| MANAGEMENT DISCUSSION AND ANALYSIS | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Financial Review

The Bank was able to record excellent results in every business segment it operated during the year. The Bank stepped into new geographical locations locally as well as in Bangladesh, establishing business relationships with the members of these new distinct localities. Now, the Commercial Bank delivers its services from 163 branches locally, 9 branches in Bangladesh connected to a common computer network besides fulfilling the needs of members of the community through 291 ATMs, the single largest ATM network in the country which is connected to over 1,000,000 Cirrus and Maestro ATMs network globally. Business Promotion Officers have been placed in several Middle Eastern countries to canvass inward remittances of the expatriate community to the country. Additionally, arrangements are being made to place a few Bank officers at selected overseas locations. During the year, the customer base of the Bank increased substantially thus bringing new business opportunities to the Bank. Despite the substantial increases recorded in business volumes, the Bank managed to maintain a consistent risk profile in the asset portfolio of the Bank during the year.

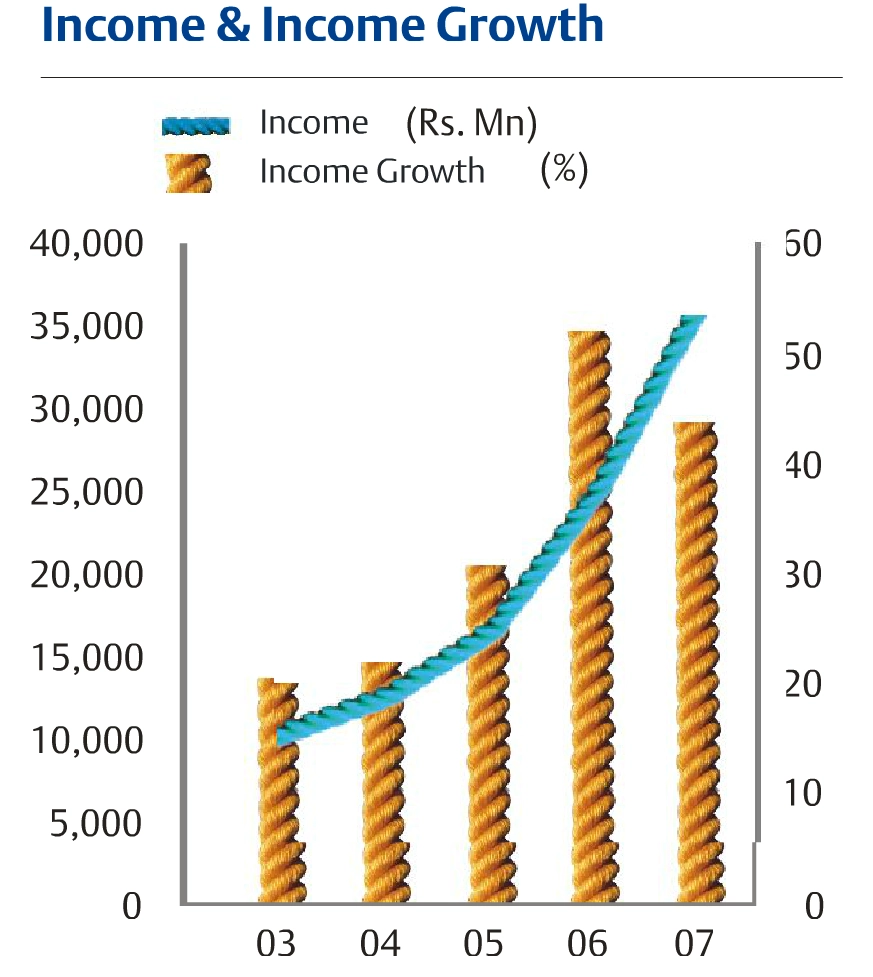

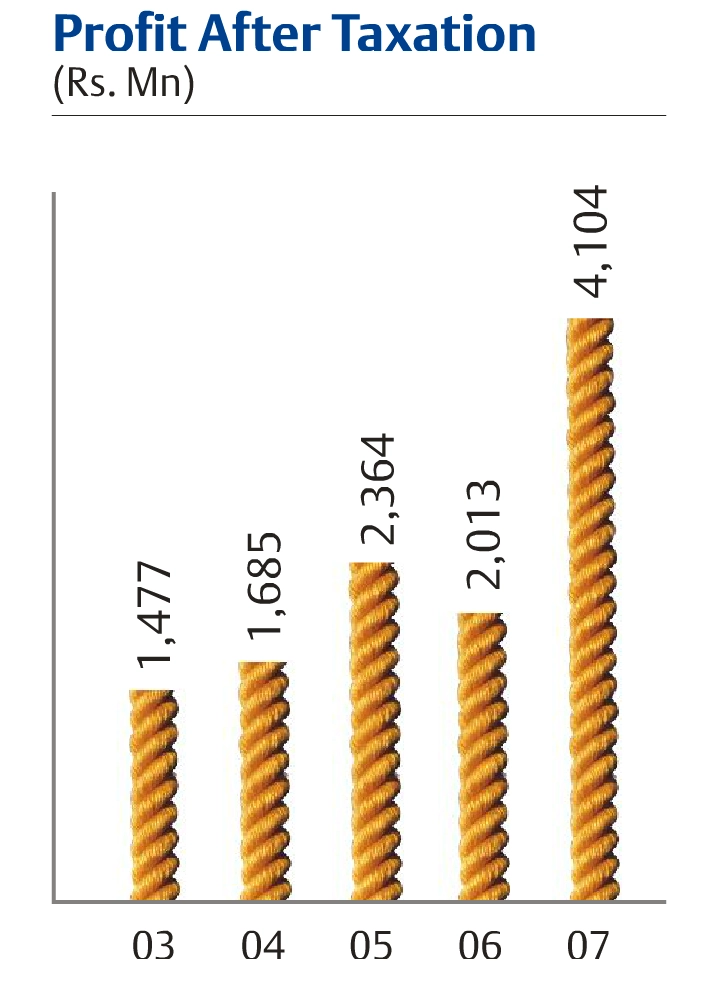

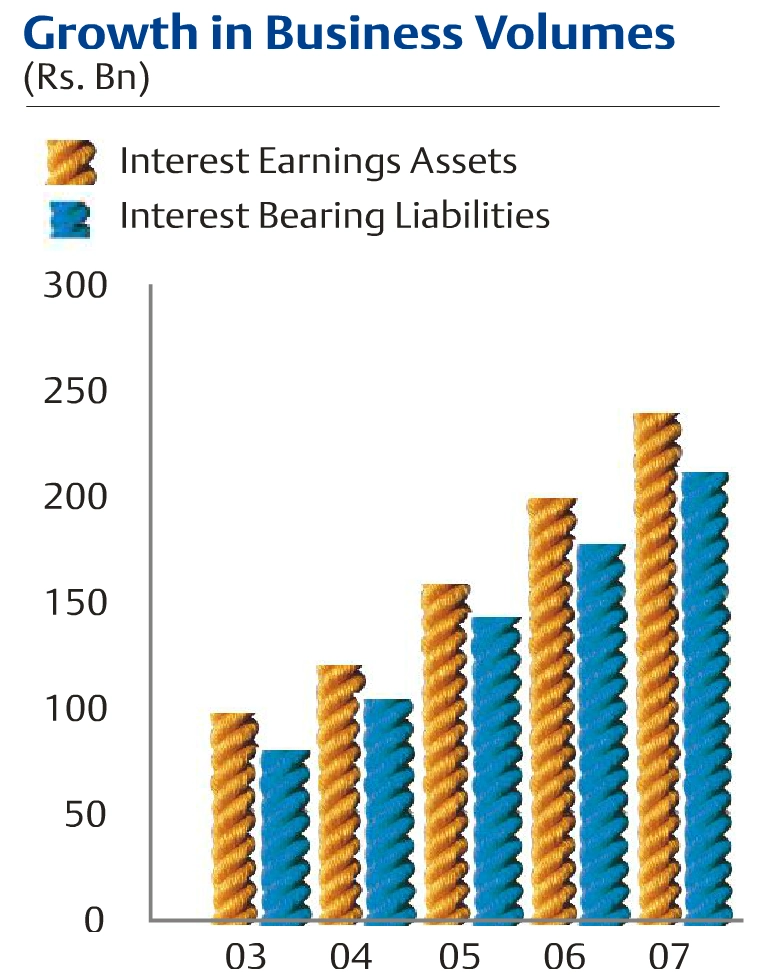

