Hyde Park Corner (Arpico Super) K

Kaduwela

Katubedda

Katubedda (Minicom)

Keyzer Street

Kirulapone Second

Kirullapone

Kohuwala

Kohuwala (Keells Super) K

Kollupitiya

Kollupitiya (Liberty Plaza) K

Kotahena A

Kotikawatte A

Kottawa

Maharagama A

Maharagama (Laugfs Super) K

Malabe

Maradana

Mattegoda (Laugfs Super) K

Moratuwa A

Moratuwa (Laugfs Super) K

Mount Lavinia

Mutwal

Narahenpita

Narahenpita (Ronan Inter’l) K

Nawala

Nawam Mawatha

Nawinna (Arpico Super) K

Nugegoda A

Old Moor Street

Padukka

Panchikawatte

Pelawatte (Laugfs Super) K

Pettah

Pettah Main Street E

Piliyandala

Pita Kotte

Rajagiriya

Rajagiriya (Keells Super) K

Ramanayake Mawatha

Ratmalana

Reid Avenue J

Thalawathugoda

Union Place

Union Place (Keells Super) K

Vauxhall Street (SLIC)

Ward Place L

Wellawatte I

Wellawatte Second

World Trade Centre

Gampaha

Bandarawatte (Laugfs Super) K

Biyagama

Delgoda (Laughs Super)*

Divulapitiya

Ekala

Gampaha A

Gampaha (Keells Super) K

Ganemulla

Hendala (Keells Super) K

Ja-Ela

Ja-Ela (K-Zone) K

Kadawatha

Kadawatha (Arpico Super) K

Kandana A

Katunayake BIA Arrival Lounge M

Katunayake BIA Departure Lounge*

Katunayake FTZ

Kelaniya*

Kiribathgoda J

Kiribathgoda (Laugfs Super) K

Kirindiwela

Kochchikade

Makola

Minuwangoda

Mirigama

Negombo B

Negombo (Arpico Super) K

Negombo Second

Nittambuwa

Nittambuwa (Nihal Super) H

Peliyagoda

Raddolugama A

Ragama A

Seeduwa J

Veyangoda*

Wattala

Wattala (Arpico Super) K

Weliveriya

Yakkala

Kalutara

Aluthgama

Bandaragama

Beruwala (Minicom) K

Horana

Horana (Wijemanna Super) K

Kalutara

Kalutara (Arpico Super) K

Katukurunda (Minicom) K

Matugama C

Panadura

Panadura (Keells Super) K

Panadura Second

Wadduwa

Sabaragamuwa Province

Kegalle

Kegalle A

Mawanella

Ruwanwella

Warakapola

Ratnapura

Balangoda

Eheliyagoda

Embilipitiya

Godakawela

Kahawatte

Kalawana

Kuruwita

Pelmadulla

Ratnapura

Ratnapura (Minicom) K

Southern Province

Galle

Ambalangoda

Baddegama

Batapola

Elpitiya

Galle City

Galle City (Minicom) *

Galle Fort

Hikkaduwa

Karapitiya

Koggala

Neluwa

Udugama

Hambantota

Ambalantota

Beliatta

Hambantota

Middeniya

Tangalle

Tissamaharama

Matara

Akuressa

Deiyandara*

Deniyaya

Kamburupitiya

Matara B

Matara (Keells Super) K

Matara City Office

Morawaka*

Urubokka

Weligama

Central Province

Kandy

Akurana (Minicom) K

Anniwatte (Nihals Super) K

Digana

Gampola

Gelioya (Arpico Super) K

Kandy A

Kandy (City Centre) K

Katugastota

Katugastota (Minicom) K

Kundasale (Dumbara Super) K

Nawalapitiya

Peradeniya

Pilimatalawa

Wattegama Ext. Office

Matale

Dambulla

Galewela

Matale

Nuwara Eliya

Hatton

Maskeliya

Nuwara Eliya

Thalawakelle

Uva Province

Badulla

Badulla

Badulla (Minicom) F

Bandarawela

Mahiyanganaya

