Products

• Foreign Exchange dealings • FIS and futures trading • Commercial paper • Currency Swaps • Interest Rate Swaps, FRA’s, Caps,

Floors and Collars • Commodity price hedging • G7 and LKR FX options • DCD’s and other yield enhancing

structures

Core Competencies

• Availability of a fully customised

Treasury software package • Risk management unit with integrated

ALM/FTP and customer profitability • Competitive rates due to sufficient

FX resources • Possibility of mobilising foreign

currency funds

due to operations

outside the country • Possibility of mobilising local currency

funds due to well established and wide

branch network • Innovative & customised treasury

products • Strong relationships with foreign banks • Well trained Treasury team • Financial strength and image of the Bank • Hedging FX and interest rate risk • Market views on FX and interest rates • FIS trading • Highest rating among local Banks

Future Strategies

• To increase the fee-based income

through derivative products • To introduce structured products via

our branch network • To strengthen the role of ALCO with

a view to maximise gains and to

minimise risk • To improve risk management practices • To introduce Islamic banking to

attract Middle

Eastern clientele • To further streamline Treasury

operations • To ensure accuracy and timeliness

in decision- making • To become a dominant market maker

in Government debt securities • Focus on retailing structured products

via our network • Selling LKR FIS to foreigners

Overview

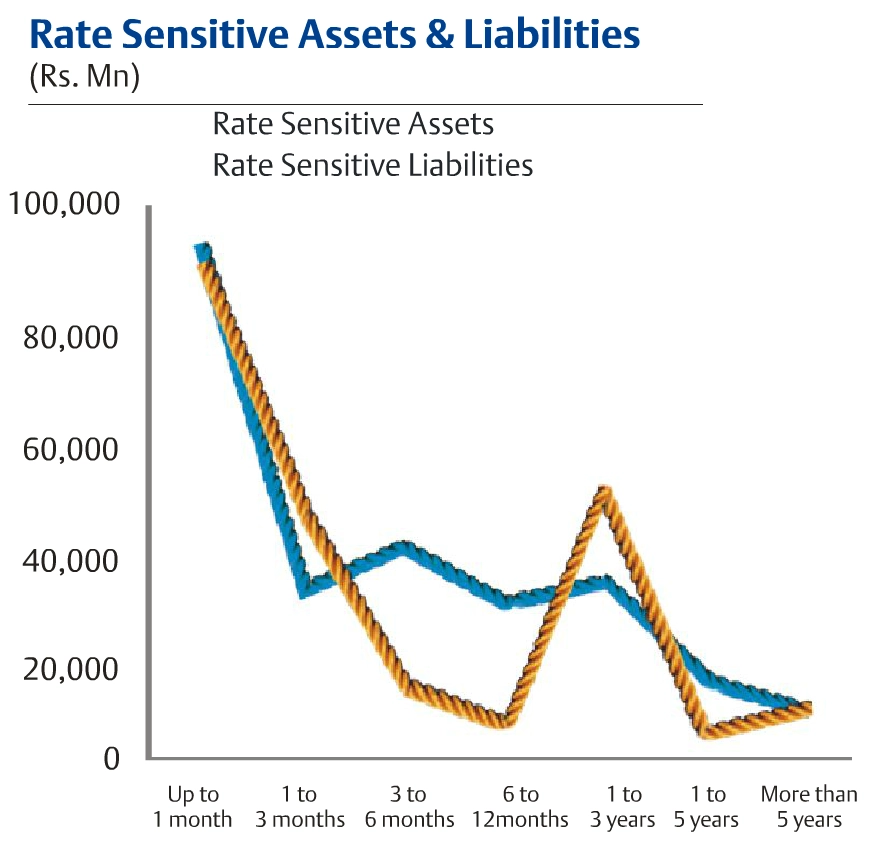

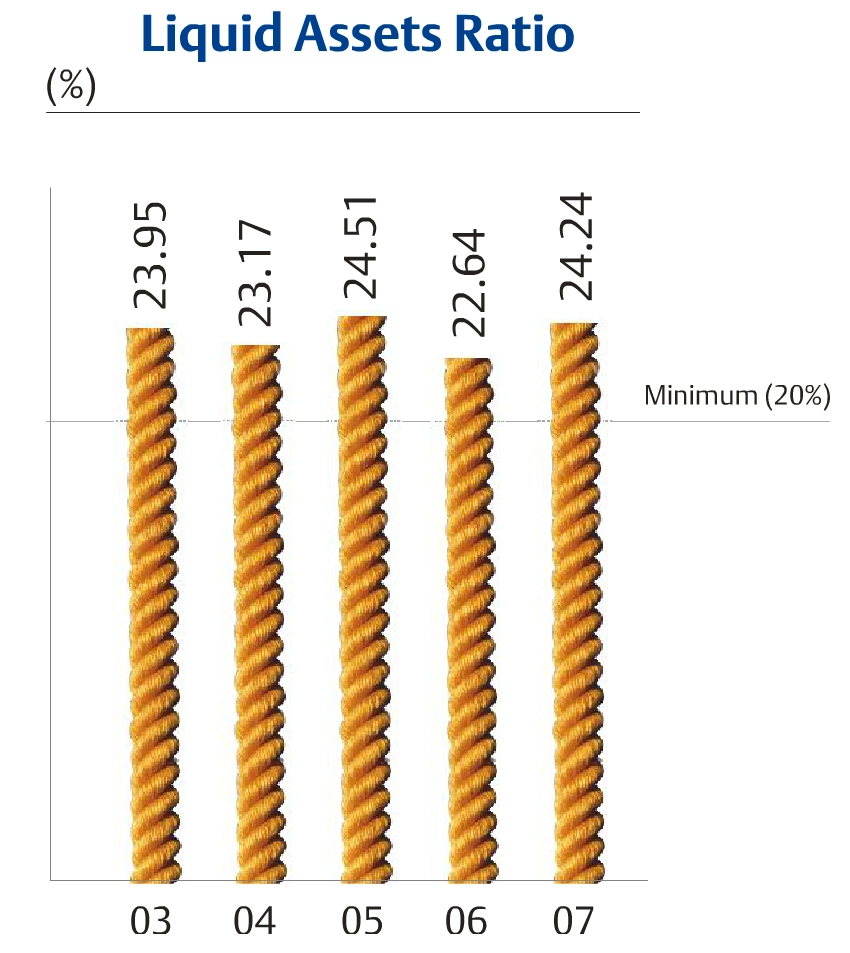

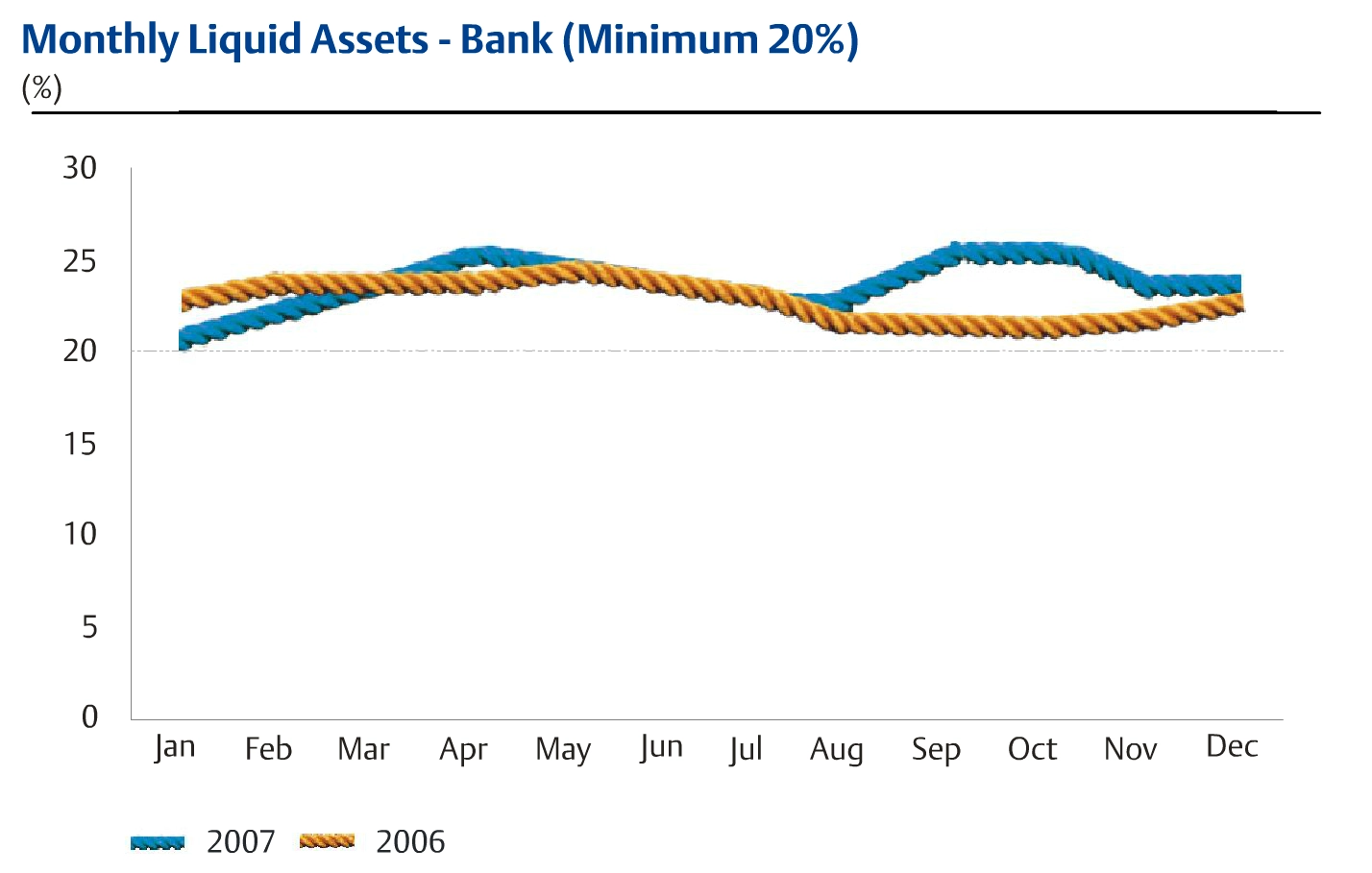

The Treasury is primarily responsible for managing the liquidity, exchange positions, exposure to market risks, mobilising resources from domestic as well as international markets, achieving preferred balance sheet mix and maximising the returns whilst minimising the risk to the Bank.

Sri Lankan financial markets faced a great deal of change in 2007 amidst volatility. Rupee interest rates traded as high as 40% on occasions. Treasury Bill yields picked up sharply after opening the year around 12.70%. The USD/LKR was also volatile with the rupee weakening by nearly 5.58% to touch a historical low at Rs. 113.50 at one stage in 2007, before ending the year firmer at

Rs. 108.50 levels after an influx of dollars through the Government’s foreign debt financing policy.

The local rupee bond market was opened to foreigners and this was received well by investors looking for carry trade related opportunities. For the first time a sovereign bond of US$ 500 million was issued by the Government in 2007.

2007 saw a great deal of volatility in global markets with the US sub prime issue taking centre stage. The dollar came under pressure mainly due to this against most currencies, with EUR, GBP, CAD and AUD gaining the most. Commodity prices like oil and gold appreciated sharply and their gains are expected to continue in 2008. Interest rate climate saw the US and UK ending the year with a rate cutting bias on the back of sub prime worries, even though inflationary pressure from rising commodity prices were threatening.