The pre-tax profit of the Bank grew to Rs. 6.705 billion from Rs. 4.214 billion reported last year, recording a phenomenal increase of Rs. 2.491billion or 59.12% over the previous year. Provision for taxation recorded a lower increase of 18.19% mainly due to effective tax planning measures adopted by the Bank. As a result, the profit after tax reached Rs. 4.104 billion compared to Rs. 2.013 billion recorded in the previous year representing a monumental growth of Rs. 2.091 billion or 103.89%. However, after discounting for the exceptional items recorded in 2006, being the initial cost incurred on account of restructuring the Pension Scheme of the Bank and profit earned on disposal of DFCC shares too, the pre-tax and post-tax profit for 2007, recorded an increase of Rs. 1.738 billion and Rs. 1.337 billion or 34.99% and 48.35% respectively, over the normalised pre-tax and post-tax profits recorded for 2006 by the Bank. The increase in profits was mainly facilitated by the impressive growths recorded in fund and fee based operations of the Bank during the year under review. Strong organic growth in business volumes and prudent fund management amidst a volatile and increasing interest rate environment contributed in recording a substantial growth in net interest income. The volumes of deposit recorded an increase of 16.26% to reach Rs.183.110 billion while total net advances recorded an increase of 15.81% to reach Rs. 174.324 billion over the previous year. The total interest earning assets reached Rs. 240.833 billion from It is noteworthy to mention that the pre-and post-tax profits of the Bank reported above were achieved after providing