Passara

Welimada

Monaragala

Kataragama

Monaragala

Wellawaya

Eastern Province

Ampara

Akkaraipattu

Ampara

Kalmunai

Pottuvil

Batticaloa

Batticaloa A

Batticaloa (Minicom) * E

Chenkalady

Kattankudy

Valaichchenai

Trincomalee

Trincomalee

North Central Province

Anuradhapura

Anuradhapura

Anuradhapura New Town

Kekirawa

Medawachchiya

Nochchiyagama

Thambuttegama

Polonnaruwa

Hingurakgoda

Kaduruwela

North Western Province

Kurunegala

Alawwa

Giriulla

Kuliyapitiya

Kurunegala B

Kurunegala (Minicom) K

Kurunegala City Office

Mawathagama

Narammala

Nikaweratiya

Pannala

Polgahawela

Wariyapola

Puttalam

Chilaw

Dankotuwa

Marawila

Nattandiya

Palavi

Puttlam

Wennappuwa (Arpico Super) K

Wennappuwa

Nothern Province

Jaffna

Chankanai

Chavakachcheri

Chunnakam

Jaffna G

Jaffna Stanley Road A

Kodikamam

Manipay

Nelliady A

Thirunelvely

Velanai

Kilinochchi

Kilinochchi

Kilinochchi (Minicom)*

Mannar

Mannar

Mulativu

Mulliyawalai

Vavuniya

Vavuniya

Vavuniya Second

* Branches opened in 2016

Banking Hours

| A | B | C | D | E | F | G | H | I | J | K | L | M | ||

| Weekdays | 9-3 | 9-3 | 9-3 | 9-3 | 9-4 | 9-6 | 9-6 | 9-6 | 9-6.30 | 9-8 | 9-9 | 9.30-7 | 10-5 | 24*7 |

| Saturday | – | 9-1.30 | 9-1.30 | – | – | 9-1.30 | – | 9-1.30 | 9-6.30 | 9-3 | 9-9 | 9.30-7 | 10-5 | 24*7 |

| Sunday | – | – | 9-1.30 | 9-1.30 | – | – | 9-1.30 | 9-1.30 | 9-6.30 | – | 9-9 | 9.30-7 | – | 24*7 |

| Bank Holidays/Poya* | – | – | 9-1.30 | – | – | – | – | 9-1.30 | 9-6.30 | – | 9-9 | 9.30-7 | – | 24*7 |

|

|

No. of Branches |

No. of ATMs |

|

Kandy District |

14 |

30 |

|

Matale District |

3 |

10 |

|

Nuwara Eliya District |

4 |

9 |

|

Central Province |

21 |

49 |

|

Ampara District |

4 |

7 |

|

Batticaloa District |

5 |

11 |

|

Trincomalee District |

1 |

3 |

|

Eastern Province |

10 |

21 |

|

Anuradhapura District |

6 |

12 |

|

Pollonnaruwa District |

2 |

8 |

|

North Central Province |

8 |

20 |

|

Kurunegala District |

12 |

38 |

|

Puttalama District |

8 |

17 |

|

North Western Province |

20 |

55 |

|

Jaffna District |

11 |

24 |

|

Killinochchi District |

2 |

4 |

|

Mannar District |

1 |

2 |

|

Mulative District |

1 |

2 |

|

Vavuniya District |

2 |

6 |

|

Northern Province |

17 |

38 |

|

Kegalle District |

4 |

10 |

|

Ratnapura District |

10 |

21 |

|

Sabaragamuwa Province |

14 |

31 |

|

Galle District |

12 |

30 |

|

Hambantota District |

6 |

13 |

|

Matara District |

10 |

21 |

|

Southern Province |

28 |

64 |

|

Badulla District |

6 |

11 |

|

Monaragala District |

3 |

6 |

|

Uva Province |

9 |

17 |

|

Colombo District |

77 |

205 |

|

Gampaha District |

39 |

125 |

|

Kalutara District |

13 |

32 |

|

Western Province |

129 |

362 |

|

|

256 |

657 |