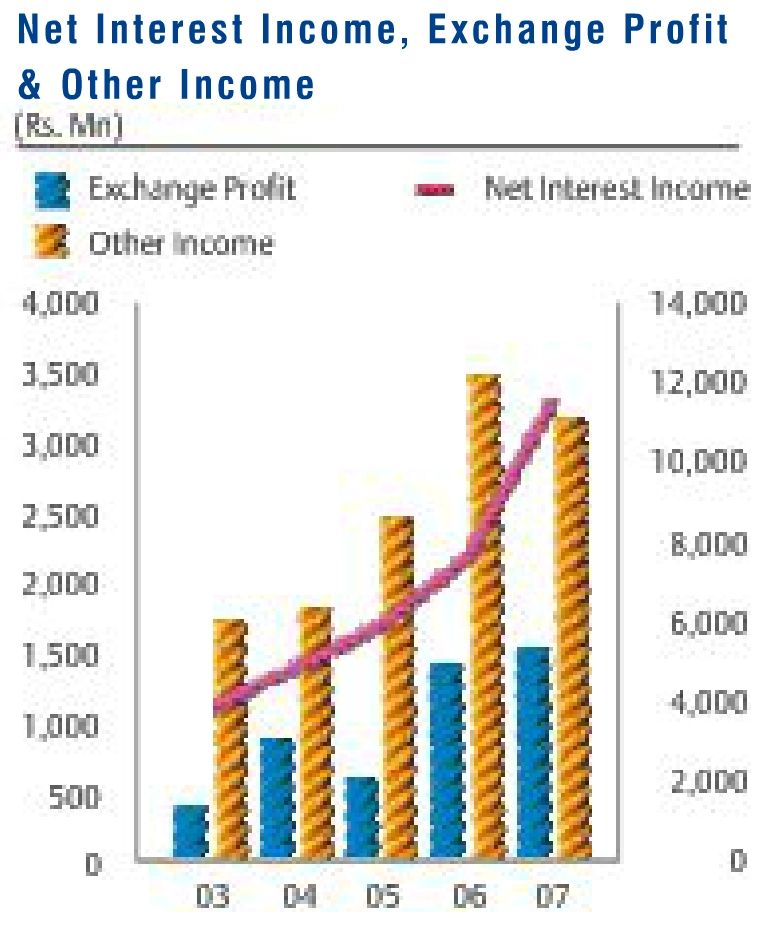

Foreign exchange profits recorded a moderate growth of 7.35% to reach Rs. 1.545 billion. This moderate growth was mainly attributable to the drops recorded in revaluation of OBC’s retained profit kept in US dollars. However, foreign exchange trading recorded a substantial increase over the previous year. The LKR/US$ rate was volatile during the year, however, before ending firmer at Rs. 108.50 after an influx of dollars through the Government’s foreign debt financing policy. On year-to-year basis, the LKR recorded a depreciation of 0.93% against the US$ in 2007 compared to 5.37% recorded a year ago. The growth in business volumes resulted in an increase of fees and commission-based income by 18.46% compared to the previous year. However, a negative growth of 46.72% was recorded in other income as a result of profit on disposal of DFCC shares being included in the other income of previous year. After discounting for such effect, the other income in 2007 recorded a growth of 6.92% compared to the previous year. Operating expenses continued to remain under firm control. As a result, the growth in earnings well exceeded the growth in costs. After discounting for the effect on initial cost of re-structuring the Pension Scheme and the saving on financial VAT thereon, the normalised operating expenses recorded an increase of 26.81% over the previous year which was well below the growth of 38.31% reported in earnings. As a result, the Cost to Income ratio of the Bank recorded a substantial improvement to reach 47.87% by the year end compared to 52.21% recorded a year earlier. It is pertinent to mention that the Cost to Income ratio of the Bank is considered to be the best ratio reported by a local commercial bank, based on the results published up to September 30, 2007. The Bank depended solely on the retention of profits to support the enhanced capital requirements consequent to the increase recorded in the asset-base of the Bank. As a result, the Bank witnessed a deteriorating Capital Adequacy ratio during the last few years. This situation has further aggravated due to the increased risk weights applied on facilities granted against residential mortgages and other loans and advances as per a Direction issued by the Central Bank in 2006. With a view to addressing this dilemma as well as to supplement deposit mobilisation efforts, the Bank made a rights issue of ordinary shares on the basis of 3 for 10 and raised Rs. 5.741 billion during first half of the year. Subsequently, the Bank also made a scrip issue of shares on the basis of 1 for 3. Total assets of the Bank increased to Rs. 267.940 billion as at December 31, 2007, as against Rs. 223.974 billion reported as at December 31, 2006, recording a growth of Rs. 43.966 billion or 19.63%. The Bank’s Bangladesh operations continued to perform remarkably well, building customer relationships and increasing the branch network. Consequent to this performance, the Bangladesh operations repatriated a profit of US$ 1.800 million during 2007. Thus, this operation has so far remitted US$ 4.500 million during the two years ended December 31, 2007. Commercial Bank recorded the largest market capitalisation of Rs. 34.234 billion among all listed banks and financial institutions in Sri Lanka and ranked No. 4 (No. 5 in 2006) among all listed companies on the Colombo Stock Exchange. The Directors recommended a final dividend of Rs. 2.50 per share payable on March 28, 2008, which together with three interim dividends already paid totalling to Rs. 4.50 per share, will add up to a total dividend of Rs. 7.00 per share for the year 2007, on the enhanced issued share capital of the Bank consequent to the rights and bonus issues mentioned above. Thus, the Bank has declared a total dividend of Rs. 1.743 billion to its ordinary shareholders for 2007, as against Rs. 0.716 billion paid for 2006, an increase of Rs. 1.027 billion. The Dividend Payout ratio of the Bank including the final dividend declared, amounted to 43.67% for the year which is also well above the minimum of 25.00% prescribed under the Deemed Dividend Tax rule. It is noteworthy to mention that the Bank has been able to maintain Compounded Annual Growth Rates in excess of 24.00% for both deposits and loans & advances and 25.00% in pre-tax profits over the past ten years. The following table summarises the Bank’s performance with regard to some of the key objectives set at the beginning of the year:

As shown in the table, the Bank achieved most of the budgeted targets set at the beginning of the year whilst recording substantial improvements over the previous year. Growth in all business segments, as evidenced by the increase in revenue have been the main drivers behind the Bank’s achievement during 2007. The pre-tax profit of the Commercial Bank Group amounted to Rs. 6.791 billion as against Rs. 4.321 billion recorded in 2006, which amounted to a growth of 57.15%. The post-tax profit of the Group for the year amounted to Rs. 4.152 billion reflected a growth of 100.37%, compared to the post-tax profit of Rs. 2.072 billion of the Group in 2006. The factors that contributed to the excellent performance of the Bank have been attributable to record such high growth rates in the Group as well. However, after discounting for the effects of exceptional items recorded in 2006, the pre-and post-tax profits of the Group recorded a growth of 33.82% and 46.95% respectively. As a result, the financial ratios of the Group have recorded substantial improvements over the previous year. The Group reported a basic Earnings Per Share of Rs. 17.04. The contribution made by the four broad business divisions viz. the Corporate Banking, the Personal Banking, International Operations and the Treasury to the profits and business volumes of these divisions is summarised below:

The performance, major initiatives during 2007 and plans for the future of these four divisions are discussed in detail. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||